There was a conference on the 10th death anniversary of Wynne Godley last year. If you haven’t seen it, the video recordings/presentation/remarks are in that link.

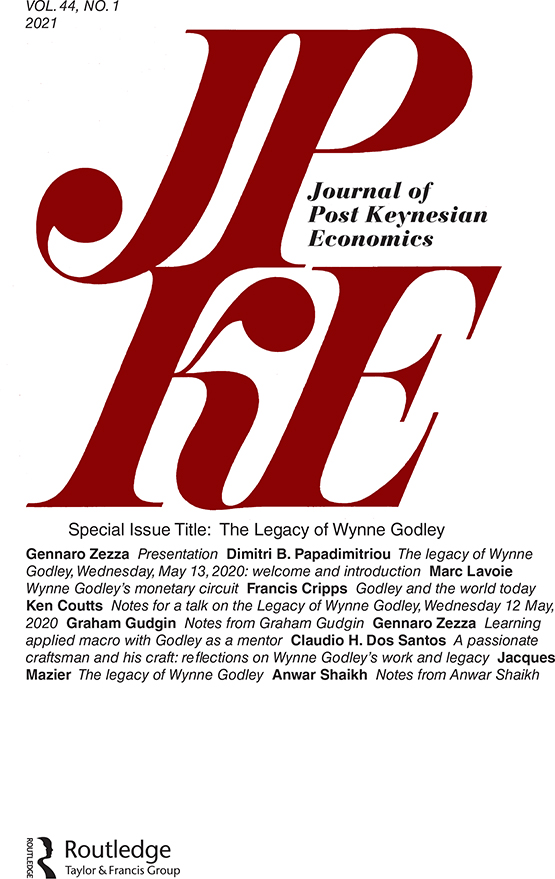

Now, there’s a special issue by the JPKE about the conference with papers as in the cover:

Recently, Institute For New Economic Thinking (INET), interviewed Anwar Shaikh in their New York office. It’s like a short autobiography of his work and his life and a background to his book, Capitalism: Competition, Conflict, Crises. Shaikh starts off describing his personal background and what led to him ask the questions he asks. He then talks about his work, from the humbug production function to the theory of international trade to the responsibilities of the heterodox.

An interesting story is about his association with Joan Robinson while writing the paper on the production function. Shaikh tells us that he was at Columbia University at the time and the professors there told him, “Joan Robinson is not an economist”!

[the header of this article is the link to the INET page which has the video and a brief description]

Henry George School of Social Science is making available lectures of a 2-semester course by Anwar Shaikh on his latest book, Capitalism: Competition, Conflict, Crises.

Anwar Shaikh is one of the few economists who had warned about cracks in the foundations of growth of the US economy and the world economy as a whole and that it will lead to a crisis in the 2000s. He has a new book titled Capitalism: Competition, Conflict, Crises. It will be published around February next year.

The book and 1024 pages and looks like a huge analysis of all ideas in economics. You can preview the table of contents at amazon.com here. The book is published by Oxford University Press and the book’s page at OUP is here.

Anwar Shaikh is a very knowledgeable economist. In an interview to Ian Macfarlane, Wynne Godley says how much he learned about neoclassical economics from Anwar Shaikh. They then put up a paper titled An Important Inconsistency at the Heart of the Standard Macroeconomic Model. Wynne Godley considered it one of his most important papers. I like the paper and want to sometime rework it in a slightly different way to show that neoclassical economics makes no sense at all.

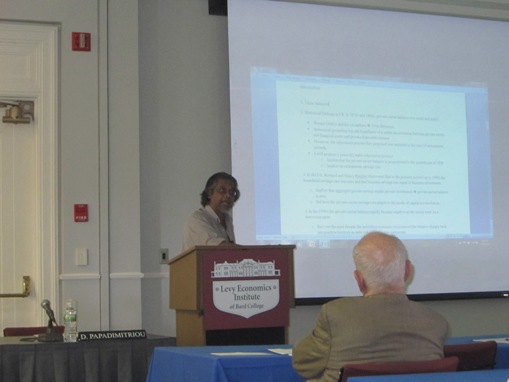

Anwar Shaikh, Levy Institute, May 2011, Photograph by me.

Louis-Philippe Rochon and Sergio Rossi have a very interesting articleEndogenous Money: The Evolutionary Versus Revolutionary Views in the Review Of Keynesian Economics. I think it was written many years back and was in an unpublished form and has been published now. It is a nice critique of views of some Post-Keynesians such as Victoria Chick and also others such as Basil Moore. For instance, the paper quotes Moore’s view from 2001:

[w]hen money was a commodity, such as gold, with an inelastic supply, the total quantity of money in existence could realistically be viewed as exogenous.

Click the image to visit the ROKE website.

There are also some nice articles in a recent issue of JPKE on neoliberalism and the financial crisis.

Some gossip: The JPKE was initially supposed to have been called Journal of Keynesian Economics but it didn’t make it because the acronym would have been JOKE.

Also, Jayati Ghosh has written an excellent blog article on Thatcherism – the ‘triumph of private gain over social good’ (borrowing words from her).

Matias Vernengo has a recent blog post on the persistence of poverty in the United States. Which reminds me of an interview clip of Anwar Shaikh titled “The Sin Of Our Era”:

click to watch the video on YouTube

Back to formal matters.

What does it mean when an economist says words such as “endogenous”, “exogenous”? Most of the times, economists – mainstream economists – themselves confuse these terms and hence you see a lot of usage of these words in Post-Keynesian economics.

An exogenous variable is supposed to be a causal variable, if the structure of a model has economic meaning. In fact, it is usually just a variable that is put on the right-hand side of equations in a model, but not on the left-hand side.

Similarly, an endogenous variable is supposed to be a caused variable. In fact, it is usually just a variable that shows up at least once on the left-hand side of an equation

which is fair but there exists another language.

There is however another usage – that is in the control sense.

Apparently no generally accepted concept of an endogenous money stock (or monetary base) has been defined. In statistical theory a variable is endogenous if it is jointly determined with other variables in the system. However, many monetary theorists have chosen to call a variable endogenous only if its magnitude is not under the control of policymakers. Such semantic problems have undoubtedly prolonged this debate.

For the money stock measure such as M1, M2 etc., there shouldn’t be any confusion. The trouble arises for things such as interest rates. For example, some economists may say that if inflation rises, the central bank may/will raise the short-term interest rate and it is endogenous while others will say it is up to the central bank to decide how much to change the interest rate, if at all. Such things lead to a lot of debate.

I like the latter usage (the control sense) but I think it is difficult to exclusively have the same usage.

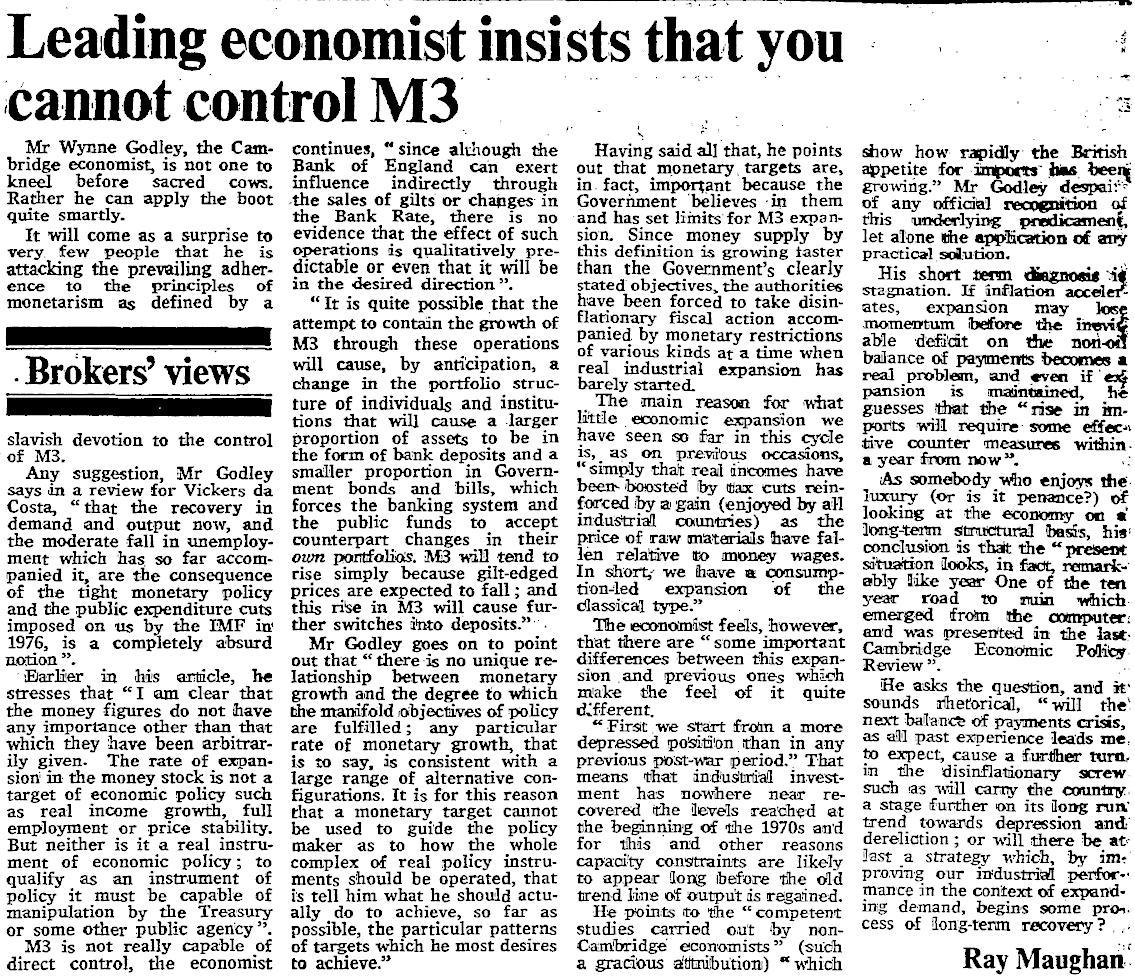

The word “control” is also misunderstood. Here is a fine article on Wynne Godley in The Times from 16 June 1978 where he details on how misunderstood the word is:

Happy reading!

Happy reading!