Frequently, discussions about debt sustainability have discussions about the importance of the interest rate and growth in debt sustainability analysis. See for example, today’s Paul Krugman’s post on his blog. It is concluded that as long as the rate of interest is below the rate of growth, the ratio public debt/gdp doesn’t explode. Unfortunately, this result is erroneous.

John Maynard Keynes’ biggest disservice to the profession is to not start with the open economy. In my view, debt sustainability is tightly connected to balance of payments.

Imagine a nation whose exports is constant. If output rises, it will have adverse effects on the current account balance of payments because of income induced increase in imports. This will have an adverse effect on the international investment position of the nation: the net international investment position will keep deteriorating unless output is slowed down or some measure is taken to improve exports. In the case of rising exports, there is a similar constraint, except it is weaker but dependent on the rate of growth of exports.

If the ratio net international investment position/gdp keeps deteriorating, either the public debt to non-residents or private indebtedness to non-residents or both have to keep rising, all unsustainable.

There are some complications. A nation’s balance of payments also depends on how assets held abroad and liabilities to foreigners affect the primary income account of balance of payments. Also, the exchange rate can depreciate (or be devalued in fixed-exchange rate regimes) improving exports and reducing imports. However assuming that exchange rate movements do the trick is believing in the invisible hand. Foreign trade doesn’t just depend on price competitiveness but also on non-price competitiveness. These complications are highly interesting but do not affect the fundamental fact that a nation’s success is dependent on the success of corporations to compete in international markets for goods in services.

Even the conclusion that the government should contract fiscal policy and aim for a primary surplus in its budget balance or else the ratio public debt/gdp keeps rising if the rate of interest is greater than the rate of growth is erroneous. Consider a closed economy. An expansion in fiscal policy will automatically raise output and gdp and hence tax collections to prevent the ratio public debt/gdp from exploding. The public sector balance may hit primary surpluses but not due to contraction of fiscal policy or targeting a primary surplus in its budget balance.

In short, although the rate of interest and the rate of growth are important in debt sustainability analysis, it is not as easy as is usually presenting in macroeconomics textbooks and in the blogosphere. For a more detailed analysis see the reference below.

Reference

Godley, W. and B. Rowthorn (1994) ‘Appendix: The Dynamics of Public Sector Deficits and Debt.’ In J. Michie and J. Grieve Smith (eds.), Unemployment in Europe (London: Academic Press), pp. 199–206

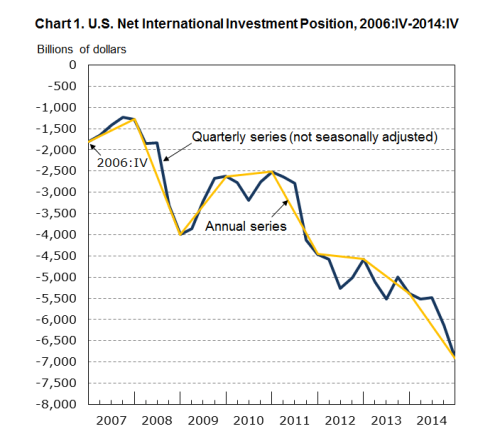

The U.S. Department of Commerce’s Bureau of Economic Analysis today released accounts for the United States’ international investment position. The U.S. is sometimes called the world’s biggest debtor and its net international investment position is now (at the end of 2014) minus $6.9 trillion.

Here’s the chart from the BEA’s website. A few points. The importance of the U.S. balance of payments and international investment position is quite neglected in analysis of the crisis. The United States’ economy went into a crisis (and the rest of the world with it) because a huge rise in private indebtedness led to a fall in private expenditure relative to income when the burden of the debt started pinching. This caused a drop in economic activity and was saved partly due to automatic stabilizers of fiscal policy as tax payments fell due to a drop in economic activity and partly due to a relaxation of fiscal policy itself by the U.S. government and governments abroad. But the huge rise in the U.S. government debt meant that resolving the crisis by fiscal policy alone would have been difficult. This is because a huge fiscal expansion would have meant that the U.S. trade deficit would have risen much faster into an unsustainable path.

See Wynne Godley’s article The United States And Her Creditors: Can The Symbiosis Last? from 2005 here arguing such things.

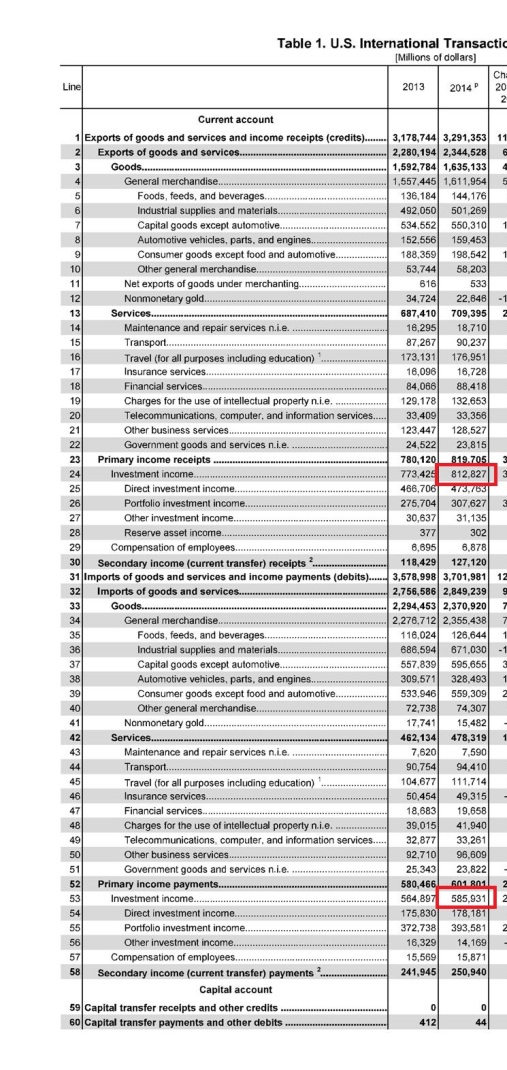

Back to the international investment position. There are a lot of interesting things about it. Although the U.S. in a huge debtor to the rest of the world, the return on assets held by resident economic units of the United States earn more than paying on liabilities to nonresidents. So according to the BEA release U.S. International transactions 2014, investment income in the full year was about $813 billion while income payments was about $586 billion. (More complication arises from “secondary income”).

In addition, revaluations of assets and liabilities also affect the international investment position and revaluations of direct investment held abroad has acted in the United States’ favour.

Of course this cannot always be the case. Take a simple example: Suppose an economic unit’s assets is $100 and liabilities is $150 and suppose assets earn 8% every year and interest paid on liabilities is 5%. So even though the economic unit has a net indebtedness of $50, it is earning

$100 × 8% − $150 × 5% = $0.5

However, if liabilities rise to $160 and beyond the net return turns negative.

In a similar way, there is a tipping point, beyond which the net primary income of the current account of balance of payments turns negative. Because the United States has a negative current account balance and the deficit adds to the net indebtedness every year, at some point in the future, the international investment position may reach a tipping point.

All this sounds as if domestic demand and output are unrelated. This is of course not the case. Imports depend on domestic demand and exports depend on economic activity abroad. Hence the constraint on output at home because if output were to rise fast, the net indebtedness of the United States will also rise fast.

Of course the concept of a tipping point may itself be misleading. Indebtedness can keep rising even if net primary income turns negative without any trouble in financial markets because it all depends on how the financial markets see the problem. But it may be said that once a tipping point is reached, the debt will start to rise much faster than now. My article here hasn’t gone into any analysis here with numbers but I will leave it for another day.

Paul Krugman seems to have been thinking on issues related to open economy monetary macroeconomics these days! He has recently warned his readers to not confuse accounting identities with causation but in a recent blog post he seems to be doing it himself.

So Krugman says:

So, here we go. Start from the observation that the balance of payments always balances:

Capital account + Current account = 0

where the capital account is our sales of assets to foreigners minus our purchases of assets from foreigners, and the current account is our sales of goods and services (including the services of factors of production) minus our purchases of goods and services. So in the hypothetical case in which foreigners lose confidence and stop buying our assets, they’re pushing our capital account down; as a matter of accounting, then, our current account balance must rise.

But what’s the mechanism? (Remember the fallacy of immaculate causation.) The answer is, it depends on the currency regime.

Strange. The last statement in the quote warns of potential mistake which is present in the previous statement! ie Krugman wants to have it both ways.

So “… as a matter of accounting …” ?

Let us consider a case (fixed exchange rate or floating) where there is an autonomous capital flow – such as a foreigner liquidating a bond and repatriating funds. This by itself doesn’t affect the current account. In fact it can be compensated by some accommodative flow in the capital account of the balance of payments.

[accommodative capital flows] take place only because the other items in the balance of payments are such as to leave a gap of this size to be filled … [while] autonomous payments … take place regardless of other items in the balance of payments.

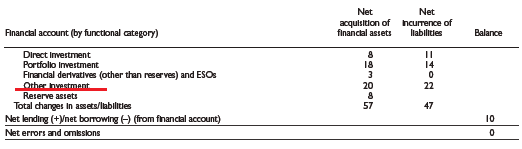

Of course because of flexible exchange rates, the distinction can become blurred but the same is also true in fixed exchange rates. So we have an item called Other Investment in the capital account of balance of payments – like the example in the IMF’s BPM6 (note: “financial account” in the BPM6 terminology, capital account means a different thing):

In addition Reserve Assets is also one. Again this is somewhat of a simplification and it is possible for other items to accommodate.

“Other Investment” is typically banking sector flows but refer to BPM6 for the full definition. “Reserve Assets” is things such as sale or purchases of foreign currency by the central bank or any other official institution. Sometimes a category Exceptional Financing is used – such as government borrowing in foreign currency in exceptional circumstances or official financing transactions from the IMF.

So changes in some items in the capital account can be balanced by changes in some other account in the capital account and not the current account. Of course this doesn’t mean that there is no causality from the capital account to the current account and I will come to it in a moment but what Krugman says is silly.

Let’s take a few examples starting with the simplest – and you guessed it right – the Euro Area 😉

Suppose there is a capital flow where a German financial firm liquidates Spanish government bonds and transfers funds back home.

As I have explained in posts long back, this will lead to a TARGET2 imbalance in which the Spanish NCB will have a rise in indebtedness to the ECB (which is considered to be a Spanish non-resident). Either it ends here or the Spanish banking system will try to attract funds from abroad. In either case there is an accommodative flow in the balance of payments – balancing the initial outflow and without affecting the current account.

Now take the example of a nation with its currency pegged to another anchor currency. Suppose a nonresident economic unit sells sells securities and transfers funds outside the country. Since banks acts as dealers in the foreign exchange markets, this leaves the banking system with a short position in foreign currency. It may try to close it by borrowing in foreign currency or try to attract funds from outside. In the latter case that is all there is to it (in the short term) and this flow is accommodating and will appear in Other Investment. In the former case, the banking system is left with an open position in foreign currency. As long as the bank’s own risk management or the central bank (with the confident knowledge that it has sufficient foreign exchange in case it has) thinks this it is alright, this is what there is for the short term. Else banks may need to attract funds from abroad. However if there is a depreciation outside the tolerable band (fixed doesn’t mean god has fixed it) in response to a huge amount of capital outflow, the central bank may sell foreign currency. It may also try to hike interest rates to get attract foreigners.

Again no change in the current account. One item in the capital account cancels another to preserve the accounting identity Krugman quotes.

In floating exchange regimes this is more complicated but the story is not too different from the BoP viewpoint. An outflow of funds will be accommodated by banks’ open position (or inventories). Banks will typically try to offload the inventories depending on market conditions and opportunities and it is sometimes said in the fx microstructure theory that the inventory half-life is around 15 minutes. The currency will depreciate to the point where expectations of the market participants reverse in the direction of appreciation bringing in flows in the opposite direction to the initial capital outflow. How this works precisely is a very challenging open question. Of course looked at from a medium term perspective, in general, it is not immediately obvious why the current account balance and capital account sum to zero since the magnitude of “Portfolio Investment” and “Direct Investment” may be quite different from the current account balance. But the sum of balances is zero as a matter of accounting. In such cases, banks may try to attract funds from abroad themselves by marketing bonds offshore – i.e., they may try to find offshore funding. More complications arise from derivative contracts with nonresidents which is not easy to go into in this post.

Of course this not guaranteed to work – pure float is the luxury of a few nations – and sometimes the central bank may need to intervene in the foreign exchange markets and in the extremis, undertake exceptional financing transactions such as borrowing from the IMF.

In recent times, the Reserve Bank of India had an interesting swap scheme with the banking system who would attract funds from abroad.

Of course, none of this means there is no causality from the capital account to the current account. A nation may face troubles financing its balance of payments and it may try to deflate domestic demand by fiscal and monetary policy to keep its current account imbalance from getting out of hand. It is important to note here this is not a straightforward result of the identity but there is a more complicated story and that output suffers because of this. Krugman makes it sound as if nothing happens to output.

Phil Pilkington takes an issue with Sergio Cesaratto on the usage of the phrase “balance-of-payments crisis” on problems of the Euro Area.

Phil’s argument is that typically nations facing balance of payments problems need foreign currency and it manifests itself as a depreciation of the domestic currency but in the Euro Area this isn’t the case (because the exchange rates are fixed irrevocably between the Euro Area nations by the national central banks and the ECB). So the usage of the phrase “balance-of-payments crisis” is an abuse of language.

Now, to be short my argument that there is nothing wrong with the usage is because of the definition of what “balance-of-payments” actually is. Here is why:

A balance of payments transaction is a transaction between residents and non-residents. It is not relevant in which currency the transaction really is. So if you were a U.S. resident and if I as an Indian pay you $1 in New York in person, it is still a balance of payments transaction from the viewpoint of the United States. (of course if I own a firm in the United States which pays you then it is not a balance of payments transaction because the firm would be a resident).

In this way it becomes clear that some Euro Area nations have a balance of payments financing problem and since it reached a crisis level, the problem can be classified as a balance of payments crisis even though there is no exchange rate which has collapsed.

The nations which were/are in troubled had difficulties because they had huge current account deficits and as a result became indebted to the rest of the Euro Area. This became unsustainable and turned into a crisis. And both borrowers and lenders are to be blamed.

Since these nations had huge indebtedness to the rest of the Euro Area, they had troubles borrowing and refinancing their debts with foreigners and still have.

So I do not know why someone can take an issue with the phrase “balance-of-payments crisis”.

Except for the huge depreciation of the domestic currency, the Euro Area economic dynamics resembles a typical balance-of-payments crisis in all other ways. There is deflation of domestic demand, financial instability, high unemployment, increase in poverty and decrease in happiness and standard of living etc. There is international help in both cases.

Once again. A BoP transaction is between residents and non-residents. (See 2008 SNA, and BPM6 on this). A BoP crisis hence is a crisis in which borrowing and refinancing existing debt from non-residents has become difficult and is at crisis levels. Whatever a country such as Portugal does at the moment, some units will be left indebted to the rest of the world/Euro Area. This is because liabilities are greater than financial assets and the difference is the net indebtedness to foreigners. Whatever new debts are created are equal in value to newly created financial assets. So the arithmetic dictates foreigners should be relied upon. The one qualification is that Portugal significantly improves its net exports but that is the same as saying its balance of payments is improving.

So anyone saying it is not a “balance-of-payments crisis” is fooling himself/herself.

Recently India is going through a mini-crisis where its currency has plummeted and with hosts of other reasons such as high inflation and a dysfunctional government not just because of the ruling party but also because of the opposition. In all this corruption has risen a lot. During the last few weeks, the Reserve Bank of India – the central bank – has tried to fight the depreciation of the rupee by taking various steps but in spite of this, the currency kept depreciating.

Unsurprisingly, a blame game has begun. To some extent it is good. It shows that the subject Economics isn’t what it has pretended to be – else we would never have had these debates. Simon Johnson recently wrote an article India’s Economic Crisis for NYT’s Economix which once again reminded economists of how dangerous the ideology that financial crisis are a thing of the past can be.

Initially some section of the media made it appear as if the Reserve Bank of India governor is blaming it on the “tapering” of the large scale asset purchases of the U.S. Federal Reserve. In fact an RBI release appeared to say it explicitly. But the RBI governor Duvvuri Subbarao has of course clarified saying that it was just a trigger but put the blame on India’s Finance Minister.

Economists seem to blame the Reserve Bank of India (and the supposed “fiscal indiscipline” of the government). According to them the RBI created a panic of sorts by reacting and this exacerbated the pressure on the Indian Rupee. So according to Swaminthan Aiyar, an economist who wrote an article titled India’s Problem Is Exports, Not the Rupee,

A falling rupee is a political, not an economic disaster

How silly can that get. While the title is okay (India needs more exports), but the above slogan just echoes the thought held among economists that the central bank shouldn’t interfere in the currency markets and that somehow the currency may have stabilized. Criticising the Reserve Bank is like criticising someone under attack for trying to defend (but failing to defend properly). It is important to realize that this “there is always a price” notion is an ideology of economists – a depreciation of a currency says something about it acceptability in international markets. So the fear is that the Rupee may become unacceptable in international markets and go to the IMF for help to refinance its international debts and the pound of flesh demanded in return. If the Rupee continues to depreciate, there will be further outflow of foreign funds and domestic banks will come under tremendous pressure in the foreign exchange markets in which they act as dealers. Perhaps Aiyar needs some lessons from Simon Johnson.

Paul Krugman suggests that India’s net international investment position hasn’t deteriorated and wonders what the issue really is. While it is true that India’s NIIP is not as worse as countries such as Hungary, there is no hard and fast rule that minus 20% is good and minus 100% is bad. India’s currency doesn’t have a brand and acceptability in international markets and 20% can be bad considering the direction in which it is headed given the current account deficits.

The silliest thing I heard (saw actually in a Tweet) is: Japan’s currency is depreciating and that is not a crisis but India’s currency is depreciating and that is a crisis – isn’t that self-contradictory? No it isn’t. Japan is a net creditor to the rest of the world and can talk up its currency as fast as it talked down its Yen. Japan is in a position where it instead can boost domestic demand instead of beggaring its neighbours.

There are other blame games as well. There has been a sharp rise in corruption – or perhaps it is more right to say that such cases have come to the limelight while it has always existing at a large scale. So this has caused India’s troubles. Although there is truth to it, this by itself doesn’t cure India’s external problems. Imagine if these problems hadn’t existed and that there was a rapid rise in output (which anyway is not bad compared to the rest of the world). The rise in output would come about with a rise in domestic demand and this would have also led to a rise in imports deteriorating the balance of payments.

One frequent slogan when such troubles arise in the external sector – and which has been repeated recently – is “increase productivity”. While increase in productivity is welcome (so long as it accompanies a rise in production), this is separate from relative competitiveness with the rest of the world. It is true that a rise in productivity can have some effects on competitiveness but the causality is quite different from what economists generally assume. The major cause of rise in productivity is the rise in production itself and if a nation faces a balance of payments constraint, its production is affected because of deflationary means need to be adopted to keep imports in check.

During the financial and economic crisis which began around 2007, India was the among the first nations to boost domestic demand by fiscal policy. India was already a Keynesian when the phrase “we are all Keynesians” became popular. India has done the opposite of the beggar-my-neighbour policies but has run out of steam and it is time the world boosts domestic demand and ease the constraint on the few “emerging markets” in the news.

It is a deep bias in the economics profession that balance of payments imbalances have a self-adjusting market mechanism. In the years of the Bretton-Wood it was thought that the Mundell-Fleming fixed exchange rate models explained how imbalances would self-correct. But this proved to be wrong. After the fall of the Bretton-Woods, when exchange rates floated, it was thought that there is a market mechanism via prices changes (exchange rate) to keep imbalances in check but – with exceptions of a few – economists again failed to notice their bias with their focus being shifted by Milton Friedman’s Monetarism who also hand-waved the “market mechanism” in order to promote free trade. India’s troubles is another reminder of how their intuitions are wrong. Instead of changing it, they simply blame the government.

It is time for the rest of the world to first boost domestic demand so that India’s exports rise to pay for its imports. This is beneficial to the world itself because it will enjoy more imports. Some criticisms of the Indian government are true but this alone is far from sufficient in solving India’s problems. More importantly, there is no market mechanism to resolve imbalances – a drastic change in coordination of fiscal and monetary policies combined with trade policies which are mutually consistent and beneficial are required.

In a short recent speech, the Indian Prime Minister – the great man who steered the direction of the Indian economy in the early 1990s – says:

The purpose of the study of economics is not to provide settled answers to unsettled and difficult questions, but sometimes to warn economists and the world-at-large, how not to be misled by clever governments.

which is similar to what Joan Robinson once:

The purpose of studying economics is not to acquire a set of ready-made answers to economic questions, but to learn how to avoid being deceived by economists.

– in “Marx, Marshall And Keynes”, Occasional Paper No. 9, The Delhi School of Economics, University Of Delhi, Delhi, 1955.

I’d say Manmohan Singh doesn’t go as far as Robinson in putting the blame on economists themselves but I guess there is some amount of influence. But what Singh says is true – governments of advanced nations mislead the less advanced ones.

Also in the short speech:

I would like to say, that when we study economics, our impulse is not the philosopher’s impulse – knowledge for the sake of knowledge – but for healing that that knowledge may help to bring. These are the words of past thinkers: Wonder is the beginning of philosophy; but it is not wonder, but social enthusiasm, which revolts against the silence of fixed life, and the orderliness of the mainstream, which is the beginning of economic science.

Which is not not surprising since Manmohan Singh is influenced by Joan Robinson and Nicholas Kaldor. Here is a nice interview by the BBC’s Mark Tully from 2005 Architect Of The New India published in the October 2005 issue of the Cambridge University Alumnus Magazine.

Here is an excerpt from the interview:

The thinking behind his solutions to India’s financial problems was first shaped at Cambridge by the theories of John Maynard Keynes. The great man had died almost 10 years before Manmohan Singh arrived but his legacy was still very much alive. ‘At university I first became conscious of the creative role of politics in shaping human affairs, and I owe that mostly to my teachers, Joan Robinson and Nicholas Kaldor. Joan Robinson was a brilliant teacher but she also sought to awaken the inner conscience of her students in a manner that very few others were able to achieve. She questioned me a great deal, and made me think the unthinkable. She propounded the leftwing interpretation of Keynes, maintaining that the state has to play more of a role if you really want to combine development and social equity.’

‘Kaldor influenced me even more; I found him pragmatic, scintillating, stimulating. Joan Robinson was a great admirer of what was going on in China, but Kaldor used the Keynesian analysis to demonstrate that capitalism could be made to work. So I was exposed to two alternative schools of thought. I was very close to both teachers, so the clash of thinking sometimes got me into difficulties. But that made me think independently.’

In Other News

The Reserve Bank of India announced some measures recently to curb the instability of the Indian Rupee:

The first announcement – effectively raising short term interest rates and which caught everyone by surprise – was on 15 July 2013:

The market perception of likely tapering of US Quantitative Easing has triggered outflows of portfolio investment, particularly from the debt segment. Consequently, the Rupee has depreciated markedly in the last six weeks. Countries with large current account deficits, such as India, have been particularly affected despite their relatively promising economic fundamentals. The exchange rate pressure also evidences that the demand for foreign currency has increased vis-a-vis that of the Rupee in part because of the improving domestic liquidity situation.

Against this backdrop, and the need to restore stability to the foreign exchange market, the following measures are announced:

Over the last two months, the Reserve Bank of India (RBI) has undertaken several measures to contain the volatility in the foreign exchange market. Among them, some measures intended to check excessive speculation adding to undue volatility in market conditions were instituted vide the RBI’s Press Release No.2013-2014/100 dated July 15, 2013. These measures have had a restraining effect on volatility with a concomitant stabilising effect on the exchange rate. Based on a review of the measures, and an assessment of the liquidity and overall market conditions going forward, it has been decided to modify the liquidity tightening measures as follows:

Thomas Palley has a new article Coordinate Currencies or Stagnate on international coordination of exchange rates. (h/t Matias Vernengo). He has a nice small critique of the Chicago school according to which “market forces” work toward resolving imbalances.

It is great such a thing has been raised because the importance of policy coordination (in general – monetary, fiscal and exchange rates) is often forgotten.

In an article Agenda For International Coordination Of Macroeconomic Policies, Tobin wrote [1]

Coordinate policies! So economists urge governments. Financiers, journalists, pundits, politicians take up the cry. Central bankers and finance ministers agree, as do presidents and prime ministers. They meet, they talk, they announce progress. It turns out to amount to very little…

But the global imbalance has worsened and it has now created a situation in which such coordination is more badly needed.

Wynne Godley had been warning of such things in the 2000s. In a 2005 article [2] with his collaborators, he wrote:

A resolution of the strategic problems now facing the U.S. and world economies can probably be achieved only via an international agreement that would change the international pattern of aggregate demand, combined with a change in relative prices. Together, these measures would ensure that trade is generally balanced at full employment…Those hoping for a market solution may be chasing a mirage.

I have also found the last words in academic literature very insightful [3]:

… It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

Time will tell how right he was 😉

References

James Tobin, Agenda For International Coordination Of Macroeconomic Policies, Ch 24, p 633, Essays In Economics, Volume 4: National And International, The MIT Press, 1996.

Wynne Godley, Dimitri Papadimitriou, Claudio Dos Santos and Gennaro Zezza – The United States And Her Creditors: Can The Symbiosis Last?, Levy Institute Strategic Analysis, September 2005. Link

Wynne Godley, Dimitri Papadimitrou and Gennaro Zezza – Prospects For The United States And The World – A Crisis That Conventional Remedies Cannot Resolve, Levy Institute Strategic Analysis, December 2008. Link

Why are current account deficits a haemorrhage in the flow of circular income? Weak external trade performance implies a drain in demand and hence pressure on the path to full employment and also that fiscal policy has to give in: else public debt and net indebtedness to foreigners keep rising relative to output which cannot be sustained for long. This means that if an individual nation or the world as a whole needs reflation, drastic changes need to made on how the world is run – especially using a system of regulated international trade rather than a system of free trade.

Nicholas Kaldor had a lot of change of mind about exchange rates during his lifetime. In the introduction to Volume 6 of his collected essays Further Essays On Applied Economics, he has a lot to say about his views.

Nicky Kaldor also had a paper The Relative Merits Of Fixed Exchange And Floating Rates – a memorandum as an economic adviser to the Chancellor in 1965 in which he was arguing for the merits of floating the exchange rates. In page xiii from introduction to Further Essays On Applied Economicshe confesses:

The strategy advocated in my 1965 paper “The Relative Merits of Fixed and Floating Exchange Rates” thus proved in practice futile …

… So the policy which I advocated in the 1960s and developed at greater length in my 1970 Presidential Address to the British Association,of reconciling full employment growth with equilibrium in the balance of payments through adjusting the relationship between import and export propensities by a policy of continuous manipulation of the exchange rate, proved in the event a chimera. The main reason for this was that (along with most economists) I greatly overestimated the effectiveness of the price mechanism in changing the relationship of exports to imports at any given level of income. The doctrine that exports and imports are kept in balance through induced changes in their relative prices is as old and deeply ingrained as almost any proposition in economics.

So there you have it – realising his mistake earlier than anyone else.

He goes on further to drive this point:

… In other words, what the Harrod theory asserts is that trade is kept in balance by variations of production and incomes rather than by price variations: a proposition which implies that the income elasticity of demand of a country’s inhabitants for imports and those of foreigners for its exports are far more important explanatory variables than price elasticities.

which is essentially saying that it is non-price competitiveness which is far more important than price competiveness.

Further …

… If the Harrod theory provides the realistic explanation of the underlying forces which maintain the trade flows of an industrial exporter in balance (subject, of course, to the exceptions to this rule in the shape of long-term surplus and deficit countries, which must be capable of being explained in the same framework) this also carries the implication that the relationship of import propensities to exports will be relatively insensitive to such variations of relative prices as can be accomplished by monetary or exchange rate policies.

This latter implication (though discussed in the 1930s) seems to have got lost when the debate on fixed versus flexible exchange rates flared up again in the 1960s. This explains perhaps the exaggerated hopes placed on variations in exchange rates as an instrument of the “adjustment process” in international trade and payments and, for Britain in particular, on a system of “managed floating” as a means of securing higher and stable growth rates.

Again he later emphasises his learning:

… I was convinced that once exchange rates are freed from the rigidities imposed by Bretton-Woods, the forces of cumulative causation which made some countries grow fast and others slowly will no longer operate, or not in the same manner. That belief was so badly shaken by experience of subsequent years for for reasons explained in my most recent paper on the subject, which is discussed below.

I believe that the basic problem today is not the exchange rate regime, whether fixed or floating. Debate on the regime evades and obscures the essential problem.

Of course that doesn’t mean one ties both shoes together and irrevocably fixes exchange rates (and give up the government powers to make drafts at the central bank) but the essential problem referred above – although gets diluted – doesn’t go away outside a monetary union.

Cyprus has recently received the attention of academicians and financial professionals in recent weeks. Need I say that?

So national bankruptcy is to be resolved by winding down a bank, moving guaranteed deposits (i.e., upto €100,000) to another and as per the latest Reuters article on this, big numbers (anywhere ranging from 20 to 40 per cent loss on deposits on amounts over €100,000) are quoted.

The current plan is closer to what one would wish to see in an orderly bank resolution. Laiki Bank is to be split into good and bad banks. Deposits of less than €100,000 in the bank and assets worth €9bn – the sum owed to the central bank as part of its liquidity support – will be transferred to Bank of Cyprus. The remainder will be wound down. Those with claims to deposits in excess of €100,000 will obtain whatever the value of the bad bank’s assets turns out to be.

Meanwhile, savers at the Bank of Cyprus with deposits of more than €100,000 will have their accounts frozen and suffer a “haircut” of still unknown size. That reduction in value is likely to be large: perhaps 40 per cent. Finally, temporary exchange controls are to be imposed.

Why are the reasons for such huge numbers?

The reason is that the nation has accumulated huge net indebtedness to foreigners over years and this has been financed by banks raising deposits from foreigners, so that if debt traps are to be avoided, foreigners are to be required to take losses.

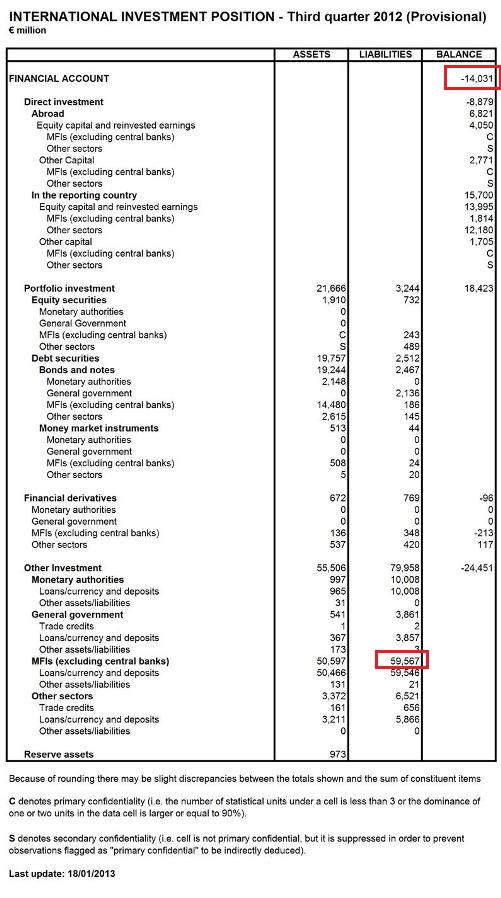

The following is the international investment position of Cyprus at the end of Q3 2012 (source: Central Bank of Cyprus)

In the balance of payments literature, banks’ position is referred as Other Investment. Also, the above refers to a Financial Accountbut it really means net IIP. Ideally it would have been better if this data had been updated but the above information is useful nonetheless.

As a percent of gdp, the net IIP position (with the opposite convention to standard usage) was 81.1% (Source: Eurostat) which is big in itself but very much lower than the now famous banks’ liabilities to foreigners/Russians! (the second red box above).

If a nation wants to resolve bankruptcy, it is better to do it by imposing losses on foreigners – especially if an international lender of last resort is available! And if this is to done it in the optimal way, best to do it once – rather than keep doing it. The ratio of two red boxes in the table – i.e., net liability as a proportion of gross bank liabilities to foreigners is 24.56%.

So Cyprus needs to wipe out about this amount as a percent of deposits roughly. It is not necessary to reach a position of zero indebtedness but something low such as 10% of gdp is ideal. Some buffer is needed because there will be leakages in spite of capital controls – requiring fire sale of foreign assets (and subsequent losses) by banks or borrowing from the ECB which may want to ensure that banks have good collateral for the ELA. Foreign deposits below €100,000 shouldn’t be hit. So “net-net”, as a percentage, this may be higher than 24.56%. All this depends on the latest situation and the distribution of foreign deposits and also the distribution between residents and foreigners but 24.56% of deposits is a good starting point – it gives a rough estimate of the order of magnitude of the problem.

At any rate, losses imposed on foreigners have to be big for the ECB and Euro Area governments to stand behind.