One of Augusto Graziani’s best papers was The Theory Of The Monetary Circuit, Économies et Sociétés, 24 (6) (June), pp. 7–36. The paper is available at the UMKC course site here.

One description of money is looking at payments as triangular transactions. Graziani says that for money to exist, three conditions have to be met:

since money cannot be a commodity, it can only be a token money;

the use of money must give rise to an immediate and final payment and not a simple commitment to make a payment in the future; and

the use of money must be so regulated as to give no privilege of seignoriage to any agent

(image credit: Xerxes Books, from whom I obtained the copy)

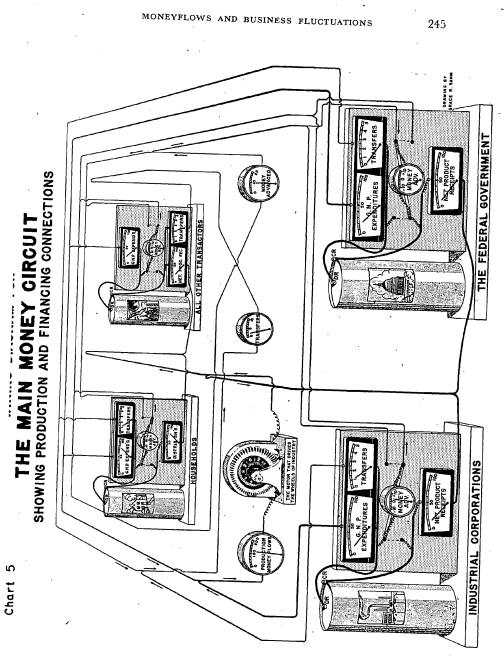

In his book, he actually draws a diagram of a circuit – on the inside covers and on page 245:

The circuitists’ motivation for using the phrase “circuit” was a circular flow starting with credit but Copeland was in total opposition of the usage of the phrase “hyrdraulic/s” and the misleading notions that this latter phrase conveys about money. Hence he proposed the phrase money circuit. Check his book on why this is so for details. I will at some point write about Copeland’s arguments.

One of Graziani’s main themes runs as follows. In order to finance production, the entrepreneur must obtain the funds necessary to pay his workforce in advance of sales taking place. Starting from scratch, he must borrow from banks, at the beginning of each production cycle, the sum which is needed in order to pay wages, creating a debt for the entrepreneur and, thereby, an equivalent amount of credit money, which sits initially in the hands of the labour force. Production now takes place and the produced good is sold at a price which enables the debt to be repaid inclusive of interest, while hopefully generating a surplus – that is, a profit – for the entrepreneur. When the debt is repaid, the money originally created is extinguished. An entire monetary circuit is now complete.

This account of the monetary circuit has a number of extremely important and distinctive features. It emphasises, in particular, that a) there is a gap in (historical) time between production and sales which generates a systemic need for finance; b) bank money is endogenously determined by the flow of credit and c) total real income must be considered to be divided into three parts – that received by entrepreneurs, that received by labour and that received by banks. We have already travelled an infinite distance from the (yes, silly) neo-classical world where production is (must be) instantaneous, where money must be exogenous and fixed and has no counterpart liability, and where the distribution of income is determined by the marginal products of labour and capital – a construction which depends entirely on the assumption that all firms sit perennially on a single aggregate neoclassical production function frontier.

Few posts back, in More On Horizontalism, it was mentioned how loans make deposits. The unanswered question in the post was If loans make deposits, why do banks require funding? That will still be left unanswered for the time being, but in this post we will discuss simple payment systems and settlement. Hopefully it was clear in the post how banks occupy a central position in the process of money creation.

Before we go into payment systems, first let me introduce to Augusto Graziani’s concept of money, which I really like [1].

since money cannot be a commodity, it can only be a token money;

the use of money must give rise to an immediate and final payment and not a simple commitment to make a payment in the future; and

the use of money must be so regulated as to give no privilege of seignoriage to any agent

So the process of settlement involves more than two agents and in most cases, the payer, the payee and a bank. Even in cases, when the payer pays the payee in currency notes, the transaction secretly involves central bank money because currency notes are liabilities of the central bank.

How do banks settle among themselves? A simpler but not often asked question is why banks need to “settle” amongst themselves? This will be answered soon but the answer to the first question is central bank money. Banks cannot keep telling each other “I owe you”. Central banks haven’t existed since the beginning of time, and banks would earlier settle among themselves in gold. Why gold? is a slightly difficult to answer but at this point it’s sufficient to say that the properties of gold have made it attractive for settlement.

Before we get into payment systems, let us for the sake of formality, categorize payments into two types [2]- credit transfers (“push”) and debit transfers (“pull”). Most transfers are credit transfers and are initiated by the payer. Debit transfers are transfers initiated by the payee. Example: a cell phone company making a payment instruction to its customer’s bank to transfer funds to its own bank account at the end of a bill cycle to settle the monthly bill, after the customer has allowed the pull transaction to take place periodically. We will worry about only push transactions.

Technology has advanced so much that such payments happen fast! RTGS – Real Time Gross Settlement is a feature banks offer (for a minimum transaction size) in which transactions are settled in real-time with instant irrevocable finality. In the Euro Area, the European System of Central Banks have developed a system called TARGET2, which I believe settles all payments real-time.

So in the above diagram, customer A who banks at Bank A transfers funds to customer B who banks at Bank B. After the payment instruction is initiated, Bank A owes $1m to Bank B. Since everyday, there are zillions of transactions happening in both ways, banks try to keep a balance at the central bank. These are called reserves but modern central bank articles use the phrase settlement balances more often these days.

What happens if banks do not have sufficient funds at the central bank? Is that allowed? Since central banks require that funds be transferred as soon as possible, they allow banks to go into an overdraft. How much overdraft does the central bank provide? In principle – as much as possible, provided banks provide good quality collateral. Central banks have standards on what collateral is acceptable and these may change from time to time. Typical requirements include good rating by the rating agencies. Since the market value of the collateral can fluctuate and it is risky for the central bank, they require a haircut. This roughly means that for borrowing (i.e., going into an overdraft at the central bank) say $1m, banks need to provide a collateral whose market value is say $1.1m. This is a topic in itself, and no more will be said for now – maybe a good topic for a future post!

This brings me to the final part of this post. What about settlement between a bank and its customers? Bank employees, for example, are encouraged to open an account at the same bank and their monthly salary is credited at the end/beginning of the month. Is this settlement? A rough answer to this question is that bank money is convertible. There is nothing preventing a bank customer from transferring funds to another bank. If the customer does so, the diagram above shows that the bank has to settle the amount with another bank or the central bank and has to attract funds from various sources. Else, the bank has to offer an alternative to the customer such as paying interest on the deposits and requiring in exchange that the customer is not able to withdraw funds for a fixed term. Needless to say, the bank also needs to maintain good relations with the customer.

Finally, the topic of international money flows is dear to me and will be taken up in another post.

References

Augusto Graziani, The Theory Of The Monetary Circuit, Economies et Societes, 1990. Available at the UMKC course site

Dominique Rambure, Alec Nacamuli, Payment Systems: From Salt Mines To The Board Room, Palgrave Macmillan, 2008.