In this New Economic Perspectivespost Randy Wray and Eric Tymoigne confuse accounting identities with behaviour.

In a context, the bloggers claim:

… Only a government deficit induced by fiscal policy leads to net saving.

where “net saving” is saving net of investment.

This posits a one-way causality of the sectoral balances accounting identity S − I = G − T from the right to the left.

This is inaccurate because of the endogeneity of the budget deficit which Wray himself is aware of but nonetheless confuses. This is because private expenditure may lead to a change in output and tax flows which may change the sign of the private sector balance (S minus I)

Suppose the private sector is in deficit and the government budget in surplus and the household sector drastically reduces its propensity to consume. This will lead to a fall in output and income and hence reduce tax flows to the government even if fiscal policy hasn’t changed (government expenditure and tax rate decisions haven’t changed) and the private sector’s balance can turn into a surplus from a deficit position.

That’s what endogeneity of the budget balance is all about. [Some government expenditure may change because of social transfers but the magnitude of this may be much lower than other things involved such as the private sector balance or changes.]

Second, it ignores the external sector.

Moreover the authors make another claim:

Monetary policy can change the composition of net saving by buying financial assets in the domestic sector in exchange for government currency, but it cannot change the size of net saving, i.e. the net accumulation of financial assets.

Cannot change the size of private sector saving net of investment?

Suppose the private sector is in surplus and interest rates are high. The central bank reduces interest rates drastically to induce the private sector’s expenditure to rise. If there is a large rise in investment for example, the private sector can go into a position of a deficit. It is true that the private sector may want to target a small surplus but this isn’t the case always and the private sector can remain in a deficit for long – not necessarily due to fiscal policy.

In the opposite case/scenario, starting from a case of a private sector deficit, suppose the central bank drastically raises interest rates to the point of causing the economy to go into a recession. The private sector balance may rise as people save more and output will fall, leading to lower tax outflows to the government and hence changing the private sector balance.

Some humility is needed by a few people who incorrectly seem to think they know how the world works with confused language such as “taxes aren’t revenue”!

Central bank asset purchases or LSAPs increase the stock of money aggregates compared to the counterfactual when there is no QE. Is there an excess of money?

These are two different things.

The notion of “excess money” is usually associated with Monetarism where the supposed “excess” is eliminated by rise in prices of goods and services. Excess money causes prices rise as much to reduce the value of money to reconcile whatever economic agents want to hold so that money demand = money supply where supply is given exogenously.

Which of course is quite wrong.

The reason it is wrong is that while – as argued in the previous posts – QE causes the stock of money to rise, there is no excess because prices and perhaps even quantities in financial markets (which is different from the market for goods and services) adjust so that the stock of money is still demand determined.

Of course that is not to say that the stock of money is the same as the counterfactual – i.e., the stock of money in a QE world is different from what it would have been in the absence of QE. So the stock of money is not exogenously given and adjusts to the demand for money as argued in the previous post and this demand depends on various things such as expected returns on imperfect substitutes – which QE influences.

In the markets for goods and services, there’s hardly an effect because prices are set by producers according to their costs.

Of course there needs to be a few qualifications – in the market for primary products, myths and speculation can lead to a rise in prices – such as the price of oil and this can have inflationary effects but the world we live in is not one in primary products and the original Monetarist idea highlighted at the start of this article is still misleading.

Of course none of this is implies that LSAP/QE has less effect on prices of financial markets – it can indeed cause some unwanted booms.

Another thing is that I mentioned in the previous blog post that supply of money influences demand but doesn’t determine it. Does that mean that the central bank has a “control” on the stock of the money within some limits? Well, not really. Control means influencing whatever is said to be under control to move in the desired direction and this is not always so. For example if the central bank were to behave like what the Bank of England was experimenting in the 70s under Monetarists’ influence, and sell bonds in large quantities in the financial markets, economic units – such as the non-banking sector may expect bond prices to fall and desire to increase their holding of money (as in deposits). This will lead them to sell the bonds to the banking sector which is prepared to buy the bonds acting as dealers in the bond markets. So the outcome may be opposite of the objective with which the central bank started with.

In the post, the blogger Circuit quotes Robert Hetzel who says:

Starting in mid-December 2008 when the FOMC lowered its funds-rate target to near zero with payment of interest on bank reserves, the textbook reserves-money multiplier framework became relevant for the determination of the money stock. The reason is that the Fed’s instrument then became its asset portfolio, the left side of its balance sheet, which determined the monetary base, the right side of its balance sheet. As a result, from December 2008 onward, the nominal (dollar) money stock was determined independently of the demand for real money. Although the reserves-money multiplier increased because of the increased demand by banks for excess reserves, the Fed retained control of M2 growth. Even if banks hold onto increases in excess reserves, the money stock increases one-for-one with open market purchases. (2012:237) (emphasis added)

This post is inspired by the nice comment by JKH in the same post.

JKH says:

Excellent post.

I think Hetzel is wrong though.

What is at work in QE is better described as a money duplication process rather than a money multiplier process. It’s entirely different.

The correlation between base changes and M2 changes during QE has nothing to do with the reserve ratio calculation that is part of the money multiplier math.

It has to do with the fact that non-banks were the ultimate source for most of the assets acquired by the Fed under QE. To the degree that’s the case, there is a 1:1 duplication of reserve expansion and M2 expansion at the point of transaction origin. Non-bank bond sellers basically convert their bonds to M2 at source.

Subsequent commercial bank balance sheet changes may change the one-to-oneness that appeared at origination, but that also has nothing to do with money multiplier dynamics.

So in total this has nothing to do with a standard money multiplier argument. The two should not be confused.

I have a few more things to add on Hetzel.

When the Federal Reserve buys assets such as US Treasuries and agency debt and mortgage-backed securities from the private sector, it increases the stock of money aggregates such as M1 – as most of the ultimate sellers are non-banks, even though the Federal Reserve purchases the bonds via reverse auctions from primary dealers.

Now whether the money multiplier story works or not (it doesn’t!), it superficially looks as if the Federal Reserve is determining the stock of money – supporting Hetzel’s view – again superficially.

But does it?

In Post-Keynesian monetary theory, economists say that the stock of money is “demand-determined” and Hetzel’s arguments seems to be against this view. However what Hetzel forgets is that while the Federal Reserve influences the stock of money, it is still demand-determined. This is because money-demand depends on agents’ portfolio preferences. If agents have “excess” stock of money, they may reflux this by reducing their loans toward the banking system – just like Post-Keynesians claim. The Federal Reserve QE Education page New York Fed 101: The Federal Reserve’s $600 Billion Treasury Purchase Program (Called by some QE or QE2) itself says so:

In fact since QE leads to higher asset prices, economic units may in fact borrow more funds to invest (read: speculate) in the stock markets.

Also note that “money-demand” is dependent on various things such as expected returns on substitutes. To the first approximation we may say that the stock of money was determined by the Federal Reserve since it has an eye on the monetary aggregates (although not targeting in the Monetarist sense). But once the process is set in motion, it then becomes endogenous because of behaviour of economic units.

Only in the limited case of settlement balances can we say that a monetary aggregate (monetary base or MB in this case) was set by the central bank.

The correct way of seeing this is via using Wynne Godley’s asset allocation model. In this what the variable Md is still decided by household behaviour – which depends on portfolio preferences, wealth, income and expected returns on all assets. LSAP works by reducing the supply of long-term bonds and hence reducing long-term yields via the “preferred-habitat” theory and hence increasing demand for other assets via imperfect asset substitution and changing their prices.

This itself has an influence on money-demand (because money-demand also depends on expectations of returns of other assets) but the amount of asset purchases by the Fed doesn’t determine the stock of money at any point in time.

Hence Hetzel is both wrong by appealing to the money multiplier mechanism and even if he hadn’t his other point about the stock of money being supply-determined is incorrect.

You can read Nick Edmonds’ blog on how this works – he has the most precise way of describing QE/LSAP.

Described as “Award-winning documentary about Keynes by Professor Mark Blaug, which received a Silver Medal at the New York Film and Television Festival circa 1988.” on the University Of Cambridge page of the video.

There’s also a book by Mark Blaug by the same title.

(h/t Louis-Philippe Rochon and Anas Abd Jalil on Facebook)

James Tobin’s papers are very interesting. I have a special liking for him even though he sometimes said strange things and used a lot of neoclassical analysis. His asset allocation theory is one of the most interesting things in monetary economics.

I came across this paper from his book Essays In Economics – Vol 1: Macroeconomics titled Money And Income: Post Hoc Ergo Propter Hoc? (also available here if you neither have the book nor jstor access).

The paper is also noted and analysed in Louis-Philippe Rochon’s book Credit, Money, and Production: An Alternative Post-Keynesian Approach (p 124 – )

In this paper Tobin takes Milton Friedman to task by constructing what he calls an “ultra-Keynesian” model which he describes as

In the ultra-Keynesian model, changes in the money supply are a passive response to income changes generated, via the multiplier mechanism, by autonomous investment and government expenditure.

(note: multiplier as in expenditure multiplier and not “money multiplier”).

For some strange reason Tobin says he doesn’t believe in this model but shows how Friedman’s empirical findings (the latter’s assertion that “changes in the supply of money are the principal cause of changes in money income Y”) are all wrong especially his assertion about leads and lags. This was also noted by Nicholas Kaldor in his 1970 article The New Monetarism reprinted in his Collected Essays, Vol 6 as Chapter 1.

… Suppose the initiating change is a decision of some firms to increase their inventories, financed by borrowing. The first impact is to cause some other firms whose sales have increased unexpectedly to incur some involuntary disinvestment. It is only when that is made good by increased orders that productive activity is expanded; any such expansion will cause higher wage outlays which in turn may involve further borrowing. The ultimate effects on income involve further changes in productive activity arising from the expenditure generated by additional incomes. There is every reason to supposing, therefore, that the rise in the “money supply” should precede the rise in income – irrespective of whether the money-increase was a cause or an effect.

So much for the various tests using Econometrics by Friedman – these don’t prove anything.

Again in his 1980 paper Monetarism and UK Monetary Policy, Kaldor states:

… the change in the money supply may be the consequence, not the cause, of the change in the money incomes (and prices), and that the mere existence of time-lag – that changes in the money supply precede changes in money incomes, is not in itself sufficient to settle the question of causality – one cannot rule out the possibility of an event A which occurred subsequent to B being nevertheless the cause of B (the simplest analogy is the rumblings of a volcano which frequently precede an eruption).

Back to Tobin. He says the following from what his “ultra-Keynesian” model:

… The main point of the exercise can be made by assuming that the monetary authority provides the bank reserves as necessary to keep r constant… The monetary authority responds to the “needs of trade”. With the help of the monetary authority, banks are able and willing to meet the fluctuating need of their borrowing customers for credit and of their depositors of money.

… The financial operations of the government and the banks are as follows: The government and the monetary authority divided the increase in debt … between “high-powered money” and bonds in such a manner as to keep the interest rate on target… the monetary authority provides enough new high-powered money to meet increased reserve requirements and any new demand for excess reserves. The remainder of the increase in public debt … takes form of bonds and is just enough to satisfy the demands of the banks and the public.

An important observation made by Tobin is that because the stock of money rises following a fiscal expansion due to a rise in income, an ultra-Keynesian

… would not even be surprised if some observers of the accelerated pace of monetary expansion in the wake of a tax cut conclude that monetary rather than fiscal policy caused the boom.

Tobin shows how “every single piece of observed evidence that Friedman reports on timing is consistent with the timing implications of the ultra-Keynesian model”.

This is quite important. Somehow most observers cannot understand the role of fiscal policy and there is almost total attention given to “what the Federal Reserve is doing or going to do” by economic commentators and “experts” of Wall Street with most comments on fiscal policy being that fiscal deficit should be somehow reduced. “We are all Keynesians now” is quite misleading because most economic commentators are heavily distorted by the quantity theory of money even though sometimes they claim to not believe in Monetarism.

Anyway, have a look at Tobin’s paper Money And Income: Post Hoc Ergo Propter Hoc?

In his chapter Postkeynesian Precepts For Nonlinear, Endogenous, Nonstochastic, Business Cycle Theories, K. Vela Velupillai has some nice words on Wynne Godley and his book Monetary Economics co-authored with Marc Lavoie:

Eugene Fama was on CNBC today (US time) (video here) and he argued that QE is a non-event.

Since he was on CNBC, I presume he has prices of financial assets in mind when he says it is a “non-event” – the logic being that the Federal Reserve and the Treasury together have effectively issued short-term debt and reduced the supply of long term debt.

Of course while this it is true that there is reduction of the supply of long term debt and increase in short term debt (compared to the counter-factual), it doesn’t mean it has no effect whatsoever. Of course Fama says it may have minor effect and the description of QE as a non-event is just a quick way of communicating his point, even if he is true, it is not that simple.

But first, it is great to see Fama doesn’t say this has led to a rise in prices of goods and services!

The U.S. Federal Reserve has purchased long term bonds – such as US Treasury securities and agency mortgage-backed securities by settling the purchase by issuing settlement balances to banks’ accounts at the Federal Reserve (in either case when a bank or a non-bank is a buyer).

This is however different from any other operation changing the composition of the bonds held by the private sector because in QE, banks have been holding balances at the Federal Reserve which they may not have held otherwise. As a counterpart to this the money stock compared to the counter-factual is also higher. Because of this, the non-bank private sector will “re-balance” its portfolio and this will clear via a higher price of assets such as bonds and equities.

In general investors – both residents and nonresidents – are also interested in international assets and this will lead to a price rise of equities in other countries as well because of capital inflows (from their perspective). Of course, one may argue that a capital flow in one direction is compensated by an outflow in the other direction but this needn’t mean there is no effect because this “clearing” occurs via changes in prices – such as exchange rates and prices of assets in the resident issuer’s currency.

There are two effects here. Prices of financial assets may change purely because of rise in expectations and also due to a rise in demand for the asset when expectations are held constant. In general both will have an effect because these two cannot be cleanly separated.

There are some who try to argue that as if it is only the expectations that matter – as if the rise is purely due to a change in investor sentiment and not due to a change in asset demand. From the point of view of asset allocation theory however, both matter.

Another thing is how much effect a billion of “asset purchase” by the Federal Reserve has. That is a slightly different question. In modelspeak it is that depends on the various parameters of the portfolio preferences. However there are people who say this is difficult to measure empirically. True but exactly for the same reason, it is also difficult to empirically say what effect this will have when if the Federal Reserve “tapers” QE.

At any rate, the point is that saying that the large scale asset purchases of the Federal Reserve or QE is just like another debt management operation is not a good argument because in QE, banks hold the short term debt of the official sector which is not the case in ordinary debt management operations and the counterpart to this is the rise in the money stock than otherwise leading to portfolio re-balancing by the non-bank private sector and the overseas sector.

There are some who think that Tobin’s asset allocation ideas (which was what Ben Bernanke had in mind when he started QE) are incorrect. Recently emerging market currencies saw sharp depreciation when it was thought the Federal Reserve may taper. Whether this was due to incorrect sentiments or due to whether the asset allocation theory applies is another question – the Federal Reserve Open Market Committee (FOMC) still has to consider these things when taking a decision on tapering because even if the asset allocation theory on which it has based its LSAP is wrong, investor sentiment may itself can have negative effects on financial markets.

Looking at the matter more academically, the thinking that “there is no portfolio rebalance” is equivalent to thinking that money (as in deposits) are held non-volitionally by the non-bank sector – something which doesn’t sound right.

In the above I avoided arguing how much effect QE has had on asset prices because as I mention it is difficult to empirically conclude. In my opinion it is quite strong. But irrespective of this, the fact that it is difficult to know empirically (but with some data from depreciation of currencies of “emerging markets”) also means that it is difficult to say what happens if there is “taper”. You could argue that there was no effect to begin with and hence there is no trouble withdrawing it but there is a risk that you may be wrong!

Personally I think QE is a waste of time but for different reasons. It somehow misleads policy makers – the ones making fiscal decisions to wishfully think something good is going to happen. Financial markets however seem to be worried at the mere mention of “taper” so the best way for the Federal Reserve would be to convince that this is silly – slowing down is not to be worried about.

An interesting article, which raises the following questions in my mind: Is the younger generation of economists like Raj skipping some of the big questions of economics because some smaller questions are easier to answer? If so, is that optimal from the standpoint of society as a whole?

There are two things here: The question whether Economics is a science hides the fact that most economists at the most basic level are simply incompetent and struggle with basic economic concepts. This can come across as pompous but you only have to look to believe it. The Mankiw quote above is another level of shamming.

In other subjects – science or in arts – if you have the talent, there is a good chance you are successful and lead a good life. Of course one can fail or not do well for various other reasons such as having a failed love relation affecting your performance and so on, but if you are interested in economics early in life and go to a university to study, ability can make your life difficult and even miserable because your professors don’t know anything.

While it is a good debate to compare Economics to sciences such as Physics, the trouble is that almost all economists at the most elementary level fail to understand the most basic things.

Take for example the textbook on Macroeconomics by Krugman and Wells. If you are interested even partly in Macroeconomics and skim through heteredox blogs, you will find out how the concept of the “money multiplier” is erroneous to say the least. But look at what the authors say in page 399 of the 3rd edition:

(source: amazon.com)

And this – the money multiplier story – is just one example among numerous others. The question of whether economics is science or not is sometimes irrelevant when at the most basic level, most economists failed to understand simple things.

Paul Krugman seems to have been thinking on issues related to open economy monetary macroeconomics these days! He has recently warned his readers to not confuse accounting identities with causation but in a recent blog post he seems to be doing it himself.

So Krugman says:

So, here we go. Start from the observation that the balance of payments always balances:

Capital account + Current account = 0

where the capital account is our sales of assets to foreigners minus our purchases of assets from foreigners, and the current account is our sales of goods and services (including the services of factors of production) minus our purchases of goods and services. So in the hypothetical case in which foreigners lose confidence and stop buying our assets, they’re pushing our capital account down; as a matter of accounting, then, our current account balance must rise.

But what’s the mechanism? (Remember the fallacy of immaculate causation.) The answer is, it depends on the currency regime.

Strange. The last statement in the quote warns of potential mistake which is present in the previous statement! ie Krugman wants to have it both ways.

So “… as a matter of accounting …” ?

Let us consider a case (fixed exchange rate or floating) where there is an autonomous capital flow – such as a foreigner liquidating a bond and repatriating funds. This by itself doesn’t affect the current account. In fact it can be compensated by some accommodative flow in the capital account of the balance of payments.

[accommodative capital flows] take place only because the other items in the balance of payments are such as to leave a gap of this size to be filled … [while] autonomous payments … take place regardless of other items in the balance of payments.

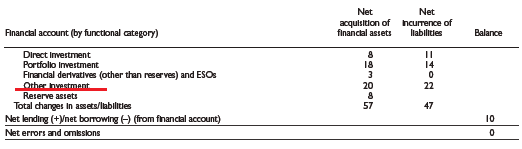

Of course because of flexible exchange rates, the distinction can become blurred but the same is also true in fixed exchange rates. So we have an item called Other Investment in the capital account of balance of payments – like the example in the IMF’s BPM6 (note: “financial account” in the BPM6 terminology, capital account means a different thing):

In addition Reserve Assets is also one. Again this is somewhat of a simplification and it is possible for other items to accommodate.

“Other Investment” is typically banking sector flows but refer to BPM6 for the full definition. “Reserve Assets” is things such as sale or purchases of foreign currency by the central bank or any other official institution. Sometimes a category Exceptional Financing is used – such as government borrowing in foreign currency in exceptional circumstances or official financing transactions from the IMF.

So changes in some items in the capital account can be balanced by changes in some other account in the capital account and not the current account. Of course this doesn’t mean that there is no causality from the capital account to the current account and I will come to it in a moment but what Krugman says is silly.

Let’s take a few examples starting with the simplest – and you guessed it right – the Euro Area 😉

Suppose there is a capital flow where a German financial firm liquidates Spanish government bonds and transfers funds back home.

As I have explained in posts long back, this will lead to a TARGET2 imbalance in which the Spanish NCB will have a rise in indebtedness to the ECB (which is considered to be a Spanish non-resident). Either it ends here or the Spanish banking system will try to attract funds from abroad. In either case there is an accommodative flow in the balance of payments – balancing the initial outflow and without affecting the current account.

Now take the example of a nation with its currency pegged to another anchor currency. Suppose a nonresident economic unit sells sells securities and transfers funds outside the country. Since banks acts as dealers in the foreign exchange markets, this leaves the banking system with a short position in foreign currency. It may try to close it by borrowing in foreign currency or try to attract funds from outside. In the latter case that is all there is to it (in the short term) and this flow is accommodating and will appear in Other Investment. In the former case, the banking system is left with an open position in foreign currency. As long as the bank’s own risk management or the central bank (with the confident knowledge that it has sufficient foreign exchange in case it has) thinks this it is alright, this is what there is for the short term. Else banks may need to attract funds from abroad. However if there is a depreciation outside the tolerable band (fixed doesn’t mean god has fixed it) in response to a huge amount of capital outflow, the central bank may sell foreign currency. It may also try to hike interest rates to get attract foreigners.

Again no change in the current account. One item in the capital account cancels another to preserve the accounting identity Krugman quotes.

In floating exchange regimes this is more complicated but the story is not too different from the BoP viewpoint. An outflow of funds will be accommodated by banks’ open position (or inventories). Banks will typically try to offload the inventories depending on market conditions and opportunities and it is sometimes said in the fx microstructure theory that the inventory half-life is around 15 minutes. The currency will depreciate to the point where expectations of the market participants reverse in the direction of appreciation bringing in flows in the opposite direction to the initial capital outflow. How this works precisely is a very challenging open question. Of course looked at from a medium term perspective, in general, it is not immediately obvious why the current account balance and capital account sum to zero since the magnitude of “Portfolio Investment” and “Direct Investment” may be quite different from the current account balance. But the sum of balances is zero as a matter of accounting. In such cases, banks may try to attract funds from abroad themselves by marketing bonds offshore – i.e., they may try to find offshore funding. More complications arise from derivative contracts with nonresidents which is not easy to go into in this post.

Of course this not guaranteed to work – pure float is the luxury of a few nations – and sometimes the central bank may need to intervene in the foreign exchange markets and in the extremis, undertake exceptional financing transactions such as borrowing from the IMF.

In recent times, the Reserve Bank of India had an interesting swap scheme with the banking system who would attract funds from abroad.

Of course, none of this means there is no causality from the capital account to the current account. A nation may face troubles financing its balance of payments and it may try to deflate domestic demand by fiscal and monetary policy to keep its current account imbalance from getting out of hand. It is important to note here this is not a straightforward result of the identity but there is a more complicated story and that output suffers because of this. Krugman makes it sound as if nothing happens to output.

Question: Are flexible exchange rates better than fixed exchange rates?

Answer: Silly oversimplified question.

In a blog post today, Paul Krugman asks Do Currency Regimes Matter? – in the context of the Euro Area. My answer to that would be James Tobin’s wisecrack:

I believe that the basic problem today is not the exchange rate regime, whether fixed or floating. Debate on the regime evades and obscures the essential problem.

Of course that doesn’t mean one ties both shoes together and irrevocably fixes exchange rates (and give up the government powers to make drafts at the central bank) but the essential problem referred above – although gets diluted – doesn’t go away outside a monetary union. Also, a crucial element often missed in the discussion is the existence of the “common market” which acted as (and still acts as) a constraint on Euro Area economies to expand domestic demand.

Sadly by blurring issues such as this and oversimplifying the macroeconomics behind all this, the Euro Area was formed with the incredible lacuna.

One of economists’ fantasy is assuming the existence of a floating exchange rate regime without any need of official intervention. Although it is true for some nations, it doesn’t mean any nation can simply “truly float” and stop worrying.

In the same article A Proposal For International Monetary Reform, Tobin also points out:

Clearly flexible rates have not been the panacea which their more extravagant advocates had hoped …

although also pointing out that:

… I still think that floating rates are an improvement on the Bretton Woods system. I do contend that the major problems we are now experiencing will continue unless something else is done too.

Incidentally, I do not think Tobin tax in the foreign exchange markets is the way to go as has been pointed out by economists working in fx microstructure theory. Nonetheless Tobin’s highly important insights remain.

John Maynard Keynes’ biggest disservice to the economics profession is to not start with an open economy. In a world of free trade and free movement of capital, a nation’s biggest constraint on raising output is the “balance-of-payments constraint”. It is sad that in spite of the crisis the economic profession has not even started debating on the constraints imposed on nations due to free trade (and the whole world as a consequence).