As mentioned in my previous blog, Paul Krugman tries his best to put down heterodoxy. His claims that nobody predicted the crisis is deeply unintellectual when someone such as Wynne Godley and other heterodox economists had warned about it. Moreover, Jan Hatzius who uses Wynne Godley’s approach also had made a case for a severe deflation around 2007. There’s a reason I bring in Hatzius because sometime ago, Paul Krugman mentioned Jan Hatzius:

Now, it’s interesting to note that the really smart Wall Street money doesn’t buy into this canon. Jan Hatzius and the rest of the economics group at Goldman have an underlying macroeconomic framework pretty much indistinguishable from mine, and have consistently talked down the risks from easy money and deficits.

[emphasis: mine]

There are two things dishonest about this. First, Jan Hatzius pays tribute to Wynne Godley when he writes for Goldman Sachs about the sectoral balances approach and obviously doesn’t mention Krugman. Second Wynne Godley was a heterodox economist and strongly against orthodoxy. Jan Hatzius uses Wynne Godley’s approach and Krugman claims it is indistinguishable from his and sidelines heterodoxy.

In response to Thomas Palley’s op-ed, Paul Krugman has written a couple of pieces on his New York Times blog (here and here)

I have seen many heteredox economists defending Krugman but these pieces should now make it crystal clear that Paul Krugman himself is the head of Gattopardo Economics. Consciously or subconsciously, Krugman’s strategy has been to sideline heteredox, in the hope that pages of history sing praises of him. Unfortunately for him, whenever he gets into a technical argument with heteredox economists on money, he makes the silliest mistakes.

Rather than giving many examples of why Krugman is the part of the problem, let me illustrate one example where he pushed very hard on the issue of free trade. It is a lecture paper for Manchester conference on free trade, March 1996 titled Ricardo’s Difficult Idea.

The following quote is clearly a strategy for propaganda:

5. What can be done?

I cannot offer any grand strategy for dealing with the aversion of intellectuals to Ricardo’s difficult idea. No matter what economists do, we can be sure that ten years from now the talk shows and the op-ed pages will still be full of men and women who regard themselves as experts on the global economy, but do not know or want to know about comparative advantage. Still, the diagnosis I have offered here provides some tactical hints:

(i) Take ignorance seriously: I am convinced that many economists, when they try to argue in favor of free trade, make the mistake of overestimating both their opponents and their audience. They cannot believe that famous intellectuals who write and speak often about world trade could be entirely ignorant of the most basic ideas. But they are — and so are their readers. This makes the task of explaining the benefits of trade harder — but it also means that it is remarkably easy to make fools of your opponents, catching them in elementary errors of logic and fact. This is playing dirty, and I advocate it strongly.

(ii) Adopt the stance of rebel: There is nothing that plays worse in our culture than seeming to be the stodgy defender of old ideas, no matter how true those ideas may be. Luckily, at this point the orthodoxy of the academic economists is very much a minority position among intellectuals in general; one can seem to be a courageous maverick, boldly challenging the powers that be, by reciting the contents of a standard textbook. It has worked for me!

(iii) Don’t take simple things for granted: It is crucial, when trying to communicate Ricardo’s idea to a broader audience, to stop and try to put yourself in the position of someone who does not know economics. Arguments must be built from the ground up — don’t assume that people understand why it is reasonable to assume constant employment, or a self-correcting trade balance, or even that similar workers tend to be paid similar wages in different industries.

(iv) Justify modeling: Do not presume, as I did, that people accept and understand the idea that models facilitate understanding. Most intellectuals don’t accept that idea, and must be persuaded or at least put on notice that it is an issue. It is particularly useful to have some clear examples of how “common sense” can be misleading, and a simple model can clarify matters immensely. (My recent favorite involves the “dollarization” of Russia. It is not easy to convince a non-economist that when gangsters hoard $100 bills in Vladivostock, this is a capital outflow from Russia’s point of view — and that it has the same effects on the US economy as if that money was put in a New York bank. But if you can get the point across, you have also taught an object lesson in why economists who think in terms of models have an advantage over people who do economics by catch-phrase). None of this is going to be easy. Ricardo’s idea is truly, madly, deeply difficult. But it is also utterly true, immensely sophisticated — and extremely relevant to the modern world.

All models are incomplete because they ignore many complications in order to highlight a few key concepts. In other times, a simple model is a starting point with the aim that the modeler adds more complications to make it more realistic. So it is sometimes not a good critique to point out what the models misses. But Steve Keen is making it look as if Palley’s critique is of what his models do not have.

This is diverting attention. For about two years or more, Keen has given all sorts of definitions of aggregate demand. The reason Palley’s critique is so solid is that it again points out that Keen’s definitions are wrong. Keen has repeated statements on aggregate demand and “change in debt” many times, making it sound like a universal law. Palley has shown via very straightforward arguments as quoted in my previous post Thomas Palley’s Nice Critique Of Steve Keen’s Models that the definition is incorrect. Moreover, Keen has changed his definitions as highlighted by a nice blog article by JKH. In my opinion Keen himself is confused on which definition is right and uses all of them together many times without realizing that they are different. His earlier definitions were simply incorrect on basic flow of funds accounting.

In short, there is no simple expression for changes in aggregate demand with changes in debt, a point mentioned by Nick Edmonds on his blog. Even if not, one could argue that it is useful but that is not the case because even at the theoretical level, there are conceptual issues, a lot because Keen doesn’t do his accounting right. Such things are not mere technicalities but the concepts of flow of funds is highly important to make some progress in analytic modeling.

Keen says:

My approach was to take the other side’s model, and show that if their assumptions were correct, they were right: banks could be ignored in macroeconomics, and changes in private debt had only a miniscule effect on demand.

Then I made one realistic small change, and hey presto — banks were essential to macroeconomics, and changes in private debt were the main game (but not the only one) in changing aggregate demand.

True neoclassical economists do not incorporate money and debt in their analysis but Keen has all this while given hints that Post-Keynesians themselves have not if you see his videos. Even the above quotes suggests as if nobody has done this before Keen. That coupled with the fact that Keen considers anyone having issues his models to be sinful of the loanable funds model. There is an irony here because Keen himself makes errors of the loanable funds approach when distinguishing bank debt and non-bank debt.

In my opinion Keen should completely get rid of this aggregate demand/change in debt slogan. Rejection of this does not mean debt is unimportant and all that. There are nice and realistic models such as that of Wynne Godley and Marc Lavoie (G&L) in which money and credit are central to the analysis and with no need at all for Keen’s fondness of aggregate demand/change in debt. These models have a very important role for aggregate demand and credit and feedback effects and so on but there is no need for inventing new definitions.

Neither is there any need for Lebesgue integrals. If one repeats Keen’s analysis where an economic unit pays for a good with a debit card or cash instead of a credit card, then it violates his own aggregate demand/change in debt definitions.

I think Marshall Auerback is seriously mixing up different parts of the flow of funds accounts of an economy. He is heteredox, so it will be good if he gets these things right.

… debt is once again rising relative to GDP. That shouldn’t be happening if corporate savings (profits) are booming.

Funnily, his question precisely has the answer: because profits are rising, so has liabilities of U.S. firms, because increased profits has led them to increase investment. This can easily be shown via a few national accounts/flow of funds identities. For the nonfinancial production firms sector, we have:

Net Lending = Undistributed Profits − Investment

Profits is undistributed profits plus dividends, and net lending is net acquisition of financial assets less net incurrence of liabilities,

Net Lending = NAFA − NIL

so,

NIL = Investment − Profits + Dividends + NAFA

where NIL and NAFA are firms’ net incurrence of liabilities and net acquisition of financial assets, respectively in the language of the flow of funds or the system of national accounts such as the 2008 SNA.

This suggests that if profits rise, firms may incur less liabilities but assuming other things in the equation stay the same. But if other things are themselves changing — such as if investment is rising, profits can rise simultaneously with rising liabilities. It is slightly paradoxical at first but CFOs generally know that firms’ borrowing requirement may rise when it is growing fast and the same is possible even if firms are taken as a whole. Firms may also buy back shares by borrowing from banks and this adds more interesting things to the story.

Of course, it is possible that the rising debt may move into an unsustainable territory but this story is a bit different than cooking the books interpretation of Auerback.

Some people point out that the critique “there is no money multiplier” is wrong because it is a ratio whatever said. No! The phrase “money multiplier” itself is wrong because the phrase itself captures a wrong causal story. A phrase is a small group of words standing together as a conceptual unit and hence the phrase “money multiplier” is inaccurate and misleading.

So take the textbook Keynesian multiplier first. It suggests that a rise in government expenditure leads to a rise in output more than the increase in the expenditure. The ratio of rise in output to the rise in expenditure is the multiplier.

But this is not the case with the “money multiplier”. There is no direction of causality from a rise in bank settlement balances to the rise in the money stock. This is true even if the central bank is doing QE/LSAP, i.e., purchasing assets on a large scale. So if the central bank purchases government bonds in the open market, it leads to a rise in banks’ settlement balances at the central bank and also a rise in the money stock. But the rise in the settlement balances could not have been said to have caused the rise in broad monetary aggregates such as M1, M2 etc. It is the act of the central bank purchase which leads to a rise in the stock of both narrow and broad monetary aggregates.

Now to the case of no QE.

Same story: the rise in banks’ settlement balances could not have been said to have caused a rise in broad monetary aggregates. The more appropriate phrase is “credit divisor”. Here’s Marc Lavoie from his 1984 paper The Endogenous Flow Of Credit And The Post Keynesian Theory Of Money

The Credit “Divisor”

To sum up the monetarist point of view, which, for causality purposes, is similar to the view endorsed by the great majority of economists, one can use equation (2):

M = m B (2)

where m is the monetary multiplier, and where causality is read from right to left, B being the independent variable while M is the dependent one.

On the other hand, the post Keynesian view can be summarized by equation (3):

B = (1/m) M (3)

where 1/m is the so-called credit divisor; B is the dependent variable and M is the independent variable. As a matter of fact, this equation cannot be found explicitly in any of the post Keynesian writings, but it is clear that such a relationship is implied by a large segment of the post Keynesian literature.

The choice between the multiplier and the divisor is a function of the opinions one has about general equilibrium. If one believes that money appears as the result of production processes, that is, as a consequence of the flow of credit created for entrepreneurs by commercial banks, then the multiplier is unacceptable since money becomes a sort of residue, which is incompatible with general equilibrium theorizing. Furthermore, central banks are generally engaged in “defensive” operations, that is, they act according to equation (3).

Another paper of Marc Lavoie informs us that the phrase credit divisor was first used by Louis Levy-Garboua and Vivien Levy-Garboua in a paper in 1972.

Thomas Palley has a new paper Effective Demand, Endogenous Money, And Debt: A Keynesian Critique Of Keen And An Alternative Theoretical Framework, which can be found on his blog.

In the abstract, among other things, Palley points out that Steve Keen’s treatment of endogenous money “falls into the theoretical morass regarding the black box of velocity of money via its adoption of a form of Fisher equation to determine AD.”

The part I found most interesting was that Keen’s new equation suggests that “changes in income are … driven exclusively by borrowing and loan repayment” and Palley illustrates the inaccuracy by considering cases where expenditure can be changed without borrowing:

The assumption that only borrowing and loan repayment can change AD is implausible. Households and firms can change their propensities to spend without borrowing or repaying loans. A central insight of Keynesian economics concerns the role of money which can act as a sink for purchasing power. Spending can be reduced by adding to idle balances, and it can be increased by activating existing idle balances. In the US, firms currently hold massive cash hoards. Those hoards can be activated to finance investment spending that increases AD. Export levels can change, and households and firms may also change the composition of their spending between domestic output and imports. Changes in the distribution of income, at both the functional and personal levels, can affect AD because of different propensities to spend out of income among agents. All of these changes can be accomplished independently of new borrowing or debt repayment. Moreover, borrowing in prior periods creates debt service transfers from debtors to creditors and these transfers will affect the pattern of leakages to the extent debtors and creditors have different propensities to save. Given all of that, there is no reason why this period’s aggregate demand should equal last period’s income or last period’s aggregate demand.

The paper is available in pdf at Thomas Palley’s blog post.

I was recently re-reading an article by Nicholas Kaldor and J. Trevithick [1] and I came across this fine description of rational expectations:

The main plank of the monetarist school has hitherto been that inflation is invariably ‘demand induced’: it can result only from an excessive demand for goods which, however, can manifest itself in the prevalence of excess demand in the labour market [footnote i]. In either case, any consequential increase in output or any fall in unemployment below its natural rate can occur only temporarily.

This latter view, which was shared until recently by the great majority of monetarist economists, is now contradicted by a more radical group of monetarists who developed the notion of ‘rational expectations’ and applied it to the study of inflationary processes. Their position is an extension of the argument that the increase in employment induced by monetary and fiscal policy is the result of some form of ‘cheating’ since workers had expected higher real wages than they actually received, whereas employers had expected to pay a lower real wage than they ultimately had to pay.

It is now claimed by this group of American monetarists that the above theory assumes that expectations are formed on an irrational basis, whereas it is in the interests of all economic agents to form a ‘correct model’ of how the economy functions. The proper cognition of the economy enables rational expectations to be formed which will prevent all but ‘surprise’ departures from an equilibrium path and will, therefore, render nugatory any attempt to reduce unemployment below its ‘natural’ level even in the short run. The centrepiece of this argument is that both workers and employers realise that the quantity theory of money is correct and that wages and prices must rise in the same proportion as the money supply. As a result, it is argued that increased expenditure will cause increases in wages and prices directly without affecting real variables such as output, employment or the real wage rate. They contend that they will base their expectations not on a projection of past trends in the price level or one of its time derivatives (such a procedure would usually be ‘irrational’) but on the ‘correct’ understanding of the economy which takes changing trends into account. Although the mechanism through which prices and wages rise is unclear, this school by-passes the traditional mechanism by which they rise under the pull of excess demand only. The corollary of this hypothesis is that inflation can be reduced far more painlessly than was thought by early monetarists, for, provided that the government can convince the public that it has a firm intention to get the money supply under control, the price level and the level of money wages will respond with only a very short lag: it does not require appreciable restriction of demand in real terms or any abnormal fall in employment even for a temporary period. [footnote ii]

This rational expectations theory goes beyond the untestable basic axioms of the theory of value, such as the utility-maximising rational man whose existence can be confirmed only by individual introspection. The assumption of rational expectations which presupposes the correct understanding of the workings of the economy by all economic agents—the trade unionists, the ordinary employer, or even the ordinary housewife—to a degree which is beyond the grasp of professional economists is not science, nor even moral philosophy, but at best a branch of metaphysics.

[emphasis added]

[footnote i: Harry G. Johnson, ‘What is Right with Monetarism’, Lloyds Bank Review, April 1976]

[footnote ii: It is well known that in the last five years, many Western countries have experienced the phenomenon of rising unemployment coupled with accelerating inflation. This appears to undermine the validity of the traditional natural rate hypothesis and, a fortiori, the rational expectations version. Professor Friedman (‘Inflation and Unemployment’, Institute of Economic Affairs, 1977), has acknowledged this divergence between monetarist theory and empirical observation, but he is hard-pressed to explain it.]

In this recent video, Marc Lavoie (at 28:00) quotes Philip Mirowski saying the same thing:

… orthodox macroeconomists came to conflate ‘being rational’ with thinking like an orthodox economist. What this implied was that agents knew the one and only ‘true model’ of the economy (which conveniently was stipulated as identical with neoclassical microeconomics) …

[1] Kaldor N. and Trevithick J. 1981. A Keynesian Perspective On Money, Lloyd’s Bank Review. (reprinted in Collected Economic Essays, Vol. 9)

In the previous post Paradox of Profits?, I mentioned how I view the paradox of profits as the confusion between production firms’ operating surplus (as defined in the SNA such as the 2008 SNA or earlier versions) and surplus on the financial account of the system of national accounts.

The paradox is highlighted by saying that at the beginning of the monetary ‘circuit’, firms inject an amount of money M and can only recover a maximum of M.

So let us think of an economy in which there is no money or banks initially and suddenly someone producers find a way to make cakes and the banking system opens simultaneously. This is admittedly an oversimplification but nonetheless useful.

Initially firms decide to make 100 cakes and price it $1 per cake. They hire labour and pay $60 as wages. For this, they borrow $60 from banks. Households is a mix of both labour and entrepreneurs.

Now households consume cakes worth $55.

Before proceeding, it is important to note that inventories will be valued at current costs. So even though firms have initially paid households $60 and recovered $55, they have still made a profit of $22. This is because 55 cakes were sold and cost $55 × 0.6 = $33.

So:

Profits = $22

I am neglecting the interest costs on loans but this is minor in comparison to the income generated by production so as to matter crucially.

That profits are $22 can be seen from the profits formula of the previous post:

Ff= C + ΔIN − WB −rlL

Having sold 55 units of cakes, firms have 45 units left in their inventory. But since inventories are valued at current costs, the multiplicative factor here is 0.6, so ΔIN = $27. So,

$22 ≈ $55 + $27 − $60 − ε

After having paid their employees, firms started out with no bank balance but soon have $55 in bank deposits. They then pay back $33 of loans, leaving them with $22 of bank deposits. At this stage household hold $5 of deposits: they received $60 and consumed $55.

So total bank deposits is $27. This is equal to the value of inventories. This is also equal to the initial loan of $60 minus the repayment of $33. So firms’ inventories are backing the loan amount.

Firms are now in a situation to distribute dividends. It is clear that they don’t have trouble paying interest to banks. (In this example but not always the case).

Another production cycle starts. Dividends will buy more cakes and make more profits for firms. Fixed capital formation can also be added in the story without any problem.

Post-Keynesians unnecessarily worry a lot about the paradox of profits. This post is on my thoughts on the paradox. In my view, there is no paradox at all. It is simply the case of not looking at all the parts of the system of national accounts/flow of funds.

Although Post-Keynesians use Kalecki’s profit equation in which the government deficit adds to profits, the statement of the paradox is for a pure credit economy. But in any case, there is none.

Let us assume that at the beginning of the ‘circuit’, production firms need an initial loan to pay the wage bill WB in advance. Households receive the wages and consume C and allocate their saving in financial assets (households don’t buy houses). The two financial assets are money and equities so:

WB − C = ΔM + ΔE

Production firms’ profits Ff is:

Ff= C + I –WB − rlL

Here, I is the gross fixed capital formation of production firms or investment, Lis the outstanding loan of firms from the banking system and rl is the rate of interest on these loans.

Now assume all investment is financed by issuing equities (i.e., ΔE = I). With a small amount of algebra:

Ff= − ΔM − rlL

So this is the “paradox”.

Now there are several things wrong with this. The simplest is that profits are actually paid to households and there’s a term for change in inventories missing in the right hand side. If profits are not paid, they are retained and investment is then financed by both issuing equities and retained earnings. So ΔE ≠ I.

There is an alternative way of stating the “paradox” which says: if firms inject money at the start of the production process, how do they recover more money at the end of the process? This seems to confuse what is known as operating surplus in the system of national accounts (such as in the 2008 SNA or earlier versions) with the surplus on the financial account.

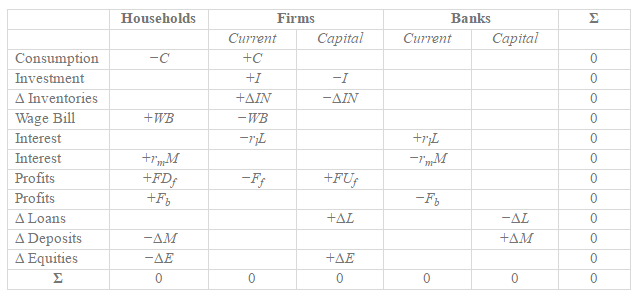

So let us redo this. Here is the transactions flow matrix for the economy (assuming away banks’ undistributed profits):

First assume all profits are distributed (i.e., FUf= 0 and FDf= Ff).

So:

WB + rmM + Ff + Fb − C = ΔM + ΔE

Ff= C + I+ ΔIN − WB −rlL

Then assuming ΔE = I and a bit of algebra,

ΔIN = ΔM

In other words, there is no paradox at all. Ff has simply dropped out. All this means is that if households wish to hold more of their assets in deposits instead of equities, firms will be left with more inventories.

Of course, you might ask, “how have you assumed that profits are distributed when there is a paradox?”. The answer is that I haven’t done anything self-inconsistent. More consistency checks would be via constructing a dynamic model and check if it solves but assuming it does, the above static analysis is good enough. There is no paradox to begin with.

So in the above, although there was no paradox of profits, there was still a pressure on output and hence profits—if households wished to hold more of their wealth in deposits and reduce their preference to buy equities, firms will be left with more inventories and will have to reduce investment. This reduction in investment happens because of two reasons – a fall in equity prices and a fall in output leading to a fall in firms’ expectations of sales. Of course, this can be seen via writing dynamic models, and one shouldn’t rely on identities. But bank loans will be useful here and so higher preference for ‘money’ needn’t necessarily lead to a fall in output. If households wish to hold more money instead of other assets, firms may switch to bank loans and this process creates deposits.

But let’s for the moment still assume that investment is not financed via bank loans but via issuance of equities and retained earning. In this case,

WB + rmM + FDf + Fb− C = ΔM + ΔE

Ff= C + I+ ΔIN − WB −rlL

but also,

ΔE = I −FUf

and with some algebra,

ΔIN = ΔM

Again, no paradox. At all!

Now in the final case, assume that production firms use bank loans to finance investment in addition to financing it via equities. The equations are:

WB + rmM + FDf + Fb− C = ΔM + ΔE

Ff= C + I+ ΔIN − WB −rlL

ΔE = I −ζΔL − FUf

where 0 < ζ < 1is that part of ΔL used for investment expenditure. In this case,

ΔIN + ζΔL = ΔM

So if households wish to hold more deposits, firms will switch to bank loans without any drop in inventories, output or expectations, with the qualification of course that bank credit is available.

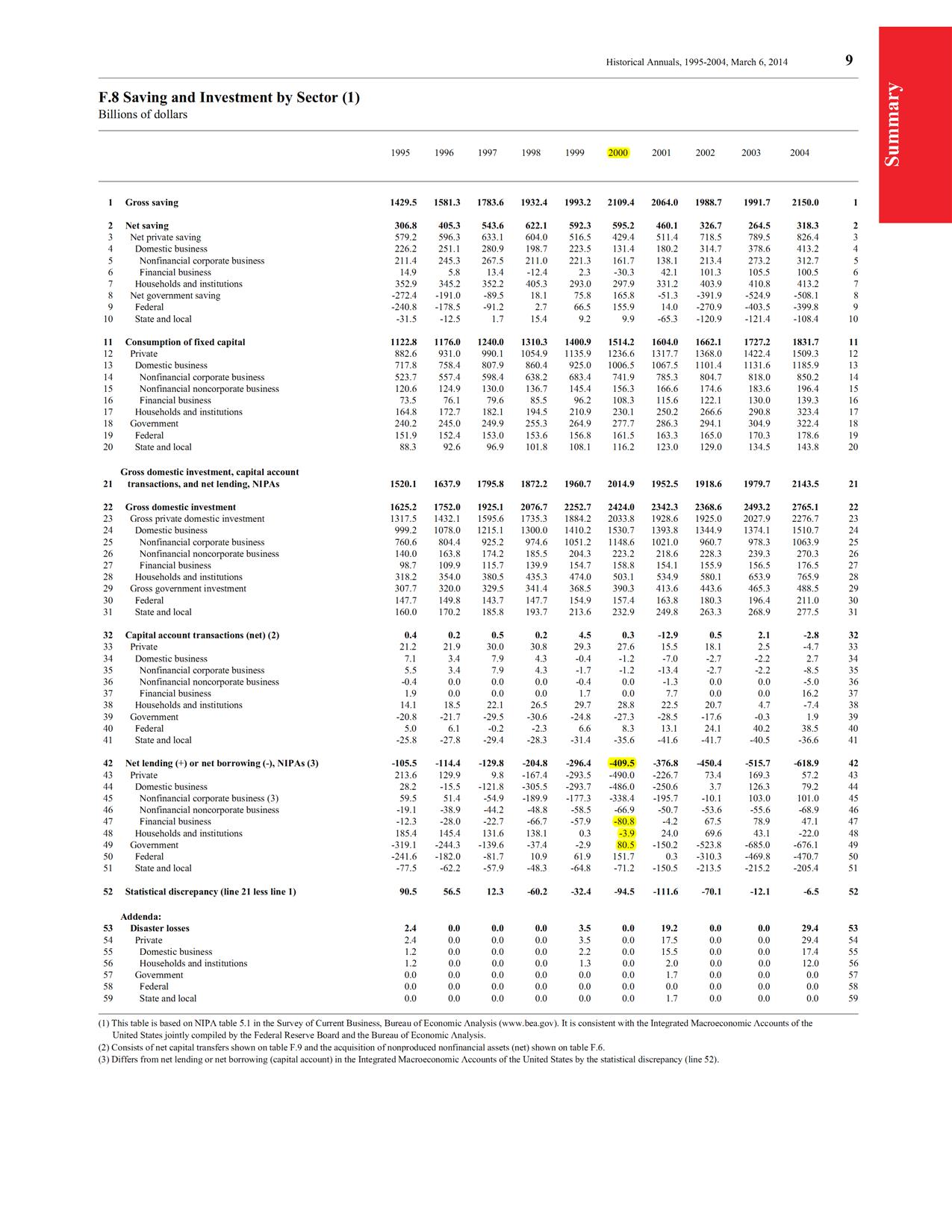

Some have suggested (via Kalecki’s profit equation) that the paradox can be resolved only because of government deficits. This is not needed at all because there is no paradox. So around the turn of the millennium, the US government had its budget balance in surplus and the nation’s current account balance of international payments was in deficit over many quarters. Yet US firms made profits and were able to distribute them.

See the data below: the first one highlights in yellow the current account balance (line 42) and the budget balance (line 49) and also the fact that the financial balances of other sectors (lines 47/48) were low negative compared to profits numbers in question (source Z.1):

(click to expand and click again)

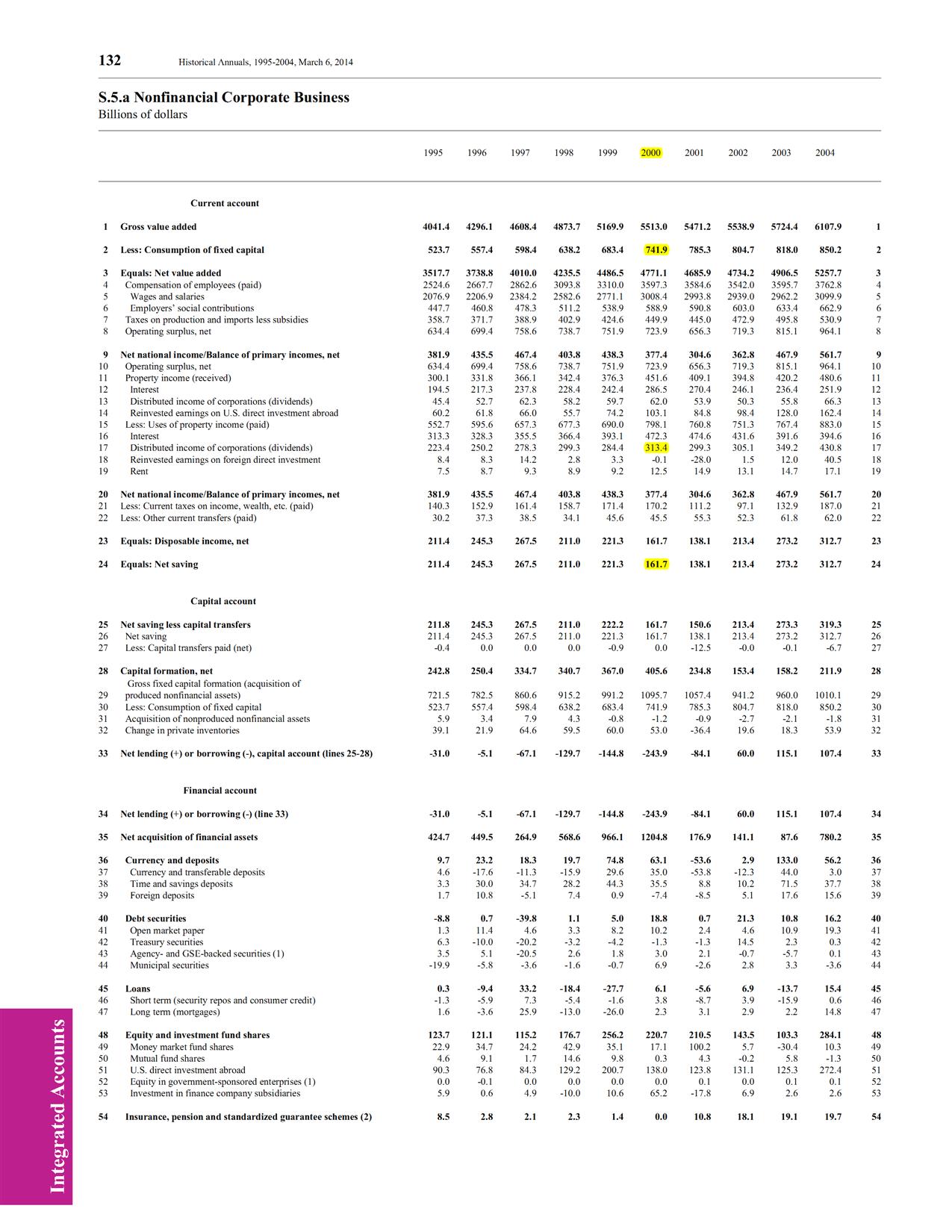

the second one shows the net undistributed profits (undistributed profits less depreciation) (line 24), distributed profits (line 17) and depreciation (line 2) from which profits can be calculated, implying budget deficit and/or positive current account balance of payments is not needed to resolve the paradox of profits (because there is none to begin with).

(click to expand and click again)

Of course, fiscal policy was tight around the time (although the budget balance is a poor measure of this) and this led to a fall in output soon, but that issue shouldn’t be confused with the paradox of profits.

Conclusion

One does not simply confuse operating surplus and surplus on the financial account of the system of national accounts. There is no resolution of the paradox of profits because there is none to begin with.

What brings the supply and demand for money into equivalence?

It is interesting that the recent Bank of England quarterly bulletin referred to an article of Peter Howells, a Post-Keynesian (also available here), although I don’t think the authors appreciate why the paper is interesting.

The title of my blog post is flicked from a paper by Basil Moore which is in reply to Howells.

Howells sets up the problem:

[B]anks set up their collateral standard and lending rates … and then meet all loan requests forthcoming. The demand for loans is determined by other variables in the economic system … making the loan volume exogenous from the banks’ point of view and the resulting quantity of deposits endogenous … Notice, crucially that in this view, increases in the money supply are demand-determined but the demand in question is the demand for loans … the question then is what reconciles the demand resulting from this lending with peoples’ willingness to hold money? … What is it that ensures that the supply of new deposits created by the flow of net new lending is just equal to the quantity demanded?

Let me present it in another way. To be clear let us assume the economy is closed. Output is determined by domestic demand or by private expenditure and government expenditure. Output is equal to the national income and is distributed to various economic units such as households who among other things allocate a part of their wealth into deposits. So there is a money demand. Of course expenditure is partly from income and sale of existing assets and by borrowing from other economic units and in particular from banks which lend by creating deposits in this process. So there is a change in the money supply. So there are two pictures with overlapping stories but not exactly so the question is – what processes ensure that

Ms = Md

is valid at every instant of time?

Does the rise in income and higher demand for money (because of a rise in wealth) alone ensure this? Is there a price clearance? Prices of what? Goods and services? Or prices in financial markets? (‘price’ includes interest rates such as deposit rates, loan rates, bond yields, equity prices and so on).

Also note this is in nominal variables. So is the rise in income purely due to a rise in prices or purely a rise in real output or a mix of the two? What causes inflation?

Where does QE fit into this? Does it raise output? Real/nominal? Raise prices – of goods and services or asset prices or both?

It is important to appreciate the formulation of the question. In case you don’t yet appreciate the question, more from Howells:

The starting point is that the demand for the loans that create the deposits originates in the desire of deficit units to spend in exceess of income. It is a question of financing an income-expenditure discrepancy. Furthermore, it is a decision made by a subset of the community since not everyone is involved in demanding an increase in their indebtedness to banks. (Indeed it is not even the case that everyone holds a stock of bank debt…). By contrast, the decision to hold (i.e., not spend) the newly created deposits is a portfolio decision. Furthermore, it is a decision made by different people (“the community as a whole”) from those concerned with borrowing it… the fact remains that so long as we are dealing with two groups of agents, with different motives, an ex ante coincidence of preferences is quite implausible. The question, then, is how are these ex ante preferences to be reconciled, ex post.

Back to Moore’s paper. Moore summarizes possible solutions suggested by Howells:

… Howells considers four responses that have been proposed to his conundrum:

Kaldor and Trevithic[k] – any excess money is automatically extinguished as a result of the repayment of bank debt.

Chick – the income multiplier process will automatically increase the demand for active balances.

Laidler – the buffer stock demand for money is a demand “on average” over a period of time, rather than a demand for a fixed stock at a moment of time.

Moore – “convenience lending,” the rejection of an independent money demand curve, rooted in a “full-blooded rejection of the idea of equilibrium”: In a non-ergodic world, no meaning can be attached to the notion of a unique general equilibrium stock of money demanded.

Howells maintains that the above list offers “promising solutions” to the mechanism that reconciles net new lending to borrowers with the change in the demand for money for the wealth holders. But he concludes that “each … on its own is almost insufficient” for the “reconciliation. As a result, he proposes that variations in relative interest rates, “which can and do occur continuously, provide the key to the fine-tuning required by the balance-sheet identity” …

Frequently in such discussions the accommodative behaviour of the banking system is forgotten. So there is another mechanism as highlighted by Nicholas Kaldor in his book The Scourge Of Monetarism (Oxford University Press, 1982):

As it is, a highly developed banking system already provides such facilities on an ample scale, since it is prepared to accommodate the public’s changing demand between different types or financial assets by altering the composition of the banks’ assets or liabilities in a reverse direction. If the non-banking public wishes to switch its holding of gilts for interest-bearing bank deposits, the banks are ready to supply such deposits at the minimum of inconvenience, and at the same time to place their surplus funds into the gilts which were previously held by the public. Similarly the banks provide easy facilities to their customers for switching balances on current accounts into interest-bearing deposit accounts, or vice versa.

In general banks not only hold government bonds but also other kinds of securities such as mortgage-backed securities, agency debt and so on. In olden days, there was no securitization and banks would hold more government bonds which got substituted. (See the Fed’s H.8 weekly release for data on banks’ assets) [There’s a Geithner ppt which mentions this in one slide, anyone has a link?]

This point is an important one because here the reconciliation happens via changes in quantities. Remember it is not just loans which create deposits but also banks buying bonds from the non-banking system which create deposits.

The answers to these questions can be found systematically by using James Tobin’s asset allocation theory.

Let me mention some positions. At one end are Monetarists for whom the direction of causality is from money to other things. So there may be an excess of money and if so leads to higher expenditure and a hot potato process in which money supply and demand are brought into equivalence by rise in prices of goods and services. It can also lead to a rise in real output but the Monetarists emphasize the price aspect more. In addition they also distinguish between government expenditure and private expenditure and try to point out that the latter is more efficient and so on.

Looking at an economy as a moving picture, as expenditures increase, output rises and there is a rise in prices of goods and services and a rise in the stock of money. Monetarists look at coincident events and assign some strange causalities.

Moving beyond Monetarism, there’s also a view that the reconciliation of the supply and demand for money necessarily happens via a rise in interest rates on everything including bank loans leading to a crisis. Of course that it not true because beyond a point banks will reduce lending instead of offering loans at higher interest rates. Banks have their own animal spirits but this is via tightening credit standards, quality of collateral etc. Also this is not the only outcome because the process of lending and borrowing increases output and income and can stabilize debt ratios. Nonetheless, debts can move into unsustainable territories and financial crisis do happen, and when it happens, there’s a high demand for money and the reconciliation may happen via bankruptcies of firms and the central bank may need to accommodate the rise in demand for money by lending at a large scale since bankruptcies threaten a fall in output.

Of course there are many more mechanisms for the reconciliation which I have avoided. It may happen that due to changes in portfolio preferences, there is a stock market boom and firms will go IPO instead of borrowing from the banking system. So we have economic units who wish to hold less money and more equities and firms borrowing less from the banking system leading to a reconciliation. (A more careful analysis is needed because firms have deposits after having raised funds through an IPO).

Now consider convenience lending. There is of course some truth to it. If you receive you salary on a Friday evening, you are not rushing to allocate newly held deposits into the stock market because it is already closed (unless you have an international brokerage account). So you are holding the deposits non-volitionally. However, subscribing to convenience lending alone is a bit extreme.

Now to QE/LSAP. When the central bank purchases financial assets such as government bonds from the markets, it creates bank settlement balances and deposits in the process. Wealth holders will then purchase other assets and the reconciliation happens via changes in prices of financial assets.

This post is far from any complete analysis of the interesting questions but hopefully I have got readers interested in something. The question on reconciliation asks what reconciliates the demand and supply of money – income, prices (of goods and services or prices in financial markets), quantities and so on. Also, some seem to think that “price clearing” has to do with some notions about an equilibrium. I don’t think these two are the same things. One can have price changes and clearances without appealing to the notion of any “equilibrium”.