Paul Krugman has a new article, Why A Trade War With China Isn’t ‘Easy To Win’ (Slightly Wonkish), in The New York Times, in which he rightly points out Donald Trump’s switching positions on trade with China. Krugman however has a generic point about international trade as some kind of mercantilism:

Admittedly, the political economy of trade is kind of mercantilist, because it’s driven largely by producer interests. Long ago I wrote about “GATT-think”, the view of trade, enshrined in international negotiations, that sees exports as good, imports as bad, so that letting someone sell us stuff, even if it’s better and cheaper than we could make ourselves, is a “concession.” The genius of the postwar international trading system was that it harnessed this special-interest reality, using the ambitions of exporters to offset the protectionism of those competing with imports, to engineer a kind of enlightened mercantilism that vastly expanded world trade.

[italics: mine]

So Krugman is admitting that it is in the interest of big producers, but claiming that his interests aren’t aligned with them and that the rules of trading were made such that it somehow offset them.

The reality is of course different. More successful countries do not need protection at home. At least we can say that they’re are willing to forgo protectionism as the advantage from selling more easily in markets abroad is immense. As Joan Robinson pointed out in a 1977 article (and even before), What Are The Questions?

From a long-run point of view, export-led growth is the basis of success. A country that has a competitive advantage in industrial production can maintain a high level of home investment, without fear of being checked by a balance-of-payments crisis. Capital accumulation and technical improvements then progressively enhance its competitive advantage. Employment is high and real-wage rates rising so that “labour trouble” is kept at bay. Its financial position is strong. If it prefers an extra rise of home consumption to acquiring foreign assets, it can allow its exchange rate to appreciate and turn the terms of trade in its own favor. In all these respects, a country in a weak competitive position suffers the corresponding disadvantages.

When Ricardo set out the case against protection, he was supporting British economic interests. Free trade ruined Portuguese industry. Free trade for others is in the interests of the strongest competitor in world markets, and a sufficiently strong competitor has no need for protection at home. Free trade doctrine, in practice, is a more subtle form of Mercantilism. When Britain was the workshop of the world, universal free trade suited her interests. When (with the aid of protection) rival industries developed in Germany and the United States, she was still able to preserve free trade for her own exports in the Empire. The historical tradition of attachment to free trade doctrine is so strong in England that even now, in her weakness, the idea of protectionism is considered shocking.

[italics: mine]

The last sentence is also important when discussing Krugman. The United States’ balance of payments has deteriorated and needs some protectionism. But economists are attached to the idea of free trade like it’s some dogma.

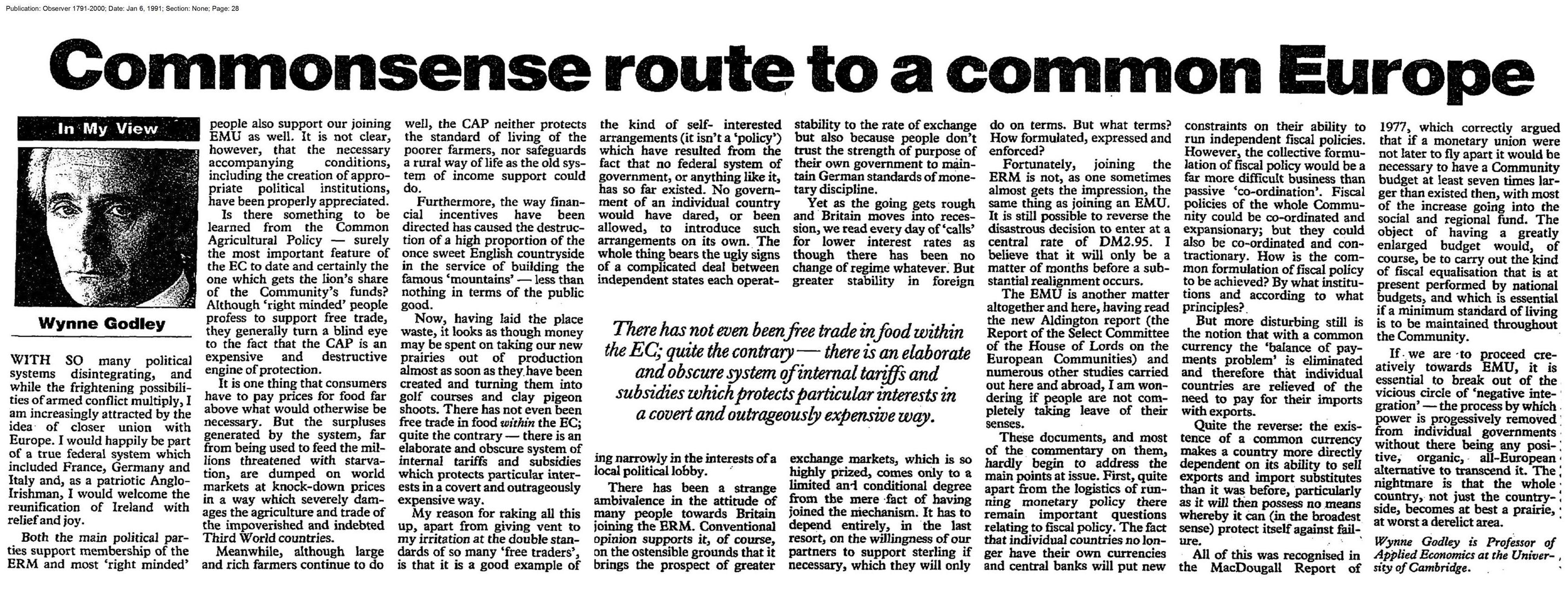

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

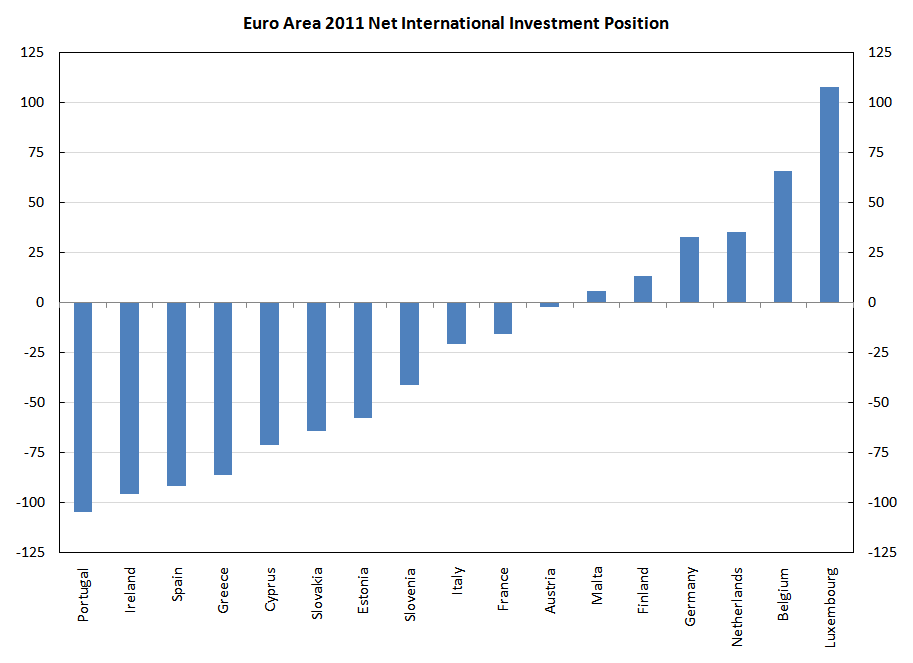

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

The first talk is about what economics is and ought to be, how we define it, how it is taught and practiced and how much the public is aware of it, how it was political economy many years back and now pretends to be non-political and so on.

The second lecture is about development in general. It tells an interesting story in the start about Jakarta, Indonesia where there’s a separate lane for car pooling. Chang says how some rich person would enter the carpool by getting people at the entrance and whose job is to just sit in the car!

The French edition of Keynes’ The General Theory, has a nice preface explaining what his book is all about. It is dated 20 February 1939.

This is available in The Collected Writings Of John Maynard Keynes, Volume VII – The General Theory Of Employment, Interest And Money. The Collected Writings has volumes I-XXX.

First, Keynes announces how he is breaking from orthodoxy:

For a hundred years or longer English Political Economy has been dominated by an orthodoxy. That is not to say that an unchanging doctrine has prevailed. On the contrary. There has been a progressive evolution of the doctrine. But its presuppositions, its atmosphere, its method have remained surprisingly the same, and a remarkable continuity has been observable through all the changes. In that orthodoxy, in that continuous transition, I was brought up. I learnt it, I taught it, I wrote it. To those looking from outside I probably still belong to it. Subsequent historians of doctrine will regard this book as in essentially the same tradition. But I myself in writing it, and in other recent work which has led up to it, have felt myself to be breaking away from this orthodoxy, to be in strong reaction against it, to be escaping from something, to be gaining an emancipation.

Then Keynes says what he is doing:

I have called my theory a general theory. I mean by this that I am chiefly concerned with the behaviour of the economic system as a whole,—with aggregate incomes, aggregate profits, aggregate output, aggregate employment, aggregate investment, aggregate saving rather than with the incomes, profits, output, employment, investment and saving of particular industries, firms or individuals. And I argue that important mistakes have been made through extending to the system as a whole conclusions which have been correctly arrived at in respect of a part of it taken in isolation.

Keynes, I imagine thought that the root of all orthodoxy is the saving-investment identity. Once this is understood, things follow more easily. He says:

Let me give examples of what I mean. My contention that for the system as a whole the amount of income which is saved, in the sense that it is not spent on current consumption, is and must necessarily be exactly equal to the amount of net new investment has been considered a paradox and has been the occasion of widespread controversy. The explanation of this is undoubtedly to be found in the fact that this relationship of equality between saving and investment, which necessarily holds good for the system as a whole, does not hold good at all for a particular individual. There is no reason whatever why the new investment for which I am responsible should bear any relation whatever to the amount of my own savings. Quite legitimately we regard an individual’s income as independent of what he himself consumes and invests. But this, I have to point out, should not have led us to overlook the fact that the demand arising out of the consumption and investment of one individual is the source of the incomes of other individuals, so that incomes in general are not independent, quite the contrary, of the disposition of individuals to spend and invest; and since in turn the readiness of individuals to spend and invest depends on their incomes, a relationship is set up between aggregate savings and aggregate investment which can be very easily shown, beyond any possibility of reasonable dispute, to be one of exact and necessary equality.

He then says how output is determined not by the capacity to produce but dynamic demand-led processes:

Rightly regarded this is a banale conclusion. But it sets in motion a train of thought from which more substantial matters follow. It is shown that, generally speaking, the actual level of output and employment depends, not on the capacity to produce or on the pre-existing level of incomes, but on the current decisions to produce which depend in turn on current decisions to invest and on present expectations of current and prospective consumption. Moreover, as soon as we know the propensity to consume and to save (as I call it), that is to say the result for the community as a whole of the individual psychological inclinations as to how to dispose of given incomes, we can calculate what level of incomes, and therefore what level of output and employment, is in profit-equilibrium with a given level of new investment; out of which develops the doctrine of the Multiplier.

and introducing the paradox of thrift:

Or again, it becomes evident that an increased propensity to save will ceteris paribus contract incomes and output; whilst an increased inducement to invest will expand them. We are thus able to analyse the factors which determine the income and output of the system as a whole;—we have, in the most exact sense, a theory of employment. Conclusions emerge from this reasoning which are particularly relevant to the problems of public finance and public policy generally and of the trade cycle.

Keynes then argues against the typical claim that the rate of interest adjusts to bring saving equal to investment:

Another feature, specially characteristic of this book, is the theory of the rate of interest. In recent times it has been held by many economists that the rate of current saving determined the supply of free capital, that the rate of current investment governed the demand for it, and that the rate of interest was, so to speak, the equilibrating price-factor determined by the point of intersection of the supply curve of savings and the demand curve of investment. But if aggregate saving is necessarily and in all circumstances exactly equal to aggregate investment, it is evident that this explanation collapses. We have to search elsewhere for the solution. I find it in the idea that it is the function of the rate of interest to preserve equilibrium, not between the demand and the supply of new capital goods, but between the demand and the supply of money, that is to say between the demand for liquidity and the means of satisfying this demand.

Keynes then announces his break away from Monetarism:

I have called this book the General Theory of Employment, Interest and Money; and the third feature to which I may call attention is the treatment of money and prices. The following analysis registers my final escape from the confusions of the Quantity Theory, which once entangled me. I regard the price level as a whole as being determined in precisely the same way as individual prices; that is to say, under the influence of supply and demand. Technical conditions, the level of wages, the extent of unused capacity of plant and labour, and the state of markets and competition determine the supply conditions of individual products and of products as a whole. The decisions of entrepreneurs, which provide the incomes of individual producers and the decisions of those individuals as to the disposition of such incomes determine the conditions. And prices—both individual prices and the price-level— emerge as the resultant of these two factors. Money, and the quantity of money, are not direct influences at this stage of the proceedings. They have done their work at an earlier stage of the analysis. The quantity of money determines the supply of liquid resources, and hence the rate of interest, and in conjunction with other factors (particularly that of confidence) the inducement to invest, which in turn fixes the equilibrium level of incomes, output and employment and (at each stage in conjunction with other factors) the price-level as a whole through the influences of supply and demand thus established.

And finally attacks the docrine of Say’s Law:

I believe that economics everywhere up to recent times has been dominated, much more than has been understood, by the doctrines associated with the name of J.-B. Say. It is true that his ‘law of markets’ has been long abandoned by most economists; but they have not extricated themselves from his basic assumptions and particularly from his fallacy that demand is created by supply. Say was implicitly assuming that the economic system was always operating up to its full capacity, so that a new activity was always in substitution for, and never in addition to, some other activity. Nearly all subsequent economic theory has depended on, in the sense that it has required, this same assumption. Yet a theory so based is clearly incompetent to tackle the problems of unemployment and of the trade cycle. Perhaps I can best express to French readers what I claim for this book by saying that in the theory of production it is a final break-away from the doctrines of J.-B. Say and that in the theory of interest it is a return to the doctrines of Montesquieu.

If you have read Monetary Economics by Wynne Godley and Marc Lavoie, you will notice that their approach is quite close to this spirit. In their approach, the components of demand which are exogenous are government expenditure and exports. Etc.

After the recent Employment Situation Summary by the U.S. Bureau Of Labour Studies, it is becoming more clear that the concept of NAIRU is a chimera, a deceit.

In a 1943 article, Joan Robinson talked of why the establishment wishes to keep a fraction of the population unemployed. It is quoted in Nicholas Kaldor’s 1983 article, Keynesian Economics After Fifty Years:

… recession hit a number of countries and it became generally believed (rightly or wrongly) that ‘Keynesian’ instruments of economic policy were unavailable for coping with this situation. At the same time the anti-Keynesian school of economists, the ‘new’ monetarists, rapidly gained followers among influential people more or less simultaneously in a number of countries and this was combined by widespread and rapidly growing antagonism to Keynesian ideas. The reason for this antagonism, not openly acknowledged, was the change in the power structure of society which the pursuit of Keynesian policies had brought about. This was foreseen well before the adoption of Keynesian methods of demand management. Thus in an article in The Times in January 1943 on post-war Full Employment it was stated:

Unemployment is not a mere accidental blemish in a private- enterprise economy. On the contrary, it is part of the essential mechanism of the system, and has a definitive function to fulfil. The first function of unemployment (which has always existed in open or disguised forms) is that it maintains the authority of masters over men. The master has normally been in a position to say: ‘If you don’t want the job, there are plenty of others who do’. When the man can say ‘If you don’t want to employ me there are plenty of others who will’ the situation is radically altered.4

The change in the workers’ bargaining position which should follow from the abolition of unemployment would show itself in another and more subtle way. Unemployment in a private enterprise economy has not only the function of preserving discipline in industry, but also indirectly the function of preserving the value of money. If free wage bargaining as we have known it hitherto, is continued in conditions of full employment, there would be a constant upward pressure upon money wage-rates. This phenomenon also exists at the present time, and is kept within bound by the appeal of patriotism. In peace-time the vicious spiral of wages and prices might become chronic.5

4 The doctrine is usually associated with Karl Marx who argued that capitalism can only function with a ‘reserve army’ of unemployed labour. But Marx himself owes these ideas (though he never seems to have acknowledged it) to Adam Smith, who wrote in the Wealth of Nations that normally there is always a scarcity of jobs relative to job-seekers: ‘There could seldom be any scarcity of hands nor could the masters be obliged to bid against one another in order to get them. The hands, on the contrary, would in this case, naturally multiply beyond their employment. There would be a constant scarcity of employment and the labourers would be obliged to bid against one another in order to get it. If in such a country the wages of labour had ever been more than sufficient to maintain the labourer and to enable him to bring up a family, the competition of the labourers and the interest of the masters would soon reduce them to the lowest rate which is consistent with common humanity’ (Book I, ch. VIII, p. 24).

5 ‘Planning Full Employment – Alternative Solutions of a Dilemma’, The Times, 23 January 1943. (A ‘turnover’ article; the article was unsigned but its authorship is generally attributed to Joan Robinson.)

Recently the University Of York hosted a talk by Ha-Joon Chang on deindustrialisation. The title of the talk was: Manufacturing Matters – The Myth Of Post-Industrial Knowledge Economy.

You will find a lot of emphasis on manufacturing in Nicholas Kaldor and Wynne Godley’s work. Why is manufacturing important? Wynne Godley emphasised the supremacy of manufactured products over services in exports, since it’s more difficult to export services. Nicholas Kaldor also suggested increasing returns to scale in manufacturing.

We are frequently told that manufacturing lost its importance. Ha-Joon Chang’s talk is precisely in debunking this myth. As Wynne Godley emphasised, while the share of manufacturing in GDP has fallen, the share of imports has risen a lot. Ha-Joon Chang also points out another important point that superficial reading of data might mislead. So because of offshoring and how the data is recorded by national accounts, it might look like there is no manufacturing happening. For example—and the real thing is more complicated—Apple manufactures phones, computers, etc., in China and it is recorded as an export of services in U.S. balance of payments and hence not as manufacturing in the production account of U.S. national accounts.

You can view the talk on YouTube. It has slides and audio.

The Levy Institute Of Bard College was far ahead of anyone with its prescience on the fate of the U.S. economy (and also the world) before the crisis. So everyone should read them. Michalis Nikiforos and Gennaro Zezza have a new Strategic Analysis report.

Abstract:

The US economy has been expanding continuously for almost nine years, making the current recovery the second longest in postwar history. However, the current recovery is also the slowest recovery of the postwar period.

This Strategic Analysis presents the medium-run prospects, challenges, and contradictions for the US economy using the Levy Institute’s stock-flow consistent macroeconometric model. By comparing a baseline projection for 2018–21 in which no budget or tax changes take place to three additional scenarios, the authors isolate the likely macroeconomic impacts of: (1) the recently passed tax bill; (2) a large-scale public infrastructure plan of the same “fiscal size” as the tax cuts; and (3) the spending increases entailed by the Bipartisan Budget Act and omnibus bill. Finally, Nikiforos and Zezza update their estimates of the likely outcome of a scenario in which there is a sharp drop in the stock market that induces another round of private-sector deleveraging.

Although in the near term the US economy could see an acceleration of its GDP growth rate due to the recently approved increase in federal spending and the new tax law, it is increasingly likely that the recovery will be derailed by a crisis that will originate in the financial sector.

Dani Rodrik has a nice interview to ProMarket, the blog of the Stigler Center at the University of Chicago Booth School of Business. Rodrik’s views are dissenting but within the conventional DC wisdom/New Consensus. For example, he said as recently as last year that free trade is fine as long as losers as compensated, which is far from accurate, as free trade leads to loser regions as well. Still he has better views than neoliberals. In this interview Rodrik is asked about the ant-globalisation backlash:

Q: Much of the anti-globalization backlash of the last two years has been xenophobic, racist, authoritarian in nature. What is it about the nature of globalization that led to this kind of response?

I think a lot of it has to do with the fact that the left has been missing in action. Twenty years ago, when I was fretting that globalization would create a backlash, I would have guessed that the main beneficiary of this might have been the left, because it would capitalize on the economic and social grievances that these divisions create. Indeed, when we think about the populisms of the late 19th century—in the US or for that matter Latin America, with its long history of populism—they were by and large not racist and xenophobic, ethno-nationalist populisms, but left-wing populisms that focused on financial elites, on corporate elites, and pushed for social reform and more regulation of the economy.

Today, here and in Europe, we’re seeing much more of a right-wing ethnonationalist backlash. I think it’s partly that the left has been missing in action and that the center-left and the social democrats have essentially been complicit in many of these changes since the 1990s. New Democrats in the US and New Labour in the UK were at the very forefront of this push for hyperglobalization, so they couldn’t easily disassociate themselves from this complicity. I think Hillary Clinton’s ill-fated campaign showed that very well.

There were other shocks that made it easier. For example, immigration made it easy for right-wing nativists to provide a much more nativist, ethnonationalist frame for economic and social grievances to which I think one might have responded very differently.

This is a fairly accurate description of what has happened. As I have mentioned many times, the absence of a strong political alternative gave enough opportunities for the far right to come to power. It had an appeal—which the left lacked—although no real solution.

Although we see a lot of left-wing activism these days, it is mainly restricted to cultural issues. People still hold right wing economic ideas while sounding faux left wing.

Austerity measures adopted in the wake of the global financial crisis nearly a decade ago have compounded this state of affairs. Such measures have hit the world’s poorest communities the hardest, leading to further polarization and heightening people’s anxieties about what the future might hold. Some political elites have been adamant that there is no alternative, which has proved fertile economic ground for xenophobic rhetoric, inward-looking policies and a beggar-thy-neighbour stance. Others have identified technology or trade as the culprits behind exclusionary hyperglobalization, but this too distracts from an obvious point: without significant, sustainable and coordinated efforts to revive global demand by increasing wages and government spending, the global economy will be condemned to continued sluggish growth, or worse.

The Trade and Development Report 2017 argues that now is the ideal time to crowd in private investment with the help of a concerted fiscal push – a global new deal – to get the growth engines revving again, and at the same time help rebalance economies and societies that, after three decades of hyperglobalization, are seriously out of kilter. However, in today’s world of mobile finance and liberalized economic policies, no country can do this on its own without risking capital flight, a currency collapse and the threat of a deflationary spiral. What is needed, therefore, is a globally coordinated strategy of expansion led by increased public expenditures, with all countries being offered the opportunity of benefiting from a simultaneous boost to their domestic and external markets.

Kaldorians have been stressing how the Euro project is a half-baked idea. Nicholas Kaldor himself predicted in 1971 that the Euro Area without a federal government would be a failure and warned the establishment.

Anthony Thirlwall—the literary executor of Kaldor—also had his great predictions.

In an article, The Euro And Regional Divergence In Europe, in the book, The Eurosceptical Reader 2, in the year 2000 even predicted the rise of dark forces and the alt-right!

Some quotes:

Page 33:

The regional disaffection that will be caused by deteriorating economic circumstances in countries that lack the policy instruments to deal with economic crisis can too easily become the breeding ground for nationalism and fascism, and political resentment, as witnessed in Europe in the 1920s and 1930s. By all means, let there be more coordination of economic policies in Europe and let the countries of Europe strive for greater political cooperation in areas such as defence, human rights and relations with other countries, but not by luring them into an economic straitjacket over which there is no democratic control and from which there is no easy escape. This is a recipe for political turmoil and the fragmentation of Europe that Britain would be wise to steer clear of.

[italics: mine]

Page 28:

… paradoxically, the euro could become a threat to European integration and stability if it exacerbates regional differences within the EU which I believe it is likely to do. Shocks to countries and to regions within countries are rarely symmetric. Without the instruments to cope, asymmetric shocks will exacerbate regional differences, with the prospect of civil strife, political unrest and disaffection with the whole EU project in the affected regions. Regional policies in the EU are a poor substitute for the ability of individual countries to cope with shocks in their own way.

Page 30:

Loss of economic sovereignty

Adoption of the euro means the abandonment of all the traditional weapons of economic policy that in the past have served countries reasonably well. It is hard to imagine how the countries of Europe would have fared in the post-war years without the active use of monetary, fiscal and exchange rate policy. Relinquishing these instruments of policy could spell disaster for individual countries in the future.

Page 32:

Nowhere in the pacts and conditions governing Economic and Monetary Union and the single currency are there any safeguards against deflationary policies and deflationary conditions such as rising unemployment, falling prices or even governments running budget surpluses. The ‘rules of the game’ are asymmetrical, biased against inflation, as indeed they are at the international level whereby the International Monetary Fund penalises countries in balance of payments deficit, but not those in surplus, which therefore imparts deflationary bias in the world economy.

Page 49:

It would be churlish to wish the euro ill, but I fear that it is going to do great damage to the economies of Europe and to the noble objective of greater European harmony and cooperation. Economic and social disparities between the countries and regions of Europe are still vast, and there is nothing in the euro itself which is going to eliminate these disparities. If anything, without an effective regional policy and fiscal transfer mechanisms, they are likely to widen, making the task of political integration – if that is the ultimate aim of the euro – that much more difficult. The United Kingdom government would do well to steer clear of this risky venture for more than the lifetime of even the next Parliament.

PSL Quarterly Review has a new series Recollections Of Eminent Economists and Anthony Thirlwall has the inaugural contribution.

Abstract:

The paper is the first inaugural contribution to the new series of “Recollections of Eminent Economists”. Under this name, the previous series of the journal (then called “Banca Nazionale del Lavoro Quarterly Review”) used to publish autobiographic essays in which renowned economists described their scientific path and reflected on the recent developments of the discipline. In this work, A.P. Thirlwall recalls his personal and academic biography, ranging from employment in the UK to consultancy work in developing countries, and comments on the reception of his main works. Among the latter, special attention is paid to regional and development economics, as well as to the relation between the balance of payments and economic growth. Throughout the discussion, the author emphasizes the Keynesian inspiration of his analyses.

{kind=link}