The General Theory of Employment, Interest and Money was published in January, 1936.

Meanwhile, … , Michal Kalecki had found the same solution.

His book, Essays in the Theory of Business Cycles, published in Polish in 1933, clearly states the principle of effective demand in mathematical form. At the same time he was already exploring the implications of the analysis for the problem of a country’s balance of trade, along the same lines that I followed in drawing riders from the General Theory in essays published in 1937.

The version of his theory set out in prose (published in ‘Polska Gospodarcza’ No. 43, X, 1935) could very well be used today as an introduction to the theory of employment.

He opens by attacking the orthodox theory at the most vital point – the view that unemployment could be reduced by cutting money wage rates. And he shows (a point that Keynesians came to much later, and under his influence) that , of monopolistic influences prevent prices from falling when wage costs are lowered, the situation is still worse, because reduced purchasing power causes a fall in sales on consumption goods …

…

Michal Kalecki’s claim to priority of publication is indisputable.

– Joan Robinson, Kalecki And Keynes in Essays In Honour Of Michal Kalecki, 1964.

Michal Kalecki swam into my ken just after the publication of the General Theory of Employment, Interest and Money, in 1936. The small group who had been working with Maynard Keynes during the gestation of the book understood what it was about, but amongst the public as a whole it was still a mystery. Kalecki, however, knew it all. He had taken a year’s leave from the institute where he was working in Warsaw to write the theory of employment but Keynes’ book came out, and got all the glory. Michal never made any claim for himself and I made it my business to blow his trumpet for him, but most of the profession (including Keynes) just thought that I was being kind to a lame duck. Only since the publication of his essays written in Polish from 1933 to 1935 has it been generally recognized that he had already worked out all the essentials of what became known as Keynes’ theory (Selected Essays on the Dynamics of the Capitalist Economy, Cambridge University Press, 1971). He showed that it is investment, not private saving, that brings about capital accumulation; that a government deficit, in a slump, will increase employment; that cutting wages only makes the slump worse; that the rate of interest depends upon supply and demand of the stock of money, not on the flow of saving, and that it is the forward-looking expectation of profits that induces firms to accumulate.

The question of glory did not seem to me to be important. As Michal was the first to admit, his ideas would have taken a long time to establish while with Keynes they burst upon the world as a revolution. But I was deeply impressed by the fact that two thinkers of such different background and habits of thought could arrive at the same diagnosis of the economic situation. Logic is the same for everybody; the same logical structure, if it is not fudged, can support quite different ideologies, but for most social scientists ideology leaks into the logic and corrupts it.

In the natural sciences, it is common enough for the same discovery to come almost simultaneously from two independent sources. The general development of a subject throws up a new problem and two equally original minds find the same answer, which turns out to be validated by further work. In the history of economic thought, the case of the discovery of the theory of employment by Keynes and Kalecki is unique.

– Joan Robinson in PORTRAIT: Michal Kalecki, Challenge, Vol. 20, No. 5, November/December, 1977, pp. 67-69, http://www.jstor.org/stable/40719591

This quote of Abba Lerner from his article “The Burden of the National Debt,” in Lloyd A. Metzler et al.,Income, Employment and Public Policy (New York, 1948), p. 256 is frequently quoted in the Post-Keynesian blogosphere:

One of the most effective ways of clearing up this most serious of all semantic confusions is to point out that private debt differs from national debt in being external. It is owed by one person to others. That is what makes it burdensome. Because it is interpersonal the proper analogy is not to national debt but to international debt…. There is no external creditor. “We owe it to ourselves.”

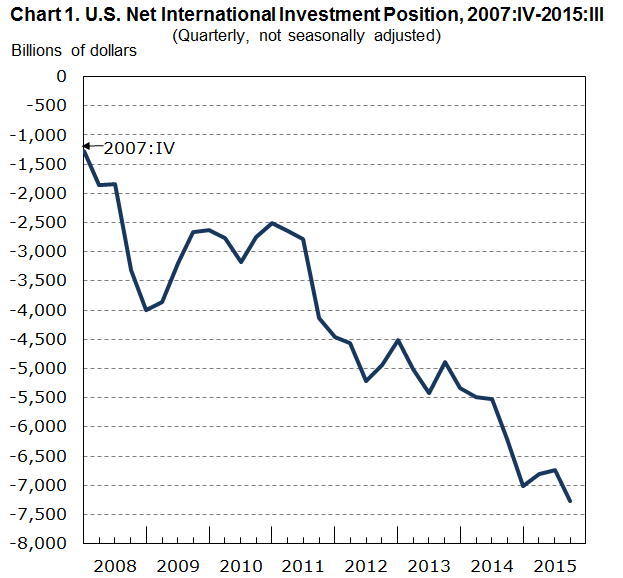

This is unfortunately inconsistent with his “functional finance”. Abba Lerner clearly says that external debt can be problematic. However he probably never realized that if his advise is followed in running fiscal policy, a nation’s balance of payments will deteriorate and its international debt will increase (because current account balance adds to the net international investment position).

Public debt is not the same the negative of the net international investment position but it’s related as the external debt is directly or indirectly picked up by the public sector.

Sound finance is all junk science but Abba Lerner is not your friend to learn about money, debts, deficits and all that.

A recommended reading is Robert Blecker’s international economics written for The Elgar Companion to Post Keynesian Economics edited by John E. King.The chapter can be previewed from Amazon.

One interesting aspect is the distribution of income between profits and wages. Blecker says:

Post Keynesian in the Kaleckian tradition emphasize the feedback effects of international competition onto domestic profit mark-up rates and hence on the distribution of income between profits and wages. When a currency appreciates (or domestic costs rise relative to foreign), oligopolistic firms squeeze price-cost margins in order to ‘price-to-market’, which in turn leads to a fall in the profit share with possible negative repercussions for investment and growth (although this may be offset by boost to domestic consumption arising from higher real wages and labour income). When a currency depreciates (or domestic costs fall relative to foreign), the opposite happens as domestic oligopolies are able to raise their price-cost margins without losing market share, income is distributed from wages to profits, and the potential repercussions for investment and growth and consumption are all reversed. Outcomes in which a redistribution of income towards wages is expansionary are known as ‘wage-led’ regimes, while outcomes in which a redistribution towards profits is expansionary are ‘profit-led’. Mainstream economists have recognized the flexibility of profit margins in response to exchange-rate fluctuations – what they call ‘partial pass-through’ – but they have not analysed the feedback effect onto income distribution, aggregate demand and economic growth.

where Snational and Inational are national saving and national investment and CAB is the current account balance of international payments. In calculating national saving and investment, one adds saving and investment, respectively, of all resident sectors of the economy.

However, an accounting identity shouldn’t be confused with behavioural relationships.

Steven Roach is a good economist and it’s sad to see him confusing this. In a recent article for Project Syndicate titled America’s Trade Deficit Begins at Home, he uses this identity to conclude that if America wants to reduce her trade deficit, the solution is more saving.

Roach says:

What the candidates won’t tell the American people is that the trade deficit and the pressures it places on hard-pressed middle-class workers stem from problems made at home. In fact, the real reason the US has such a massive multilateral trade deficit is that Americans don’t save.

Total US saving – the sum total of the saving of families, businesses, and the government sector – amounted to just 2.6% of national income in the fourth quarter of 2015. That is a 0.6-percentage-point drop from a year earlier and less than half the 6.3% average that prevailed during the final three decades of the twentieth century.

Any basic economics course stresses the ironclad accounting identity that saving must equal investment at each and every point in time. Without saving, investing in the future is all but impossible.

A little thought on behavioural relationships tell a different story. The main causality connecting accounting identities is behaviour of demand and output at home and abroad. While it is true that by accounting identity, the U.S. current account balance will improve by more saving (such as households saving more, firms retaining higher earnings and government (both at the federal and state level) attempting to increase its saving tighten fiscal policy, it happens via a contraction of output.

Wynne Godley was one who stressed this before the crisis. In his paperThe United States And Her Creditors: Can The Symbiosis Last? written with Dimitri Papadimitrou, Claudio Dos Santos and Gennaro Zezza, this is made clear:

A well-known accounting identity says that the current account balance is equal, by definition, to the gap between national saving and investment. (The current account balance is exports minus imports, plus net flows of certain types of cross-border income.) All too often, the conclusion is drawn that a current account deficit can be cured by raising national saving—and therefore that the government should cut its budget deficit. This conclusion is illegitimate, because any improvement in the current account balance would only come about if the fiscal restriction caused a recession. But in any case, the balance between saving and investment in the economy as a whole is not a satisfactory operational concept because it aggregates two sectors (government and private) that are separately motivated and behave in entirely different ways. We prefer to use the accounting identity (tautology) that divides the economy into three sectors rather than two—the current account balance, the general government’s budget deficit, and the private sector’s surplus of disposable income over expenditure (net saving)—as a tool to bring coherence to the discussion of strategic issues. It is hardly necessary to add that little or nothing can be learned from these financial balances measured ex post until we know a great deal more about what else has happened in the economy—in particular, how the level of output has changed

[boldening: mine]

This was pre-crisis from a few who were avowed Keynesians all their life! It’s unfortunate to see Steve Roach make an error even after so many years into the global economic and financial crisis. One should study Keynes seriously. While I am sure Roach appreciates the paradox of thrift, he forgets applying it to the analysis of United States of America’s trade deficits.

This is the basis of the doctrine of the ‘foreign trade multiplier’, according to which the production of a country will be determined by the external demand for its products and will tend to be that multiple of such demand which is represented by the reciprocal of the proportion of internal incomes spent on imports. This doctrine asserts the very opposite of Say’s Law: the level of production will not be confined by the availability of capital and labour; on the contrary, the amount of capital accumulated, and the amount of labour effectively employed at any one time, will be the result of the growth of external demand over a long series of past periods, which permitted the capital accumulation to take place that was required to enable the amount of labour to be employed and the level of output to be reached which were (or could be) attained in the current period.

Keynes, writing in the middle of the Great Depression of the 1930s, focused his attention on the consequences of the failure to invest (due to unfavourable business expectations) in limiting industrial employment below industry’s attained capacity to provide such employment; and he attributed this failure to excessive saving (or an insufficient propensity to consume) relative to the opportunities for profitable investment. Hence his concentration on liquidity preference and the rate of interest, as the basic cause for the failure of Say’s Law to operate under conditions of low investment opportunities and/or excessive savings, and the importance he attached to the savings/investment multiplier as a short-period determinant of the level of production and employment.

On retrospect I believe it to have been unfortunate that the very success of Keynes’s ideas in connection with the savings/investment multiplier diverted attention from the ‘foreign trade multiplier’, which, over longer periods, is a far more important and basic factor in explaining the growth and rhythm of industrial development. For over longer periods Ricardo’s presumption that capitalists only save in order to invest, and that hence the proportion of profits saved would adapt to changes in the profitability of investment, seems to me more relevant; the limitation of effective demand due to oversaving is a short-run (or cyclical) phenomenon, whereas the rate of growth of’external’ demand is a more basic long-run determinant of both the rate of accumulation and the growth of output and employment in the ‘capitalist’ or ‘industrial’ sectors of the world economy.

– Nicholas Kaldor, Capitalism and industrial development: some lessons from Britain’s experience, Camb. J. Econ. (1977)1 (2):193–204, link

The definition of saving is wrong. Saving is equal to income minus expenditure.

That’s not an exaggeration. He actually says it:

… Since saving = income – expenditures, [aggregate] saving must equal zero.

Steve Keen on Twitter supports Steve Roth.

click to view the tweet on Twitter

What’s with economists’ dislike for national accounts?

Steve Roth uses the phrase “savings” as a stock. Obviously his claim is just wrong as we know from national accounts:

Change in net worth = Saving + Holding Gains.

(with netting in holding gains).

Steve Keen doesn’t use saving as a stock but as a flow and a plural of saving. But Steve Keen’s point is also wrong. National saving is equal to the sum of saving of all economic units, such as households, firms, government etc. Even the household sector’s propensity to save collectively matters. That’s what macroeconomics is all about.

Now moving the more important point: is it possible that a higher propensity to consume reduces the long run rate of accumulation?

There are several Post-Keynesian economists who have considered the possibility. Of course it should be contrasted with supply side neoclassical economics. A few are Basil Moore, Wynne Godley, Marc Lavoie, and Gérard Duménil and Dominique Lévy as mentioned at the beginning of this post.

We quickly discovered that the model could be run on the basis of two stable regimes. In the first regime, the investment function reacts less to a change in the valuation ratio-Tobin’s q ratio-than it does to a change in the rate of utilization. In the second regime, the coefficient of the q ratio in the investment function is larger than that of the rate of utilization (γ3 > γ4). The two regimes yield a large number of identical results, but when these results differ, the results of the first regime seem more intuitively acceptable than those of the second regime. For this reason, we shall call the first regime a normal regime, whereas the second regime will be known as the puzzling regime. The first regime also seems to be more in line with the empirical results of Ndikumana (1999) and Semmler and Franke (1996), who find very small values for the coefficient of the q ratio in their investment functions, that is, their empirical results are more in line with the investment coefficients underlying the normal regime.

… In the puzzling regime, the paradox of savings does not hold. The faster rate of accumulation initially encountered is followed by a floundering rate, due to the strong negative effect of the falling q ratio on the investment function. The turnaround in the investment sector also leads to a turnaround in the rate of utilization of capacity. All of this leads to a new steady-state rate of accumulation, which is lower than the rate existing just before the propensity to consume was increased. Thus, in the puzzling regime, although the economy follows Keynesian or Kaleckian behavior in the short-period, long-period results are in line with those obtained in classical models or in neoclassical models of endogenous growth: the higher propensity to consume is associated with a slower rate of accumulation in the steady state. In the puzzling regime, by refusing to save, households have the ability over the long period to undo the short-period investment decisions of entrepreneurs (Moore, 1973). On the basis of the puzzling regime, it would thus be right to say, as Dumenil and Levy (1999) claim, that one can be a Keynesian in the short period, but that one must hold classical views in the long period.

So there is a possibility that a higher propensity to consume leads to a lower growth in the long run. I do not think this is generally true, but this could be possible in some economies.

Two conclusions. It’s counter-productive to mix the definition of saving and what’s called “net lending” in national accounts. It’s possible (which shouldn’t mean that it’s necessarily the case) that Keynes’ paradox of savings doesn’t hold in the long run. I don’t believe that’s the case but purely arguing using national accounts and/or changing definitions won’t do.

Eric Lonergan has written an interesting post about US trade deficits on his blog Philosphy Of Money/Sample Of One. In the post Eric claims that the United States is not a debtor of the world but that she is a creditor of the world! Eric also says that a lot of talk of all this is conventional wisdom and in reality the United States is getting paid to have lunch.

First, it’s no conventional wisdom. Most of standard macroeconomics is simply denying the importance of balance of payments. It is held that market mechanisms will correct imbalances, if only the government does its job. So there’s no conventional wisdom worrying about the trade deficit of the United States of America. It is exactly the opposite – a heterodox view.

Second, there is no “free lunch”. Imports put a drain on demand and output and because of the imbalance of the U.S. trade, full employment has been a distant dream. With so much of unemployment (especially in the crisis) and the slow recovery, one cannot claim that the U.S. has some free lunch. Only if there is full employment and that too remaining sustainable, can one claim that there’s some “free lunch”. A smaller point is that one needs the correct counter-factual: if the U.S. trade deficit had been lower, interest income (one of Eric’s main points) would have been even higher. So one more reason to avoid the phrase “free lunch”.

Moving to more important points. Eric claims that net return of FDI is high and hence BEA’s numbers are not right. Specifically he claims:

So here’s the crux: American generates a high positive net income from its net international asset position – which implies its net external asset position is a positive number. Despite running permanent current account deficits, the US has accumulated net external assets. this sounds less counterintuitive if you think that all it means is that US assets oversees are more valuable than foreign holdings of US assets.

To highlight how significant the difference is, BEA measures of US net external liabilities are around $7trn, if we simply value the net income on a PE multiple of 14x, the net external assets of the US are around $2.7trn!

An inconsistency this large seems extreme, but consider the valuation of foreign direct investment (FDI). According to the BEA, net FDI of the US has a value of less than $1trn, although the US earns $424bn on its overseas FDI and foreign FDI in the US only earns $153bn. If we value both income streams on 14x earnings, the US has net FDI assets of $4.2trn – the BEA ‘market value’ estimates are out by $3trn.

Now, that is not a correct way to approach this. To see the error, assume the stock of outward FDI is $100 and the stock of inward FDI is also $100 at market prices. Suppose investment receipts is $10 and income paid is $9. So it looks like the United States is earning $1 on a net FDI of 0. So according to this argument, the return is infinite!

It is better to look at the actual numbers:

Stocks

Outward FDI: $6,695bn

Inward FDI: $6,196 bn.

Flows

Direct investment income: $776bn

Direct investment payments $592bn.

There is nothing drastically wrong about these numbers. Perhaps, it can be argued that direct investment in the US by foreigners will take time to pay off, or that foreigners are satisfied with this or something else. These numbers do not appear wrong.

Netting inward and outward and comparing returns to the net stock is an invalid argument, as I showed above with an example of inward/outward FDI of $100.

In addition, on Twitter Eric says a DCF (discounted cash flow) model also supports his thesis that the United States is a net creditor. The loophole in this argument is that it holds assets and liabilities vis-à-vis foreigners fixed. But because the United States runs current account deficits, liabilities rise faster than assets attributable to the deficit. So even if the U.S. earns interest income, net, from abroad, this effect will catch up.

There’s other way of saying all this. If r is return on assets A and L are assets and liabilities.

rA > rL

rA ·A > rL·L

is not inconsistent with

A < L

Second, using subscripts, 0 and 1 for now and some point in future,

rA0 ·A0 > rL0·L0

does not imply automatically that

rA1 ·A1 > rL1·L1

because liabilities can rise faster than assets (because of current account deficits) and even if return on assets is higher than return earned by foreigners on U.S. liabilities, net interest income can turn negative.

Anyway, the point of this post is that while netting is a good concept, one cannot blindly net accounting numbers. The example, a net FDI of $0 earning a net income of $1 and hence infinite return(!) is not a valid way of doing accounting. BEA’s numbers look correct.

Frequently, economists start discussing helicopters. This is the most counter-productive discussion. There are two things due to which they invoke this:

Confusion

Intent

The confusion part is basically due to economists’ complete failure to understand what money is and how to account for it and this is due to a lack of training in national accounting/flow of funds etc.

The intent part is equally important. This is because economists are trained in thinking of fiscal policy as impotent. After the crisis, they have party understood the role of fiscal policy but the notion that fiscal policy is impotent is so deeply ingrained that it’s difficult for them to come out of it. This reason is not so obvious but can be proved as follows: If they really think that fiscal policy is not impotent, they should rather suggest a rise in government expenditure than some helicopters.

Modern textbooks on macroeconomics treat money in a remarkably uniform – and remarkably silly – way. In the primary exposition the stock of “money” is treated as exogenous in the two senses a) that it is determined outside the model and b) that it has no accounting relationship with any other variable. The reader is then invited to assume, pro tem, that the central bank controls “the money supply” so that it is constant through time. When the operations of banks are described, typically some thirty chapters later, the quantity of money is some multiple of commercial banks’ reserves as a consequence of these institutions having become “loaned up”.

Silly? The money stock, as revealed in real life financial statistics, is as volatile as Tinkerbell – for good reasons, as I shall argue below. How can it be sensible to undertake a thought experiment in which the flickering quantity called “money” is literally constant through periods at least long enough for capital equipment to be planned, built and commissioned – and for lots of other things to happen as well? And the other, “money multiplier”, story has the strange defect that, while giving some account of how credit money might be created, it completely ignores the impact on spending of the counterpart changes in bank loans which are assumed to be taking place; perhaps it is because loan expenditure would mess up the solution of the IS-LM model when alternative assumptions about “the money supply” are used, that the supposed process of money creation normally gets separated from that of income determination by so many chapters.

The bibles of the neo-classical synthesis don’t help. There is a spectacular lacuna in the constructions presented, for instance, by Patinkin, Samuelson and Modigliani with regard to the asset side of commercial banks’ balance sheets. Usually the role and even existence of bank credit is simply ignored. Modigliani (1963) gives banks (with regard to their assets) no role other than to hold government bonds; and Milton Friedman famously used a helicopter when he wanted to get more money into the system.

There is a reason for all this. It is that mainstream macroeconomics postulates in its basic model that macroeconomic outcomes are all determined by relative prices established in Walrasian markets. Individual agents are held to engage in a market process of which the outcome is to find prices for product, labour and money which clear all three markets plus, by Walras’s law, the market for “bonds”. But as is now well known, there is no use for money in the Walrasian world even though, paradoxically, “money” is a logical necessity if the model is to be solved.

[boldening: mine]

There is no need for helicopters. All is needed is a description via social accounting (i.e. national accounting). Just say “increase government expenditure” to the government or “expand fiscal policy”.

I came across a nice Marc Lavoie paper from July 2015 from which I borrowed the titled of this post. Marc Lavoie discusses the importance of PKE monetary economics, stressing flow-of-funds modelling such as as done by Wynne Godley and his prescient analysis of the fate of the US economy and the rest of the world.

(the post title is the link)

Robert Blecker has a great article from the same conference (annual conference of the Canadian Economics Association) discussing similar things: heteredox understanding of the crisis. He discusseses Wynne Godley’s Seven Unsustainable Processes. He also talks of Hyman Minsky and neo-Kaleckian models of how income distribution effects aggregate demand. His paper titled Finance Distribution And The Role Of Government: Heterodox Foundations For Understanding The Crisis is here.