A few readers/commenters of my blog brought attention to a video of Warren Mosler where he claims that “there is no such thing as a capital flight” – presumably for a nation with a “sovereign currency” with the implication that a Euro Area nations can simply leave the Euro and adopt their original currency without a fear of capital flight post the event.

(Why have capital controls then, if that’s the case?)

This claim can be easily dismissed by simple balance of payments analysis.

For this I use the IMF’s Balance of Payments Manual (BPM6). First lets look at the format of the BPM6’s numerical example.

The example is below:

(click to enlarge)

Roughly Mosler’s argument is that if a foreigner sells assets denominated in the domestic currency, some other foreigner would need to buy it.

He gives a Bretton-Woods anti-analogy where – presumably – an official foreign creditor can demand gold for conversion and repatriate it home by ship. And that since official convertibility to gold is suspended, there is no capital flight according to this mini-story.

To see there is capital flight, one needs to look at the foreign exchange market microstructure. By the way, the Neochartalists erroneously tend to treat banks as brokers (as opposed to dealers) in the foreign exchange markets. Let us say a foreigner – perhaps a financial institution – with “portfolio investment” in the country in question liquidates assets in the domestic currency and exchanges it at a domestic bank (domestic with respect to the country we are discussing). This “order flow” leaves the bank with a short position in foreign currency which it will try to eliminate. This will lead to a cascading effect because the foreign dealer it may want to offload its position will react itself and hence a series of transactions in the fx markets – leading to a depreciation of the currency.

It may happen that the currency depreciation may bring in an order flow in the opposite direction – thereby leading to a quasi-equilibrium. However if the general expectations is such that the currency may depreciate further then it is hard. If such expectations are formed, there may be even more capital ouflow!

It is precisely here that the central bank may intervene and sell foreign reserves – thereby helping the dealers (both domestic and foreign to offload their undesired positions). So recently there was news of intervention by the Reserve Bank of India in the fx markets. (minor technicality: the reduction of domestic banks’ settlement balances due to the settlement of central bank fx sales will lead to a “fine tuning reverse operation” by the central bank)

So how does the whole thing look in the balance of payments? The answer is very simple: assuming foreigners sold 100 units of assets – minus 100 due to liquidation of domestic assets and minus 100 due to sale of reserve assets.

Some time back I had started with the first part of a series of posts on this topic: see Balance Of Payments: Part 1. From the same post, here’s from the Australian Bureau of Statistics’ manualBalance of Payments and International Investment Position, Australia, Concepts, Sources and Methods, 1998

(click to enlarge)

So we have the current account, the financial and the international investment position at the beginning and end of each accounting period. In addition we have, revaluations on assets and liabilities. These arise due to change in the value of assets (such as rise in stock markets) and due to movement of the exchange rate or both.

Also, textbooks use a slightly different language than official statistics and manuals. Textbooks simply use the phrase capital account when they mean the financial account.

I aim to go into each of this and the behaviour of institutions who are involved in the whole process and how it leads to changes in assets and liabilities of all sectors and the consequences. We will see how endemic current account deficits act as a hemorrhage in the circular flow of national income as Wynne Godley would put it and decides the fate of nations as Anthony Thirlwall may have it.

To really appreciate, one needs to have a strong methodology for studying this. One way is to use G&L’s transactions flow matrix but it can get complicated in case of two nations. Needless to say, from a modeling perspective, it is more useful than the usual way of studying balance of payments. However, for appreciating G&L methodology one needs to first understand the usual way of studying this.

Double Entry Versus Quadruple Entry Bookkeeping

In contrast to national accounts, Balance of Payments is based on double entry bookkeeping. Here’s from the IMF’s Balance of Payments And International Investment Position Manual (BPM6), pg 9:

The balance of payments is a statistical statement that summarizes transactions between residents and nonresidents during a period. It consists of the goods and services account, the primary income account, the secondary income account, the capital account, and the financial account. Under the double-entry accounting system that underlies the balance of payments, each transaction is recorded as consisting of two entries and the sum of the credit entries and the sum of the debit entries is the same.

In contrast, national accounts as per SNA2008 or G&L’s way of doing it uses quadruple entry bookkeeping who point out in their book Monetary Economics that:

… Copeland pointed out that, ‘because moneyflows transactions involve two transactors, the social accounting approach to moneyflows rests not on a double-entry system but on a quadruple-entry system’. Knowing that each of the columns and each of the rows must sum to zero at all times, it follows that any alteration in one cell of the matrix must imply a modification to at least three other cells. The transactions matrix used here provides us with an exhibit which allows to report each financial flow both as an inflow to a given sector and as an outflow to the other sector involved in the transaction.

The structure of an economic model that is relevant for a capitalist economy needs to include the interrelated balance sheets and income statements of the units of the economy. The principle of double entry book keeping, where financial assets are liabilities on another balance sheet and where every entry on balance sheet has a dual in another entry on the same balance sheet, means that every transaction in assets requires four entries.

The System of National Accounts 2008 (2008 SNA) says (page 21):

In principle, the recording of the consequences of an action as it affects all units and all sectors is based on a principle of quadruple entry accounting, because most transactions involve two institutional units. Each transaction of this type must be recorded twice by each of the two transactors involved. For example, a social benefit in cash paid by a government unit to a household is recorded in the accounts of government as a use under the relevant type of transfers and a negative acquisition of assets under currency and deposits; in the accounts of the household sector, it is recorded as a resource under transfers and an acquisition of assets under currency and deposits. The principle of quadruple entry accounting applies even when the detailed from-whom-to-whom relations between sectors are not shown in the accounts. Correctly recording the four transactions involved ensures full consistency in the accounts.

Simple example: your and my favourite: loans make deposits. The following is a transaction where a household has borrowed some funds from the banking sector:

Introduction To Current Transactions

I mentioned that in recording transactions between residents and nonresidents and presenting it as balance of payments, national accountants use double entry bookkeeping (as opposed to quadruple), so any transaction in the current account necessarily involves another entry in the financial account (ignoring barter and accidental cancellations). However, the opposite is not the case: a transaction on the financial account will lead to another entry in the financial account and not directly in the current account. A purchase of US equities by a UK resident cannot be said to cause or increase the US current account deficit.

One example: if you are are US citizen travelling to the UK and have pay for coffee at the London airport by paying in Federal Reserve notes, it will give rise to an entry in the current account (credit from the perspective of the UK balance of payments) and a debit (increase in assets of UK residents: change in currency notes). This is just transaction among thousands and the question is how is all this to be recorded and more importantly (later) what does it tell us.

Here’s how a standard balance of payments table looks like (note: this does not include international investment position)

(source: UK Pink Book 2011; click to enlarge)

We will go over details in the next post in this series. For now let us see how this looks for the example presented earlier: A US traveller pays $10 for coffee at the London Heathrow airport with Federal Reserve currency notes. Assuming the current exchange rate, the following (double) entries need to be included in the UK balance of payments:

£

Credits

Debits

Current Account

Goods and Services

6.328

Financial Account

Bank Deposits, Foreign Currency Assets

6.328

This is a simple example – hardly needing so much background and information but in the next post in this series, we will look at complicated examples where intuitions can easily go wrong. If the above were the only transaction between UK and US residents in the accounting period (quarter/year), this will also change the US indebtedness to the UK by £6.328 or $10 and this will be shown in the international investment positions of the UK and the US. If the exchange rate had moved from the start of the period, revaluations would need to be done to record the closing stocks of assets and liabilities.

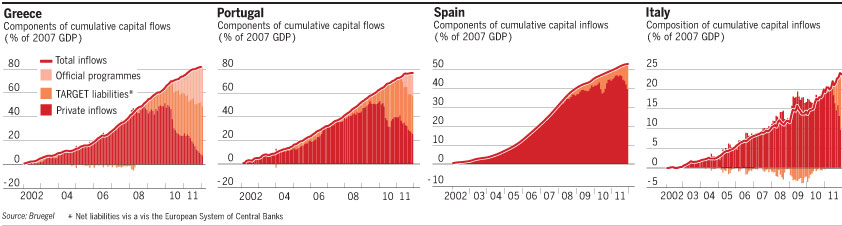

Due to the continuing capital flight out of Spain, the TARGET2 liabilities of Banco de España increased in April and averaged €284.5bn in the month. The flow equivalent in the balance-of-payments language may be called the accommodating item.

If a government (outside monetary unions) can make a draft at the central bank, why do rating agencies rate governments’ creditworthiness?

In this post, I will attempt to describe the dynamics of defaults and restructurings by going through some monetary economics of open economies.

Carmen Reinhart and Kenneth Rogoff wrote a book in 2009 titled This Time Is Different: Eight Centuries Of Financial Folly or simply This Time Is Different arguing that governments do indeed default – both in debt denominated in the domestic and foreign currencies. They blame the public debt and the government for the public debt – hence giving the innuendo that governments across the planet should attempt to cut public debt by tight fiscal policies. This is an illegitimate conclusion – on which I will say more below.

At another extreme are the Chartalists who argue that the government cannot “run out of money” and hence fiscal policy has no monetary constraints. Sometimes they qualify this statement by saying that the currency they are discussing are “sovereign currencies”. Now, there are various definitions of what a sovereign currency is but it is frequently pointed out by them that nations who have seen restructuring of government debt did not have a “sovereign currency” – because the currency is either pegged or fixed or it is the case that the government had a lot of debt in foreign currency which presumably allows defaults/restructuring of government debt in the domestic currency as well. The motivation behind this is Milton Friedman’s idea that nations should freely float their currencies in international markets and that markets will clear and that the State intervention in the currency markets can only make things worse. Hence Reinhart/Rogoff don’t prove them wrong – according to them – since the situations are supposedly different.

We will see that while there is some truth to it, the notion of a “sovereign currency” is highly misleading. Such intuitions are coincident with the incorrect notion that indebtedness to foreigners (in domestic currency) is just a technical liability and there’s nothing more to that!

Here’s S&P’s article on the methodology it uses to assign ratings on governments: Standard & Poor’s – Sovereign Government Rating And Methodology. One can see the importance it gives to the external sector. However, S&P does not provide a mechanism on how a government will finally end up defaulting. The purpose of this post is to look into this.

Before this let us make a connection between the public debt and the net indebtedness of a nation. Most people in the planet confuse the two. The former is the debt of the government whereas the latter is the (net) indebtedness of the nation as a whole. This is the net international investment position (adjusting for traditional settlement assets such as gold) with the sign reversed. This can be obtained by consolidating all the sectors of an economy and the consolidation involves (for example) netting of the assets of the domestic private sector held abroad and also its gross indebtedness to the rest of the world.

So one can think of two extremes:

Japan – with a high public debt of about 195% of gdp (includes just the central government debt), while being a net creditor of the world. It’s NIIP is about 50% of gdp (data source: MoF, Japan)

Australia – with a low public debt of 18% of gdp and NIIP of minus 59% of gdp.

So in the case of Japan, while the government is a huge debtor, the nation as a whole is a creditor, whereas in the case of Australia, it is the opposite. So the rating agencies get it wrong or opposite!

Let us first assume a closed economy. The greatest starting point in analyzing economies is the sectoral balances approach. For a closed economy it is:

NAFA = DEF

where NAFA is the Net Accumulation of Financial Assets of the private sector and DEF is the government’s budget deficit. If the private sector wants to accumulate a lot of financial assets, and the government wants to run the economy near full employment, the public debt will be higher, the higher the propensity to save, for example. (This is not as straightforward as presented here but can be shown in a simple stock-flow consistent model). So unlike what neoclassical economists think, the level of public debt is somewhat irrelevant. Neither does the government has too much trouble in financing its debt because the public debt is the mirror image of the private sector net financial asset position.

Now let us take the case of an open economy. The sectoral balances identity now is

NAFA = DEF + CAB

A deficit in the current account implies an increase in the net indebtedness to foreigners. Unless the markets miraculously clear with the exchange rate adjusting to bring the CAB in balance, a deficit in the current account implies the nation as a whole has to attract foreigners to finance this deficit i.e., via a lower NAFA or higher DEF. In the long run, the private sector is accumulating financial assets (or has small positive NAFA) and the whole of the current account balance is reflected in the public sector balance.

So the debate fixed vs floating doesn’t help too much. A relaxation of fiscal policy may spill over into higher imports with the public debt and the net indebtedness to foreigners keeps rising forever to gdp. Hence nations typically have to curb growth to bring the current account into balance.

This is theory. So let’s look at an open economy mechanism of an event of default by the government as a story.

In the following, I will use the phrase “pure float” instead of the dubious terminology “sovereign currency”.

Here’s the simplest model:

In the above, a nation with its currency on a pure float and with zero official sector liabilities in foreign currencies has a somewhat weak external position in 2012. Now, according to some of the Neochartalist arguments this nation can’t default on its government debt. However this is a wrong conclusion as the scenario above hightlights. In the scenario constructed, the balance of payments position weakens over the years (and I have mentioned that roughly in 2020 it weakens). In 2022, foreigners are no longer willing to finance the debt. This may be due to a capital flight or due to the inability of the banking system to maintain a low net open position in foreign currency. The depreciation of the domestic currency isn’t sufficient to clear the fx markets and the official sector (either the central bank or the government’s treasury) necessarily has to intervene in the foreign exchange markets by issuing debt denominated in foreign currency. The government is then acting as the borrower of the last resort and the objective is to use the proceeds to partially have more foreign exchange reserves and/or to sell the foreign currency proceeds from the debt issuance to clear the fx markets. The government is then left with a net liability position in the foreign currency. Soon the external situation worsens to the point requiring official foreign help – such as from the IMF – which promises to help and requires a restructuring of the debt both in domestic and foreign currencies.

Free marketers have a blind belief in the markets and the theories are built on the assumption that markets always clear. The recent crisis has highlighted that this isn’t the case. Even for the case of Australia – whose currency can be considered closed to being pure float – has had issues in the external sector and the Reserve Bank of Australia had to borrow in US dollars from the Federal Reserve (via swap lines) to help Australian banks meet their foreign currency funding needs during the crisis.

Of course the above is not typical but to prevent the external vulnerability to go out of control, governments keep domestic demand low and a lot of times, they over-do this.

The point of the exercise is to prove that it is not meaningless to think of nations becoming bankrupt in whichever situation one can think of and it doesn’t help to laugh at the rating agencies and make fun of them – possibly with the exception for the case of Japan. Statements such as “government with a sovereign currency cannot become bankrupt” are simply misleading. In the above, the Chartalists would argue that the currency was not sovereign and they were not wrong about the default but the currency was sovereign in their own definition in 2012!

Here are some comments on some nations.

Japan: As mentioned above, Japan is a net creditor of the rest of the world and partially as a consequence of that, most of the Japanese government’s debt is held internally. The rating agencies are aware of this but in spite of this continue to make comments on the creditworthiness of the Japanese government. It is possible that residents may transfer funds abroad for unknown reasons (which the raters for some reason suspect) but it may require just a minor interest rate hike to prevent this from happening. Japan has a relatively strong external situation and hence has no issues in financing its government debt.

Canada: Nick Rowe of WCI mentioned to me on his blog that worrying about the balance of payments constraint is like “beating a dead horse” – citing the example of Canada which has floated its currency and it seems has no trouble with its external sector. But this ignores other things in the formulation of the problem. Canada is an advanced nation and an external situation which is not weak. However, a growth of the nation much faster than the rest of the world will lead to a worsening of the external situation. To some extent the nation’s external situation has been the result of its relatively better competitiveness of exporters compared to its propensity to import and a demand situation which either as a conscious attempt of demand management of the government or by pure fluke has helped its external situation remain non-vulnerable.

United States: The US dollar is the reserve currency of the world and slowly over time, the United States has turned from being a creditor of the rest of the world to becoming the world’s largest debtor nation. (Again not due to its public debt but because of its net indebtedness to foreigners). The US external sector is a great imbalance and any attempt to get out of the recession by fiscal policy alone will worsen its external situation leading to a crash at some point. S&P is right! So to come out of the depressed state, the nation has to complement fiscal expansion with improvement of the external situation such as by (and not restricted to) asking trading partners to not revalue their currencies. Still for some reasons bloggers at the “New Economic Perspectives” think that

… Bernanke also knows that the US has infinite ability to finance these fiscal components, that there is no solvency issue and that the policy rate and both ends of the yield curve are under the direct control of the Fed.

Back to This Time Is Different. While Reinhart and Rogoff’s analysis of government debt may be useful, their conclusions can be destructive for the world as a whole. The domestic private sector of a nation needs continuous injection from outside so that it can run surpluses in general and tightening of fiscal policies will lead to a depression. Global imbalances is crucial in understanding the nature of this crisis (and not public debt alone) and even coordinated attempts to reflate economies may provide only a temporary relief. Since failure in international trade restricts the growth of nations and their attempts to reach full employment, what the world needs is an entirely different way to run the economies under managed trade with fiscal expansion. Ideas of “free trade” such as that outlined here by Alan Blinder simply help some classes of society at the expense of others because it relies on the “market mechanism” which has failed over and over again.

This brings me to “sovereignty”. As argued, the concept “sovereign currency” is almost vacuous (except highlighting the problems of the Euro Area) but sovereignty as argued by Wynne Godley in his great 1992 article Maastricht And All That and by Anthony Thirlwall in the same year on FT (my post on it here Martin Wolf Pays A Generous Tribute To Anthony Thirlwall) definitely have great importance. Some of Thirwall’s concepts of economic sovereignty in the article were: the ability to protect and encourage strategic industries, the possibility of designing systems of managed trade to even out payments imbalances, the ability to protect against certain countries with persistent surpluses, differential taxes which discriminate in favour of the tradeable goods sector.

Martin Wolf has just written an article on FT: Why the Bundesbank is wrong questioning the arguments made by Jens Weidmann, president of the Bundesbank. (This speech: Rebalancing Europe).

This chart is interesting:

(click to enlarge)

Wolf says:

Arguably, the crucial step is to agree on the nature of the illness. On this, progress is now being achieved, at least among economists. It is widely accepted that the balance of payments is fundamental to any understanding of the present crisis. Indeed, the balance of payments may matter more in the eurozone than among economies not bound together in a currency union.

I am not sure how widely accepted or understood this is, but it’s exactly right!

(Also never mind the reference to Werner Sinn in the next line in the original article – although Sinn still had a point in spite of his rather painful analysis)

Unable to make a draft at the central bank, governments are left with less means of protecting themselves in case of failures. Hence nations in a currency union are more directly dependent on the external sector.

Then on Weidmann:

Alas, these remarks confuse productivity with competitiveness. Yet these are distinct: the US, for example, is more productive, but less competitive, than China. External competitiveness is relative. Moreover, at the global level, the adjustment must also be shared. Mr Weidmann knows this. As he says, “of course, surplus countries will eventually be affected as deficit countries adjust”. The question is by what mechanism.

[emphasis: mine]

Martin Wolf knows how economies as a whole work roughly and he has been emphasizing that the solution to the world’s problems lie with the creditor nations. Also, in 2004 he said that America is in a comfortable path to ruin!

So here’s an unsuccessful attempt to prove Martin Wolf doesn’t “get it” from Bill Mitchell: So near but so far … from comprehension. This was a critique of an article written by Martin Wolf where he showed that the creditor status of Japan is hugely helpful to its recovery in spite of having a huge public debt . . . Martin Wolf’s right in spite of Mitchell’s assertion that he is wrong 🙂

In a recent paper, Bradford DeLong and Lawrence Summers suggest that a fiscal expansion can be useful to bring an economy from a depressed state (!). The rough idea being that a relaxation of fiscal policy leads to a higher output and the increase in economic activity leads to a stabilization of public debt/gdp ratio.

This condition is valid as long as (in the authors’ terminology):

(click to enlarge)

The interesting thing about this is that the authors suggest that even if r > g, it is possible for the public debt/gdp to remain sustainable under certain conditions.

I won’t have more to say on this because it uses a standard one-period analysis but the fact that some mainstream authors seem to understand the fiscal policy dynamics better is encouraging.

Arguing that their “… conclusions conflict with those of the “new consensus,” which holds that a correct setting of interest rates is the necessary and sufficient condition for achieving noninflationary growth at full employment, leaving fiscal policy rather in the air.”, they also derive a result for a closed economy:

It is usually asserted that, for the debt dynamics to remain sustainable, the real rate of interest must be lower than the real rate of growth of the economy for a given ratio of primary budget surplus to gdp. If this condition is not fulfilled, the government needs to pursue a discretionary policy that aims to achieve a sufficiently large primary surplus. We can easily demonstrate that there are no such requirements in a fully consistent stock-flow model such as ours.

The G&L style of modeling is extremely useful because it gives great attention to stocks and flows so that no errors creep in. The result is surprising the first time one hears this because it goes against intuition. This can be seen by thinking of the interest payments of the government as income for the domestic private sector!

So no conditions such as r < g!

Open Economy Debt Dynamics

For open economies, G&L are also able to construct select scenarios where a debtor nation can be indebted to the rest of the world without the nation’s debt (which is different from public debt) increasing relative to gdp forever. (Of course by no means proving/implying it for all possible scenarios).

where d is “external debt” and pb is the primary balance of the current account balance. (The expressions are relative to gdp)

Suppose the government and the central bank want to restrict external debt to 50% of gdp – with the view that foreigners may consider moving above it as unsustainable. Assume growth is 3.5% and effective interest rate paid on liabilities to foreigners is 1%. Then the tolerable primary deficit of current account balance is 1.25%. This is calculated by setting the left hand side to zero and just plugging the formulas. (See below)

Please note, a higher growth will worsen the external balance so it is not a good argument that growth can lead to a lower debt/gdp ratio.

To summarize, intuitions for a closed economy and the open economy can appear contradictory.

Standard Analysis

I have seen many economists including Post Keynesians (not G&L) take the above equation and interpret it rather differently. So assuming sustainability, a constant primary balance pb implies the debt sustains at

or simply,

A continuous time formulation leads to an equality sign. The above is derived by assuming the debt sustains at d and shuffling the terms in the first equation.

Note: the above is valid only if there a stabilization. Else, in the case where g < r, the above expression gives a negative answer for a negative primary balance – but that is because the derivation assumed sustainability and cannot be used when debt/gdp keeps rising.

This is also written sometimes as

by expanding the denominator of the previous expression using the Taylor Theorem from Mathematics.

This raises a curiosity – how come in the G&L case for the closed economy did the debt sustain even when g > r? That’s because it was a dynamic stock-flow consistent model as opposed to the artificial assumption of a constant deficit used in standard analysis such as the third equation above.

Nonetheless the above analysis shows that for a constant deficit (though artificial), debt sustains as per the equation (assuming growth and the rate of interest paid are constant as well!)

Back to Open Economies

Moving to the open economy case, where debt and deficit denote the external debt and the current account deficit, the above shows that if the primary deficit is restricted somehow to say 5% of gdp and the differential between growth and interest rate is 2%, the external debt sustains at 250% of gdp.

This should be seen as a restriction. Instead some/many Post Keynesians just state it is sustainable. A higher growth rate will increase the deficit (current account) and the debt-dynamics can make the whole process unsustainable. So one needs to model how fiscal policy itself affects the current account deficit rather than keeping it a constant relative to gdp.

This is the reason many nations find themselves troubled by the external sector.

This can be seen for the case of the United States. A huge relaxation of fiscal policy will bring back the current account deficit to 6% of gdp (and rising) and put the world on an unsustainable path. What the United States needs to do is ask its trading partners to expand domestic demand by fiscal expansion and achieve higher growth so that it itself can achieve a higher growth rate due to the extra space created for fiscal policy.

More generally, we need a concerted action!

For a related analysis see Dean Baker’s recent analysis on the trade deficit being America’s fundamental imbalance: The Iron Grip of Accounting Identities

Summary

There is no condition such as if r <g, debt is sustainable. Debt can keep rising relative to gdp simply because deficit keeps rising.

The condition r > g can be useful in studying certain circumstances for analysis.

My last post was on U.S. net income payments from abroad and how it continues to be in the favour of the United States. The late Wynne Godley had been analyzing this since 1994. In an article titled U.S. Trade Deficits: The Recovery’s Dark Side?, written with William Milberg, he had a section called “Foreign indebtedness and the foreign income paradox” where he said:

So far, the practical consequences of the United States having become “the world’s largest debtor” have not been all that significant… But it would be an error to suppose that, because the net return on net assets has been negligible in the recent past, the same thing will be true in the future…

… Why did the net foreign income flow remain positive for so long after 1988? In order to understand this apparent paradox, it is essential to disaggregate stocks of assets and liabilities and their associated flows, and to distinguish (in particular) between financial assets and direct investments… The reason that net foreign income remained positive for so long can now be understood (at least up to a point) by making a comparison of the flows shown in Figure 3 with the stocks shown in Figure 2. The net inflow that arises from direct investment has been roughly equal to the net outflow on financial assets in recent years, even though the stock of financial liabilities has been about five times as large as the market value of net foreign investments. In other words, the rate of return on net direct investments far exceeded the rate on net financial liabilities

Figure 2 referred to is below:

and Figure 3:

which is what I redrew with updated data in my previous post. But as we saw the net income payments from abroad continues to be positive (!!) even till date but the reason is similar. Foreign direct investment in the United States has risen to $2.8T at the end of 2011 as per Federal Reserve’s Z.1 Flow of Funds while U.S direct investment abroad rose to $4.8T – significantly higher (even as a percent of GDP) than in the mid-90s.

The net direct investment has seen huge returns (both via income and holding gains) and so this killing has brought in good fortunes for the United States. Of course with the whole current account of balance of payments in deficit, the external sector bleeds the circular flow of national income in the United States and contributes to weak demand there.

So a current account deficit is bad for the United States but financing this deficit has been easy for the United States given that the US Dollar is the reserve currency of the world. Why do nations require reserve assets? The late Joseph Gold of the IMF gave a nice description in his book Legal and Institutional Aspects of the International Monetary System: Selected Essays:

click to view on Google Books

What makes the US dollar the reserve currency of the world is difficult to argue. However it cannot be taken for granted that the United States may enjoy this exorbitant privilege given that the Sterling was once the darling of the financial markets and central banks.

Their argument is similar – direct investments have made huge returns for the domestic private sector of the United States and gives a good account of the external sector. Here’s a graph of the United States’ net international investment position using data reported by the Federal Reserve’s Z.1 Flow of Funds Accounts as well as the BEA’s International Investment Position:

Why the difference is a topic for another post. I don’t know it yet. Gourinchas and Rey have some answers. The Federal Reserve’s data is till 2011 end and quarterly (and seasonally adjusted) while BEA data is yearly and available till 2010.

So, from the graph above, the United States became a net debtor of the world around 1986. The indebtedness has been rising mainly due to the huge current account deficits the nation manages to run and is partly offset by “holding gains”.

Here’s a graph of the current account deficit plotted with other “financial balances” (since they are related by an identity)

By the way, the U.S. was a creditor of the world when the Bretton Woods system of fixed exchange rates collapsed. Some authors describe this collapse by saying that money has become fiat since 1971 – whatever that means!

Gourinchas and Rey point out – correctly in my opinion:

The previous discussion points to a possible instability, even in an international monetary system that lacks a formal anchor. The relevant reference here is Triffin’s prescient work on the fundamental instability of the Bretton Woods system (see Triffin 1960). Triffin saw that in a world where the fluctuations in gold supply were dictated by the vagaries of discoveries in South Africa or the destabilizing schemes of Soviet Russia, but in any case unable to grow with world demand for liquidity, the demand for the dollar was bound to eventually exceed the gold reserves of the Federal Reserve. This left the door open for a run on the dollar. Interestingly, the current situation can be seen in a similar light: in a world where the United States can supply the international currency at will and invests it in illiquid assets, it still faces a confidence risk. There could be a run on the dollar not because investors would fear an abandonment of the gold parity, as in the 1970s, but because they would fear a plunge in the dollar exchange rate. In other words, Triffin’s analysis does not have to rely on the gold-dollar parity to be relevant. Gold or not, the specter of the Triffin dilemma may still be haunting us!

Gourinchas and Rey’s arguments depend on estimating a tipping point – the point where the net income payments from abroad turn negative. This of course depends on various assumptions but let us look at it.

The gross assets of the United States held abroad and liabilities to foreigners keep changing as the nation is able to increase its liabilities and use it to make direct investments abroad. The reserve currency status has provided the nation with this privilege as central banks around the world are willing to hold dollar-denominated assets. The positive return (as well as revaluation gains from the depreciation of the dollar – when it depreciates) helps reduce the net indebtedness but the current account deficit contributes to increasing it.

The following is the graph of gross assets and liabilities – using the Federal Reserve’s Z.1 Flow of Funds Accounts data and also BEA’s data for the ratio:

So assuming assets held abroad A make a return rA and liabilities L to foreigners lead to payments at an effective interest rate rL income payments from abroad will turn negative whenever

rA · A − rL · L < 0

So A and L are changing due to the current account deficits and revaluation gains on assets and liabilities. Meanwhile, the effective interest rates are themselves changing in time because of various things such as short term interest rates set by the central banks, market conditions, state of the economy etc. Also, if the private sector of the United States makes more direct investments abroad, this will contribute to increase rA (if successful) and the process can go on with net income payments from abroad staying positive for longer. The tipping point is defined by Gourinchas and Rey as the ratio L/A beyond which the the net income payments turn negative. According to their analysis (based purely on historical data), this is 1.30.

If the net income payments from abroad turns negative, international financial markets and central banks may start suspecting the future of the exorbitant privilege according to the authors. Of course, it may be the case that even if it turns negative, the United States’ creditors don’t mind – this has been the case of Australia. The following is from the page 18 of the Australian Bureau of Statistics release Balance of Payments and International Investment Position, Australia, Dec 2011 and in their terminology – which is the same as the IMF’s – it is called “net primary income”)

(Australia’s Q4 2011 GDP was around A$369bn for comparison) and the above graph is quarterly.

So, to conclude the process can continue as long as foreigners do not mind. It shouldn’t be forgotten however that Australian banks had funding issues during the financial crisis and the RBA used its line of credit at the Federal Reserve via fx swaps to prevent a run on Australian banks and it is difficult to design policy without keeping in mind the possibility of walking into uncharted territory.

Once net primary income turns negative, the process can quickly run into unsustainable territory due to the magic of compounding of interest unless the currency depreciates in the favour of the nation helping exports. Else demand has to be curtailed to prevent an explosion but this hurts employment. Other policy options include promotion of exports and asking trading partners to increase domestic demand by fiscal expansion.

The world economy has grown over the last so many years with the United States acting as the importer of the last resort. However, the U.S. current account deficit acts to bleed the circular flow of national income and weakens demand in the States. The nation still grew because of a huge lending boom.

Today, the U.S. Bureau of Economic Analysis came out with the Q4 report on the U.S. International Transactions. According to the release,

The U.S. current-account deficit—the combined balances on trade in goods and services, income, and net unilateral current transfers—increased to $124.1 billion (preliminary) in the fourth quarter of 2011, from $107.6 billion (revised) in the third quarter. Most of the increase in the current account deficit was due to a decrease in the surplus on income and an increase in the deficit on goods and services.

So the current account balance also consists of “income payments from abroad” – a bit of wrong phrasing because all items are income/expenditure flows. The net income payments from abroad continues to surprise analysts because in spite of the net indebtedness position of the United States, this continues to be positive and in recent times has increased! (although it fell the last quarter). Many hold the belief that the United States has lower interest rates and this is the consequence of that. While it is true that interest rates outside the U.S. are in general higher, and there is some truth to the above argument, it gives one the wrong impression that it will always be the case that net income from abroad will always be positive.

The following graph shows that this intuition is misleading. Most of the contribution to the net income is due to direct investments abroad which has made a killing for the private sector and the reverse – direct investment receipts for foreigners has made next to nothing. The remaining – income from financial assets held abroad less interest/dividend paid to foreigners’ holding of U.S. financial assets is already negative!

The red line has reduced in recent times due to lower interest rates in the U.S. presumably. But the more the U.S. continues to run large current account deficits, the deeper the red line will grow – pulling the black line to zero and into the negative territory.

The net income payments from abroad is more a result of the huge killing the U.S. domestic private sector has made abroad than because of lower interest rates. For example, excluding FDI, the data from BEA suggests that the “effective interest rate” on U.S. liabilities was 1.42% in 2010, while that on U.S assets held abroad is 1.65%. This differential will not be sufficient to keep the income payments to foreigners bounded. I used the 2010 data because the International Investment Position is available only till 2010 and the one for end of 2011 will be released only mid-2012.

To understand this, consider the case when the U.S net indebtedness grows to something about 100% of GDP due to the continuous current account deficits – if market forces allow the whole process to go on(!). This is an involved analysis involving some growth assumptions and the fiscal stance in the U.S. and the rest of the world. For example, people frequently forget that a higher growth in the U.S. will also bring in higher current account deficits. But it can easily be shown that the red and the black lines above grow into a negative territory if the United States wants to quickly achieve full employment by fiscal policy alone.

Of course the above graph shows that there is a lot fiscal expansion can achieve in the medium term for the United States.

These numbers look “small” and can lead one into believing that “all is well”. And this is another mistaken view. For example if there is a drastic relaxation of fiscal policy by the U.S. government, the current account deficit will soon hit 6-8% of GDP which may require further relaxation of fiscal expansion to compensate the leakage of demand due to the current account deficit and with income payments turning negative due to higher indebtedness, this will turn into an unsustainable path because the current account deficits and net indebtedness will keep increasing relative to GDP. This will need interest rate hikes to attract foreigners but turns the whole process unsustainable unless one believes in the foreign exchange market doing the trick. Also currently the interest rates are low because the Federal Reserve has kept them artificially low and foreigners do not mind holding U.S. dollar assets at this rate. As William Dudley says interest rates will be raised at some point by the Federal Reserve and this will increase payments to foreigners. See this post William Dudley On U.S. Sectoral Balances

Of course, this is not the only scenario and there’s a lot fiscal policy can achieve in the medium term but it is important to keep in mind that something needs to be done with the external sector to bring the external sector in balance to achieve full employment.

This is the first part of a series of posts I intend to write on the “rest of the world” accounts in National Accounts. This blog is about looking at economies from the point of view of National Accounts, Cambridge Keynesianism and Horizontalism. While various descriptions of balance of payments exist, most of them simply end up making money exogeneity assumption somewhere in the description!

In my view a careful description of balance of payments offers great insights on how economies work and what money really is. It is impossible to understand the success and failures of nations without understanding the external sector.

A description in terms of stocks and flows is the most appropriate for macroeconomics. Fortunately, national accountants have a good systematic approach to this.

Consider the following transaction: a government (or a corporation) raises funds in the international markets. The buyers can be residents as well as non-residents. The currency of the new issuance can be domestic as well as foreign. Does this by itself increase the net indebtedness of the nation as a whole?

The answer is No, and can be a bit surprising to the reader because the answer is the same whether the currency is domestic or foreign. The trick in the question is that an issuance of debt increases the assets and liabilities of the issuer!

(Note: the question was about the transaction, not on what happens after this)

Gross assets and liabilities vis-à-vis the rest of the world can be a bit more complicated and we need a more systematic analysis.

Consider another transaction. A government is redeeming a 7% bond with a notional of 1bn with semi-annual coupons. How much does the net indebtedness of the country change? Assuming that all the lenders are in the rest of the world sector, the net indebtedness changes by 35m. Does not matter if the currency is domestic or not. Why 35m? Because the semi-annual coupon has to be paid on redemption and the coupons are interest payments and this is recorded in the current account and this increases the net indebtedness. The principal payment cancels out the earlier liability – the bonds.

So between the start and the end of the period, foreigners earned 35m and this increased the net indebtedness of the nation who paid the interest. Of course there are other transactions which can cancel this out.

In another scenario, if all the bond holders were residents, the net indebtedness does not change – whether the bonds were in domestic currency or not.

The above was about financing. What about imports and exports? Exports provide income to a nation or a region as a whole and imports are opposite. If a nation is a net importer (more appropriately running a current account deficit), this means its expenditure is higher than income. When expenditure is higher than income, this has to be financed and this is via net borrowing.

There is one important point worth stressing. Many people – including many economists (most?) – treat liabilities to foreigners in domestic currency as not really a liability at all – at least the government’s liabilities. The reason provided is that while usually the government is forbidden from making an overdraft at the central bank or have limited powers in using central bank credit, it can end up making a higher use of it than the limits allowed – in extreme conditions. This in my opinion, is a silly intuition.

While it is true that the governments of most nations (with exceptions such as the Euro Area governments) can make a draft at the central bank and this offers the government protection to tide over extreme emergencies, the government has to directly or indirectly finance the current account deficits and this can prove unsustainable. Despite this there is an advantage in having indebtedness to foreigners in the domestic currency because:

An indebtedness to foreigners in domestic currency prevents revaluation losses on the debt if foreigners continue holding the debt and if the currency depreciates against foreign currencies. If the debt is denominated in a foreign currency and if it depreciates, more income needs to be earned from abroad to service the principal and interest payments.

The discussion can be confusing because of the relative ease with which the United States has managed till now to finance its current account deficits because the US dollar is the reserve currency of the world and continues to do so and the holders are willing to accept liabilities of resident sectors of the United States, especially the government’s at low interest rates/yields.

James Tobin, who has provided the best description of the meaning of government deficits and debt said this in an article “Agenda For International Coordination Of Macroeconomic Policies” (Google Books link)

Nonzero current accounts must be financed by equivalent capital movements, in part induced by appropriate structure of interest rates.

We will discuss this further in many posts and for now here’s a good illustration of how the balance of payments accounts are kept. This is from the Australian Bureau of Statistics’ manualBalance of Payments and International Investment Position, Australia, Concepts, Sources and Methods, 1998

(click to enlarge)

So, one starts out with the international investment position and records the transactions in the current account and the financial account. The difference is that the former records income/expenditure flows while the latter records financing flows. The current account includes items such as imports, exports, dividends, interest payments paid to/received from non-residents etc., while the capital account records transactions such as residents’ purchases of assets abroad, increase in liabilities to non-residents and so on. Since debits and credits equal, the balances in the two accounts cancel out. To calculate the international investment position, we add the financial account flows and calculate revaluations to reach the end of period international investment position.

The international investment position records assets and liabilities vis-à-vis the rest of the world. If the difference – the NIIP – is negative, it means the nation is a debtor nation. In the construction above, all transactions between residents and non-residents are recorded – whether in domestic or foreign currency. The numbers are then converted to the domestic currency according to the best rules prescribed by national accountants.

We will look into these in more detail – including all causalities of course – in later posts in this series. Till then, the summary is: imports are purchased on credit.