PSL Quarterly Review has a new series Recollections Of Eminent Economists and Anthony Thirlwall has the inaugural contribution.

Abstract:

The paper is the first inaugural contribution to the new series of “Recollections of Eminent Economists”. Under this name, the previous series of the journal (then called “Banca Nazionale del Lavoro Quarterly Review”) used to publish autobiographic essays in which renowned economists described their scientific path and reflected on the recent developments of the discipline. In this work, A.P. Thirlwall recalls his personal and academic biography, ranging from employment in the UK to consultancy work in developing countries, and comments on the reception of his main works. Among the latter, special attention is paid to regional and development economics, as well as to the relation between the balance of payments and economic growth. Throughout the discussion, the author emphasizes the Keynesian inspiration of his analyses.

The General Theory of Employment, Interest and Money was published in January, 1936.

Meanwhile, … , Michal Kalecki had found the same solution.

His book, Essays in the Theory of Business Cycles, published in Polish in 1933, clearly states the principle of effective demand in mathematical form. At the same time he was already exploring the implications of the analysis for the problem of a country’s balance of trade, along the same lines that I followed in drawing riders from the General Theory in essays published in 1937.

The version of his theory set out in prose (published in ‘Polska Gospodarcza’ No. 43, X, 1935) could very well be used today as an introduction to the theory of employment.

He opens by attacking the orthodox theory at the most vital point – the view that unemployment could be reduced by cutting money wage rates. And he shows (a point that Keynesians came to much later, and under his influence) that , of monopolistic influences prevent prices from falling when wage costs are lowered, the situation is still worse, because reduced purchasing power causes a fall in sales on consumption goods …

…

Michal Kalecki’s claim to priority of publication is indisputable.

– Joan Robinson, Kalecki And Keynes in Essays In Honour Of Michal Kalecki, 1964.

Jan Toporowski’s intellectual biography, volume 2 of Michał Kalecki is out now.

Ashwani Saith has a fine biography of Ajit Singh for Ajit Singh (1940–2015), The Radical Cambridge Economist: Anti‐Imperialist Advocate Of Third World Industrialization for the latest issue of Development And Change.

The article highlights how his worldview and work was quite close to Nicky Kaldor.

Ajit Singh died on 23 June 2015 and there’s also a fine obituary on him in The Guardian by John Eatwell.

F.M. Scherer had a nice biography in the Palgrave Companion To Cambridge Economics.

Recently Paul Krugman wrote up an article, Globalization: What Did We Miss? for the IMF globalisation conference last fall. The paper is a large concession to the points some economists have been making on international trade and globalisation. Krugman concedes that:

soaring imports did impose a significant shock on some U.S. workers, which may have helped cause the globalization backlash.

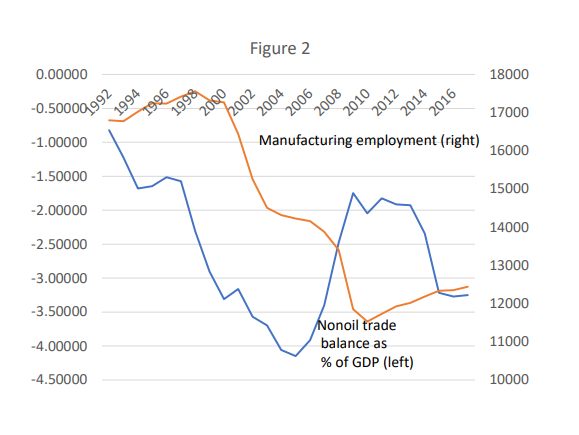

He also draws this chart, coming to the view that the US trade has led to a weakness of manufacturing.

The New Consensus narrative is that loss of employment is due to productivity rises and not due to international trade. Now Krugman has accepted the view that it is the latter.

Further, he also says:

Until the late 1990s employment in manufacturing, although steadily falling as a share of total employment, had remained more or less flat in absolute terms. But manufacturing employment fell off a cliff after 1997, and this decline corresponded to a sharp increase in the nonoil deficit, of around 2.5 percent of GDP.

Does the surge in the trade deficit explain the fall in employment? Yes, to a significant extent. A trade deficit doesn’t produce a one-for-one decline in manufacturing value added, since a significant share of both exports and imports of goods include embodied services. But a reasonable estimate is that the deficit surge reduced the share of manufacturing in GDP by around 1.5 percentage points, or more than 10 percent, which means that it explains more than half of the roughly 20 percent decline in manufacturing employment between 1997 and 2005.

Again, this is over a relatively short time period and focuses on absolute employment, not the employment share. Trade deficits explain only a small part of the long-term shift toward a service economy. But soaring imports did impose a significant shock on some U.S. workers, which may have helped cause the globalization backlash.

And trade deficits are, as I said, part of a broader story of adjustment issues.

Manufacturing is important partly because of increasing returns to scale and partly because it’s easier to export manufactures, although services are catching up.

Further, he quotes the work of Autor, et. al.:

This is where the now-famous analysis of the “China shock” by Autor, Dorn, and Hanson (2013) comes in. What ADH mainly did was to shift focus from broad questions of income distribution to the effects of rapid import growth on local labor markets, showing that these effects were large and persistent. This represented a new and important insight.

To make partial excuses for those of us who failed to consider these issues 25 years ago, at the time we had no way of knowing that either the hyperglobalization shown in Figure 1 or the trade deficit surge shown in Figure 2 were going to happen. And without the combination of these developments the “China shock” would have been much smaller. Still, we missed an important part of the story.

But concessions of previous held orthodox views are hardly straightforward. Despite this large concession, Krugman still wants to defend free trade and is against any tariffs. One may critique selective protectionism but there is also the option of imposing tariffs non-discriminately, i.e., non-selective protectionism.

More importantly, as Joan Robinson often stressed the thesis of free trade ought to also come with the answer to the question: what is the mechanism for resolving imbalances? Free traders always avoid this question, sometimes claiming—as Milton Friedman did—that floating exchange rates does the trick. But we know that it’s hardly the case. In the absence of any market mechanism, we need an official mechanism.

At their blog, in an article titled The Economic Scars of Crises and Recessions, the IMF is now conceding that demand affects supply and that all types of recessions lead to a permanent damage to the supply side. This is known in Post-Keynesian literature as the endogeneity of the natural rate of growth.

Earlier it was thought by them that these are temporary and the economy recovers to its pre-recession trend.

In a 2016 article for the INET, Marc Lavoie had argued how these ideas were new to the mainstream but well known in the heterodox literature.

These are not special to just recessions, as the IMF authors seem to be arguing but is happening continuously, even outside recession. The 2002 paperThe Endogeneity Of The Natural Rate Of Growth by Miguel A. León‐Ledesma and A. P. Thirlwall for the Cambridge Journal Of Economics is a great reference.

If there’s full employment, the rate of growth of GDP is equal to the rate of growth of the labour force plus the rate of growth of productivity. This is Harrod’s natural rate of growth. Unlike the natural rate of interest or of unemployment, this is not vacuous. Of course, below full employment, an economy can grow faster, although the actual rate of growth depends on demand always. We also know that the rate of growth of productivity depends itself on the rate of growth of the GDP. So that implies that the natural rate of growth is endogenous.

From the León‐Ledesma-Thirlwall paper:

The question of whether the natural growth rate is exogenous or endogenous to demand, and whether it is input growth that causes output growth or vice versa, lies at the heart of the debate between neoclassical growth economists on the one hand, who treat the rate of growth of the labour force and labour productivity as exogenous to the actual rate of growth, and economists in the Keynesian/post-Keynesian tradition, who maintain that growth is primarily demand driven because labour force growth and productivity growth respond to demand growth, both foreign and domestic. The latter view does not imply, of course, that demand growth determines supply growth without limit; rather, that aggregate demand determines aggregate supply over a range of full employment growth rates, and that in most countries demand constraints (related to excessive inflation and balance of payments disequilibrium) tend to bite long before supply constraints are ever reached.

Ashoka Mody has a fine articleThe Euro Area’s Deepening Political Divide on VoxEU on how recent national elections in Germany and Italy suggest that people of Europe are drifting apart.

He also gives a historical context to what voters think. For example, he says:

And in September 1992, the French public came within a whisker of rejecting the single currency.

The voting pattern in the French referendum eerily foreshadowed recent political protests. Those who voted against the single currency tended to have low incomes and limited education, they lived in areas that were turning into industrial wastelands, they worked in insecure jobs, and, for all these reasons, they were deeply worried about the future (Mody 2018: 101–103). By voting against the Maastricht Treaty, they were not necessarily expressing an anti-European sentiment; rather, they were demanding that French policymakers pay more attention to domestic problems, which European institutions and policies could not solve.

He also has a new book, Eurotragedy – A Drama In Nine Acts, soon.

In his article, Mody also refers to Kaldor’s prescience from his article The Dynamic Effects Of The Common Marketfirst published in the New Statesman, 12 March 1971 and also reprinted (as Chapter 12, pp 187-220) in Further Essays On Applied Economics – volume 6 of the Collected Economic Essays series of Nicholas Kaldor. You can read some quotes from this article here.

Basil Moore passed away recently, as I mentioned a few days back in this blog.

One of the criticisms of Moore’s work was the passive role of banks. Louis-Philippe Rochon has an excellent article in his Festschrift Complexity, Endogenous Money and Macroeconomic Theory — Essays in Honour Of Basil J. Moore, Edward Elgar, 2006, to further develop Moore’s views.

Below is the scan of the full article, provided to me by LP for posting here.

The object below is an embed of the pdf. If the embed doesn’t display, or to get a better view, you can open it in a separate browser tab here.

Nick Edmonds commented on my post Wynne Godley And Non-Selective Protectionism—which documented all the references where Wynne Godley proposes the usage of the Article XII of the GATT—pointing out that the Article XII of the GATT can only be invoked reserve assets are under threat.

Hence it is difficult for the United States to invoke it. I agree with this. It’s looks more designed for nations who accumulate reserve assets and for whom sales of reserve assets is an important way to finance current account deficits. The U.S. has some reserve assets but is under no imminent threat. (And it finances its current account deficit mainly by net incurrence of liabilities instead of sale of reserve assets).

Under the rules of the WTO, any trade restriction taken by a Member must be consistent, or in compliance, with the rules of the international trading system. Under the provisions of Article XII, XVIII:B and the “Understanding of the Balance-of-Payments Provisions of the GATT 1994”, a Member may apply import restrictions for balance-of-payments reasons.

GATT: Articles XII and XVIII:B

Article XII and XVIII:B in their current form were redrafted in 1957 by the Working Party on Quantitative Restrictions. At that time, balance-of-payments measures referred to quantitative restrictions and were an exception to Article XI which prohibits the use of quantitative restrictions. Article XII can be invoked by all Members and Article XVIII:B by the developing country Members (defined as those in the early stages of development and with a low standard of living.

The basic condition for invoking Article XII is to “safeguard the [Member’s] external financial position and its balance-of-payments”; Article XVIII:B mentions the need to “safeguard the [Member’s] external financial position and ensure a level of reserves adequate for the implementation of its programme of economic development”. Both Articles refer to the need to “restore equilibrium on a sound and lasting basis”. While Article XII mentions the objective of “avoiding the uneconomic employment of resources”, Article XVIII:B refers to “assuring an economic employment of production resources”.

Article XVIII:B contains somewhat less stringent criteria than Article XII. Article XII (para. 2)states that import restrictions “shall not exceed those necessary (i) to forestall the imminent threat of, or to stop, a serious decline in its monetary reserves” or (ii) “…in the case of a contracting party with very low monetary reserves, to achieve a reasonable rate of increase in its reserves”.

Article XVIII:B (para. 9) omits the word “imminent” from the first condition and refers to an “inadequate” level rather than a “very low” level of reserves; “adequate” is defined as “adequate for the implementation of its programme of economic development”.

Both Articles require Members to progressively relax the restrictions as conditions improve and eliminate them when conditions no longer justify such maintenance.

The 1979 Declaration

After the Tokyo Round, the 1979 Declaration on Trade Measures Taken for Balance-of-Payments Purposes (BISD 26S/205) extended the disciplines to all trade measures imposed for balance-of-payments reasons, not just quantitative restrictions. Thus all trade measures taken for balance-of-payments purposes come within the purview of notification and consultation requirements.

The 1979 Declaration introduced three new conditions for the application of balance-of-payments measures: (i) that preference shall be given to the measure which has “the least disruptive effect on trade” while abiding by disciplines provided for in the GATT; (ii) that the simultaneous application of more than one trade measure for balance-of-payments purposes shall be avoided; and (iii) that “whenever practicable, contracting parties shall publicly announce a time schedule for the removal of the measures”. It also spelled out that measures should not be taken “for the purpose of protecting a particular industry or sector”.

…

I am sure Wynne was aware of this, so it’s curious why he mentions it over the years. If anyone knows, I’ll be grateful!

Post-Keynesian economics greatly influenced Post-Keynesian monetary theory. Although his work was present in Cambridge Keynesians work, such as Joan Robinson, Nicholas Kaldor, Wynne Godley and Francis Cripps, they didn’t influence the thinking on monetary matters as much as Moore did with his great book Horizontalists And Verticalists — The Macroeconomics Of Credit Money.

He does recognise Kaldor’s work in that book:

The obvious lesson to be learned from the experience with the General Theory in the past fifty years is that .. revolutionizing the way the world thinks about economic problems” is an enormously difficult task. In spite of the mountains of Keynesian exegesis that has been produced, Nicholas Kaldor was the sole English-speaking economist of the first rank to have endorsed what is here termed the Horizontalist position (1970, 1981, 1982, 1983, 1985a, b). This book represents my attempt to enlist the support of other scholars in what has at times seemed a quixotic crusade by a member of the lunatic fringe against the prevailing orthodoxy.

I regret not having met him. My only interaction was to ask him via email, where I can buy his book Horizontalists And Verticalists because it cost $450 on Amazon at the time! He didn’t know but replied recommending his book Shaking the Invisible Hand: Complexity, Endogenous Money and Exogenous Interest Rates. But later I managed to get the book. He also said that

It was my attempt to introduce endogenous money into the Macro literature, but no one has heard of it since the mainstream never reviewed it. (They gave H&V to Phil Kagan, a leading Monetarist, who didn’t much like it, but at least it was reviewed.

Noechartalists will be surprised to know that Moore also endorsed Chartalism in his 1988 book:

[page 8] Soft or fiat money refers to unbacked paper or token coins. It maintains its value because it is legally tenderable (by fiat) in settlement of debts and taxes.

…

[page 18] Currency (fiat money) is the physical embodiment of the n,onetary unit of account (numeraire) defined by the sovereign government. It is a sure and perfectly liquid store of value in units of account. It is legal tender for the payment of taxes and for the discharge of private debt obligations enforceable in courts of law. In consequence it is generally accepted as a means of payment.

…

[page 294] Money of any kind allows the breaking of the barter quid pro quo that is imposed by lack of trust and for which money is not a substitute. Even though intrinsically worthless, money is acceptable to me provided that it is also acceptable to you and to everyone else. Trust in money now comes from government guarantee of its acceptability as legal tender. “Today all civilized money is beyond the possibility of dispute, chartalist” (JMK, 5, p. 4).

…

[page 372] Fiat money represents a bridge between the world of commodity money and credit money. In its liquidity characteristics it is virtually identical to commodity money, except that it is chartalist.

There were many places I disagreed with Moore. I don’t think he was a fan of the use of expansionary fiscal policy. I don’t know why he claimed that the Keynesian multiplier doesn’t exist. But as Geoff Harcourt says in the foreword to the book Complexity, Endogenous Money and Macroeconomic Theory — Essays in Honour Of Basil J. Moore:

But, important as these contributions have been, Basil has influenced many other topics, sometimes by his innovative thinking, sometimes by being the irritant that has led other oysters to create pearls of their own. Especially is this true of his highly individual approach to the true meaning of the Keynes–Kahn–Meade multiplier concept and also to the validity of Keynes’s concept of effective demand as presented in The General Theory. Basil has made us think anew about our understanding of the natures of saving and investment, their relationship to each other, to the concept of an under-employment rest state, and also of the relationship of the macroeconomic income and expenditure accounts, balance sheets and funds statements to the behavioral relationships originally developed by Keynes and his followers. To sometimes disagree with Basil’s arguments is not at all to detract from the great stimulus he has provided for fundamental rethinks of basic, central, core concepts and relationships.

Post-Keynesian Economics has lost a giant. R.I.P., Basil Moore.