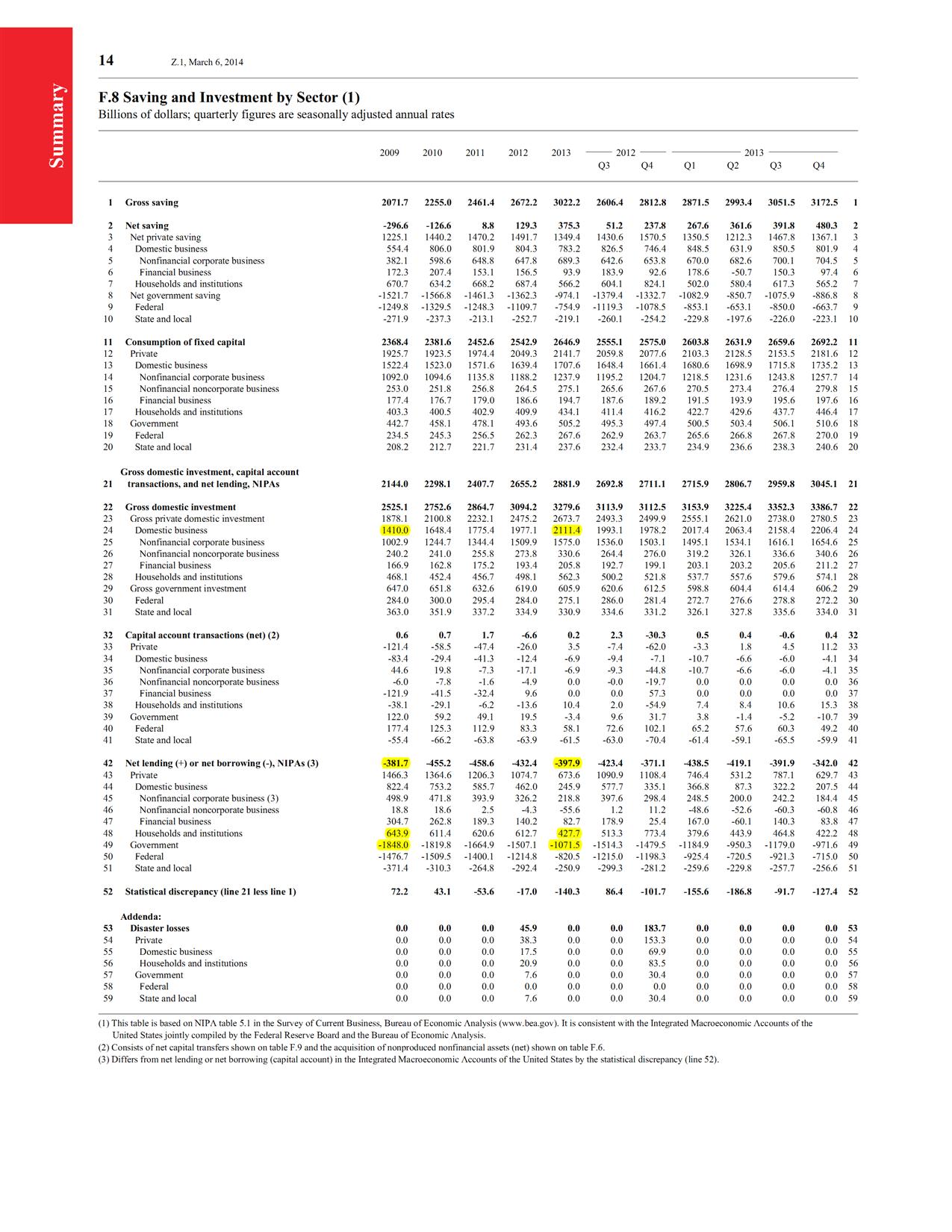

The recent Bank of England quarterly bulletin has interested blogosphere into what goes on to determine the stock of money.

Money can mean various things and here I restrict to the the monetary aggregates as defined by central banks – as in the referred publication. But whoever is interested in “money creation” also becomes interested in the creation of assets and liabilities, so the right question is more general.

As I had pointed out in my previous post, the Bank of England articles seriously ignore the role of fiscal policy. Winterspeak also mentions this.

So what is the answer? In my view the most systematic way of saying this via Tobin’s theory asset allocation, improved drastically by stock-flow consistent models of Godley and Lavoie.

Also there are two things – influence and determination. For example, something can have an influence on the stock of money but may not determine it.

Since economies are highly dynamic it is not easy to answer this in a single sentence but it can perhaps be said that fiscal policy, private expenditure and QE influence the stock of money but it is ultimately determined by the holders of wealth.

Of course since people generally have a Monetarist intuition, the right notion that fiscal policy, private expenditure and QE influencing the determination of the stock of money is incorrectly taken by people to mean that QE has the same effect as a fiscal expansion. Which of course QE does not.

First take private expenditure. Since we know that “loans create deposits” it can be suspected that bank credit has an influence on money. Of course this process is more dynamic as the expenditure has its own multiplier effect (not to be confused with the money mulplier!) on output and income. But bank credit determining the stock of money is stretching too much. For example, while a bank makes a house loan and creates deposits in the process, the process of securitization reduces the stock of money as ultimate buyers of the securized products exchange money with the mortgage-backed securities (MBS). And of course there’s the reflux mechanism via which economic units may reduce their debts toward the banking system.

Now take fiscal policy. Like private expenditure, government expenditure and taxes also influence the level of aggregate demand. This has an influential effect on credit creation via effect of increased output and income on private expenditure and via the process highlighted in the previous paragraph this has an influence on the determination of the stock of money.

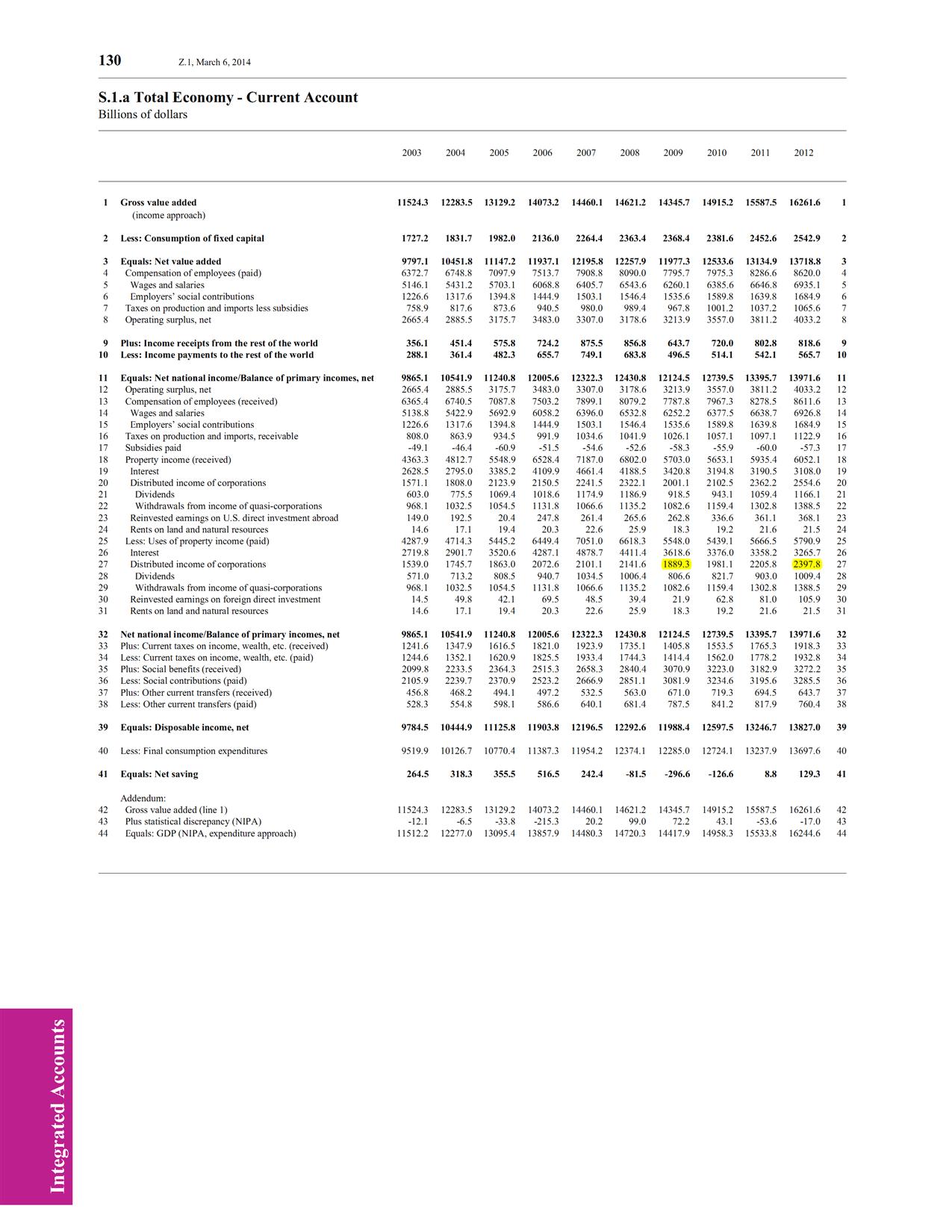

Also, while economic units are earning and making decisions on spending, they are also accumulating financial and non-financial assets. So they have a preference on how much of their wealth they allocate into each asset. A Monetarist would talk of an excess supply of money and this raising prices of goods and services and bringing the demand and supply of money into equivalence. But there is no need for this from an endogenous money perspective. One can have the equivalence brought about by adjustments of prices of financial assets and also adjustment of quantities of assets and liabilities held by various economic units such as banks. This is where the importance of the work of Tobin’s theory of asset allocation comes in.

Now let’s discuss QE. Large scale purchases of financial assets by the central bank – although influences the stock of money, doesn’t determine it. Also QE doesn’t have a direct influence on aggregate demand like private or public expenditure. It has indirect effects via raising prices of financial assets (which can be described by Tobin’s theory of asset allocation) and inducing capital gains and a wealth effect on consumption. The Monetarist intuition highly exaggerates the effect.

The point of my writing the post was to show that fiscal policy has a strong effect on influencing the stock of money. This happens via the strong effect of fiscal policy on output and income inducing private expenditure. Of course private expenditure needn’t be only induced and has an autonomous nature as well, so both fiscal policy and private expenditure have an effect. The effect is via a rise in output and income and this leading to a rise in wealth and economic units allocating a fraction of their increased wealth into ‘money’ (as in currency notes and deposits).

So Winterspeak is right in pointing out the incorrect statement of the Bank of England paper:

The amount of money created in the economy ultimately depends on the monetary policy of the central bank. In normal times, this is carried out by setting interest rates.

The above quote is suggestive of a very strong influence of interest rates on private expenditure, ignores the autonomous nature of private expenditure and the role of fiscal policy.

Nick Rowe defends textbook economics over his blog and suggests some influence of QE on prices via the Monetarist hot potato process where there is an excess supply of money and via a non-equilibrium process leads to a rise in prices of good and services! But in this he mixes asset allocation decisions with expenditure decisions, as if the two can be treated as the same. In the market for goods and services, producers set the price based on costs and their markups. So it is hard to see the influence. The supplies and demands of assets are actually brought into equivalence in the financial markets rather than the market for goods and services. He may have a point but the degree to which this has an effect is low. So holders of wealth may allocate some of their portfolio into commodity funds (after having sold their bonds to the central bank) which may buy commodities in exchanges and expectations due to a price rise and speculation and myths may cause a price rise but this is quite different from his suggested dynamics. Or it may have an effect via a depreciation of the currency and change in the consumer price index due to a change in prices of foreign goods. The question then is to what extent do what economists stress are important are actually important.

Needless to say, the usual story from money to other things is misleading. The point however is that “how money is created” is a good starting point to understand macroeconomics.