xkcd:

xkcd alt text: Hang on, I just remembered another thing I’m right about. See…

… There is also the problem of the relative levels of different types of earned income. Here we have the famous marginal productivity theory. In perfect competition an employer is supposed to take on such a number of men that the money value of the marginal product to him, taking account of the price of his output and the cost of his plant, is equal to the money wage he has to pay. Then the real wage of each type of labor is believed to measure its marginal product to society. The salary of a professor of economics measures his contribution to society and the wage of a garbage collector measures his contribution. Of course, this is a very comforting doctrine for professors of economics, but I fear that once more the argument is circular. There is not any measure of marginal products except the wages themselves. In short, we have not got a theory of distribution.

We have nothing to say on the subject which above all others occupies the minds of the people whom economics is supposed to enlighten.

[italics in original]

– Joan Robinson, The Second Crisis Of Economic Theory, 1972. Link

There’s an article at Evonomics by Joseph Stiglitz, which is an excerpt from a chapter from a book. Stiglitz has denounced the marginal productivity theory. He says:

The trickle-down notion— along with its theoretical justification, marginal productivity theory— needs urgent rethinking. That theory attempts both to explain inequality— why it occurs— and to justify it— why it would be beneficial for the economy as a whole. This essay looks critically at both claims. It argues in favour of alternative explanations of inequality, with particular reference to the theory of rent-seeking and to the influence of institutional and political factors, which have shaped labour markets and patterns of remuneration. And it shows that, far from being either necessary or good for economic growth, excessive inequality tends to lead to weaker economic performance. In light of this, it argues for a range of policies that would increase both equity and economic well-being.

… Neoclassical economists developed the marginal productivity theory, which argued that compensation more broadly reflected different individuals’ contributions to society.

It reminds me of the debate between Paul Krugman and Thomas Palley some time ago. Paul Krugman completely denied all this. In his blog post at his blog for The New York Times, Krugman said in April 2014:

But doesn’t that show that conventional economics is indeed capable of accommodating big concerns about inequality? You fairly often find heterodox economists insisting that to accept the idea that capital and labor are paid their marginal products, even as a working hypothesis to be modified when you address things like executive pay, is to accept that high inequality is morally justified. But that’s obviously not the case: there are plenty of economists who are willing to use marginal-product models (as gadgets, not as fundamental truth) who don’t at all accept the sanctity of the market distribution of income.

So you have two mainstream economists: Paul Krugman defending orthodoxy and Joseph Stiglitz denouncing the marginal productivity theory.

The holy grail of macroeconomics is to integrate the real and monetary sides of economics. One needs a good balance between the two: one shouldn’t be too much on one side.

In a recent article, Monetary Policy in a Post-Crisis World: Beyond the Taylor Rule for INET, Perry Mehrling correctly identifies the flow of funds approach and Morris Copeland. He says:

Maybe time to look back at Copeland, reconstructing his money flow approach for the modern world? That’s where I’m placing my bet.

Although, his article seems right in lots of parts, it seems to identity purely monetary factors in identifying solutions to the problems of this world. Mehrling says:

From a money flow perspective, there are logically only three sources of funds for agents who find themselves in deficit on the goods and services account. They can dishoard (spend money balances), borrow, or sell some asset. In the argument sketched above, I have suggested that post-war institutional developments have followed a course emphasizing first dishoarding, then borrowing, and then selling, i.e. monetary liquidity, then funding liquidity, then market liquidity. All three are now in play, but the new one is market liquidity. That’s the one that broke in the global financial crisis, and that’s the one we need to fix in order to get the system working again.

While the first part of the argument is correct, I am not sure how fixing “liquidity” is needed to get the system working again. In my reading of Mehrling, he comes across as someone who stresses too much on the monetary side of things and this is another example of it. What do we need to do to fix liquidity exactly? More central bank asset purchases?

The solution to the problems of the world can come about if there is a coordinated fiscal expansion combined with balance of payments targets, to say the least. I am not sure how liquidity fits into this. After the financial crisis which started in 2007, this may have been the case: what was needed was providing liquidity to the financial system. In the U.S., Euro Area and the rest of the world, central banks have helped to provide liquidity to ease financial conditions. But right now—at least in the advanced world—interest rates are low and just lowering them further won’t help increase production. And the same with “liquidity”.

Hence I am unclear about Merhling’s solutions. It’s monetary hippyness.

https://criticalfinance.org/2016/09/08/consistent-modelling-and-inconsistent-terminology/

Jo Michell has a nice reply to Simon-Wren Lewis’ critique of stock-flow coherent models.

[the title of this post is the link]

Look for links to models around the world which use the SFC methodology.

This mini-post is more intended for my own reference, so that I remember this and don’t forget.

After all these years, Mario Draghi has finally said it. After repeatedly insisting Euro Area governments do “structural reforms”, Draghi has conceded that Germany should do a fiscal expansion.

Draghi: Counties that have fiscal space should use it. Germany has fiscal space

— European Central Bank (@ecb) September 8, 2016

Post-Keynesians have always maintained that “surplus” countries put a burden on “deficit” countries. Since Germany has a high positive current account balance, and sells its product abroad, it isn’t unfair to ask its government to expand domestic demand via fiscal policy and reduce imbalances.

In my opinion, what Kaldor calls the principle of circular and cumulative causation (originally ascribed to Gunnar Myrdal) is as much an important principle in economics as is the Keynesian principle of effective demand. The former is built on top of the latter and so we could just have one most important Keynesian principle.

In an article Foundations And Implications Of Free Trade Theory, written in 📚 Unemployment In Western Countries – Proceedings Of A Conference Held By The International Economics Association At Bischenberg, France, Kaldor says:

Owing to increasing returns in processing activities (in manufactures) success breeds further success and failure begets more failure. Another Swedish economist, Gunnar Myrdal called this’the principle of circular and cumulative causation’.

It is as a result of this that free trade in the field of manfactured goods led to the concentration of manufacturing production in certain areas – to a ‘polarization process’ which inhibits the growth of such activities in some areas and concentrates them on others.

In a recent paper titled The debate Over ‘Thirlwall’s Law’: Balance-Of-Payments Constrained Growth Reconsidered, Robert Blecker says:

Another key empirical question is the direction of causality between export growth and capital accumulation: does the former cause the latter (as assumed implicitly in Thirlwall’s Law), or does the latter cause the former (as in some of the newer small-country models)? Perhaps this is a case of truly ‘circular and cumulative causation’, in which investment is required to promote exports and success in exporting in turn induces further investment.

I have always thought—ever since I have read Kaldor—that this is the case. When Kaldor says success creates more success, what he is really saying is that a rise in a success of a nation makes it more competitive and increases its exports and so on.

In Kaldorian models, however, elasticity of imports/exports is taken to be constant. Rise in production leads to a rise in productivity and hence price competitiveness. But there is no way in which there is a causation to non-price competitiveness (propensity to import, or income elasticities).

A more general modeling plus empirical work should actually study the impact on non-price competitiveness. Personally, my guess is that only this will explain the vast divergence in nations’ fortunes, empirically speaking. Without it, won’t be sufficient. Interestingly, I believe the dynamics could be complex and rich and even lead to convergence in some cases, although will remain just a theoretical curiosity.

This is a continuation of my post Simon Wren-Lewis On Wynne Godley’s Models. I was comparing stock-flow coherent models to DSGE models implicitly (didn’t mention the ‘DSGE’).

One of the things I spoke of was behaviour: firms deciding how much to produce. In stock-flow consistent models, it is decided by trends in sales. So if entrepreneurs see a fall in their inventory-to-sales ratio, they’ll produce more typically. This can be made more accurate. See Wynne Godley and Marc Lavoie’s text Monetary Economics for more details.

Here I want to concentrate on models such as DSGE or any other model used by institutions such as the UK Treasury for the case of production. In these models, there is a production function describing how much firms will produce. This is incorrect to begin with. It says nothing about behaviour. If households start borrowing a lot, in DSGE models, producers are still producing the same because production is governed by the production function. In stock-flow consistent models, simple modeling assumptions about how much firms produce are far superior. So in this case, in SFC, more borrowing leads to more sales and a change in sales trends, inventory/sales ratio and hence affecting how much will be produced.

The DSGE production function is thus inconsistent with the Keynesian principle of effective demand. DSGE is not even Keynesian. It’s thus ridiculous how economists defending DSGE models and its ancestors accuse SFC modelers of not paying attention to behaviour.

There is no branch of economics in which there is a wider gap between orthodox doctrine and actual problems than in the theory of international trade.

– Joan Robinson, The Need For A Reconsideration Of The Theory Of International Trade, 1973

Orthodox trade theory tells us that the “market mechanism” should work to resolve imbalances in the current account of balance of international payments. Although, the economics profession has conceded that Keynesianism is correct, it is still far from thinking clearly about international trade.

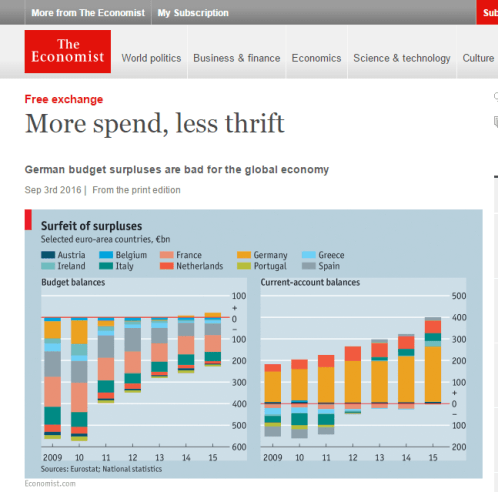

So it is a bit surprising that The Economist would say something unorthodox about this. In a recent article it complains about Germany:

This is the Post-Keynesian idea that surplus economies put a burden on deficit economies.

A fiscal expansion by the German government has the effect of raising domestic demand and imports and reducing the German current account balance of payments. This allows the rest of the world to grow both because of German imports and also because they are less “balance-of-payments constraint”.

Second, Brad Setser has a blog post on the current account surplus of the Republic of Korea (South Korea).

It’s impressive to see Setser get the causality right:

Fiscal policy alone doesn’t determine the current account (even if tends to be the biggest factor in the IMF’s own model). A boom in domestic demand, for example, would improve the fiscal balance and lower the current account surplus, just as a fall in private demand improves the current account balance while raising the fiscal deficit.

The current account balance, government’s budget balance and the private sector financial balance are related by an identity and sum to zero. But the identity itself shouldn’t be confused with causation.

The correct causation between the balances is between domestic demand and output at home versus abroad. This causality has been highlighted by Wynne Godley in the past. See more on this blog post by me here.

New Bank Of England Paper On The Financial Balances Model For The United Kingdom

Stephen Kinsella is out with a new paper with co-authors Stephen Burgess, Oliver Burrows, Antoine Godin, and Stephen Millard published by the Bank of England.

From the paper:

Our paper makes two contributions to the literature. First, we develop, estimate, and calibrate the model itself from first principles as well as describing the stock-flow consistent database we construct to validate the model; as far as we know, we are the first to develop such a sophisticated SFC model of the UK economy in recent years.4 And second, we impose several scenarios on the model to test its usefulness as a medium-term scenario analysis tool. The approach we propose to use links decisions about real variables to credit creation in the financial sector and decisions about asset allocation among investors. It was developed in the 1980s and 1990s by James Tobin on the one hand, and Wynne Godley and co-authors on the other, and is known as the ‘stock-flow consistent’ (SFC) approach. The approach is best described in Godley and Lavoie (2012) and Caverzasi and Godin (2015) and underpins the models of Barwell and Burrows (2011), Greiff et al. (2011), and Caiani et al. (2014a,b). Dos Santos (2006) describes how SFC models incorporate detailed accounting constraints typically found in systems of national accounts. SFC models allow us to build a framework for the model where every flow comes from somewhere in the economy and goes somewhere, and sectoral savings/borrowings and capital gains/losses add or subtract from stocks of wealth/debt, following Copeland (1949). Accounting constraints allow us to identify relationships between sectoral transactions in the short and long run. The addition of accounting constraints is crucial, as one aspect of the economy we would like to model is the way it might react differently when policies such as fiscal consolidations are imposed slowly or quickly

4 Such models were popular in the past; for example Davis (1987a, 1987b) developed a rudimentary stock flow consistent model of the UK economy.

[The title of this page is the link]

Simon Wren-Lewis has an article on his blog on stock-flow consistent/coherent models by Wynne Godley. Unlike other articles, this has a more engaging tone and isn’t dismissive.

This is a good thing but it has the tone “Oh, there’s hardly anything new” about stock-flow consistent modeling and the sectoral balances approach. 🤦. To me this is highly inaccurate, to say the least. None of the models outside SFC models —with one exception—come anywhere close to the important question about what money is and how money is created. Even in the Post-Keynesian literature, while there are various non-mathematical approaches, there’s hardly anything that comes close. That important exception is the work of James Tobin as is summarized in his Nobel Prize lecture Money and Finance in the Macroeconomic Process. Except that Wynne Godley’s model greatly improve upon the deficiencies of Tobin’s approach.

The sectoral balances approach is a mini-version of stock-flow coherent modeling. Wren-Lewis seems to say there’s hardly anything great and don’t tell much. First, almost nobody was making a cri de coeur as much as Wynne Godley. Second, the approach makes it clear why a huge recession was coming. This is because US private expenditure was rising faster than private income and the US private sector was in deficit for long and the private sector was accumulating debt on a huge scale relative to income. It’s difficult to say when this would have reversed pre-2007, but had to reverse. Once this is reversed, i.e., when private expenditure slows relative to private income, so that the private sector goes into a surplus, output will fall as a result of a slowdown of private expenditure.

Moreover, the US economy had a critical imbalance in its trade with its current account balance of payments touching almost 6.5% at the end of 2005, hemorrhaging the circular flow of national income at a massive scale.

Wynne Godley’s argument was that because of the external imbalance, the US fiscal policy will be unable to expand output to full employment easily, once the US enters a recession. Hence, he proposed import controls for the United States.

None of anybody outside Wynne Godley’s circle came anywhere close to saying anything of this sort.

But these empirical analysis is a much more complicated discussion. At a simpler level, nobody has come closer to what stock-flow coherent models achieve. All we see is economists struggling with basic questions on how money is created, what role it plays and so on.

Wren-Lewis also criticises SFC models saying they have minimal behavioural hypothesis. Now, this is far from the truth. If you write stock-flow consistent models, which are more realistic, you’ll end up with having a lot of equations and parameters. Behaviour of each “sector” is articulated in these models. How money is created by the act of loan making by banks, to how households and firms accumulate assets and liabilities, to how firms making pricing decisions and how much they produce and how much households consume. In addition, the importance of fiscal policy is articulated: how governments make spending decisions, whether government expenditure can be thought of as exogenous and how in normal times—when politicians pay attention to how much the government’s deficit and debt it has—governement’s fiscal policy can be thought of as endogenous. And crucially, the supreme importance of the government’s finance in the financial assets/liabities creation process. While most economists stop at one time-step for the expenditure process, using stock-flow consistent models, you can see the full process. Moreover, the analysis highlights the correct direction of causalities. A good example is the direction of causation from prices to money.

I want to however highlight another important point. A lot about how the economy works can be understood without going too much into behaviour. Just national accounts, flow of funds and a minimal set of behavioural assumptions would be a great progress. The rest of the profession however struggles to even understand basic flow of funds. A lot can be understood because most of the times, economists are erring on basic accounting. Hence their story doesn’t add up and produces something completely unrelated to the real world. If only economists understood this, that’ll be a lot of progress. Stock-flow consistent models are rich in behavioral analysis but even without it, understanding flow of funds with a minimal set of assumptions is the right direction.