The Flow of Funds Accounts provides one of the best snapshot of an economy. In an article appropriately titled ‘No one saw this coming’ – or did they? (see the full paper here), Dirk Bezemer correctly recognizes that the Economics profession’s ignorance of Flow of Funds had a big role to play in its inability to see a crisis coming. Bezemer says

We economists – and the policymakers who rely on us – ignore balance sheets and the flow of funds at our peril.

Of course, as Bezemer points out, there were exceptions. Post Keynesians were always aware of the flow of funds because monetary economy is a natural starting point in their theory. Wynne Godley and Marc Lavoie wrote a book (my favourite!) Monetary Economics: An Integrated Approach To Credit, Money, Income, Production and Wealth, Palgrave Macmillan, 2007, to unify Post Keynesian theory and the flow of funds approach, perhaps improving the presentation of the latter using something called the “transactions flow matrix”.

In my opinion, nobody even came close to Wynne Godley in not only predicting the crisis but the warning about the difficulties in resolving it.

One notable highlight of today’s Z.1 release was that

Household net worth—the difference between the value of assets and liabilities—was $57.4 trillion at the end of the third quarter, about $2.4 trillion less than at the end of the previous quarter.

A lot of readers will know about sectoral balances. How do we get that from Z.1? Table F.8 gives “Net Lending” of each sector of the economy. The difference in a sector’s income and expenditure is it’s “Net Lending”.

(click to expand, and click again to expand)

Before the crisis, the private sector had its income lower than expenditure and was financing the difference by borrowing from the other sectors. As the crisis hit, private sector expenditure retrenched – so you can see how the private sector has become a net lender from being a net borrower before the crisis. Because of this, the government’s borrowing increased from (line 49) $408.1bn in 2007 to $1,471.7bn in Q3 2011 (annualized). It was also due to a relaxation of fiscal policy during the crisis, in order to stimulate demand. The expenditure of the United States as a whole is higher than its income, and the difference is the current account deficit. This is financed by net borrowing from foreigners (line 42) – which was $446.7bn in Q3 2011 (annualized). This deficit was $715.9bn in 2007, bleeding demand at a massive scale from the US economy.

There are two more tables I see closely. The first is the net income payments from the rest of the world, which surprisingly remains positive, leading to a lot of literature about “dark matter”. (More on that some other time). This, according to the Z.1 is the “net receipts from foreigners of interest, corporate profits, and employee compensation”.

The Levy Institute has been tracking this since 1994. Here’s a latest graph (from their March 2011 analysis)

There are discrepancies between BEA and Fed data. The other table which I rush to check, whenever the flow of funds data is released is the United States’ net indebtedness to the rest of the world – L.107:

which at the end of Q3 was $3,616bn, or 24% of GDP.

There’s a new table – L.108, Financial Business – which actually appeared first time in the previous release (Q2). This sector had $64,299bn in assets and $60,457bn of liabilities at the end of Q3!

Of course, I look at all the tables at some time or the other. Highly recommended.

Marc Lavoie forwarded me the European Central Bank’s Monthly Bulletin, October 2011 which has a section on TARGET2 and the European monetary system. I have had good discussions with him on emails to nail the TARGET2 operations so it is good to see the conclusions being verified in publications. I am waiting to write a long blog post on TARGET2 and trying to collect sources I can quote/link and I came across a section on flow of funds in the same article. It appears on page 99 (page 100 of the pdf) and is titled The Financial Crisis In The Light Of Euro Area Accounts: A Flow-Of-Funds Perspective.

The article has this chart which will be very familiar to readers because it has been in the Levy Institute’s Strategic Prospects since many years.

There are some differences in terminologies. Wynne Godley (and Francis Cripps) started using NAFA (Net Accumulation/Acquisition of Financial Assets) to denote a sector’s surplus in the 1970s and Levy Institute has continued using this. Modern national accountants use Net Lending (by a sector) and split this into Net Acquisition of Financial Assets and Net Incurrence/Acquisition/Increase of/of/in Liabilities and take the difference. Levy’s authors also use Net Lending but as Net Lending to a Sector – e.g., Net Lending to Households.

The article also presents this table (termed Transactions Flow Matrix by Wynne Godley – his greatest trick)

(click to enlarge)

and has this description:

The sectoral accounts present the accounts of institutional sectors in a coherent and integrated way, linking – similar to the way in which profit and loss, cash flows and balance sheet statements are linked in business accounting – uses/expenditure, resources/revenue, financial flows and their accumulation into balance sheets from one period to the next.To this effect, all units in the economy are classified in one of the four institutional sectors (i.e. households, non-financial corporations, financial corporations and general government). Their accounts are presented using identical classifications and accounting rules (those of ESA 95), in a manner such that each transaction/asset reported by one unit will be symmetrically reported by the counterpart unit (at least in principle). Accordingly, the sectoral accounts present the data with three constraints: each sector must be in balance vertically (e.g. the excess of expenditure on revenue must be equal to financing); all sectors must add up horizontally (e.g. all wages paid by sectors must be earned by households); and transactions in assets/liabilities plus holding gains/losses and other changes in the volume of assets/liabilities must be consistent with changes in balance sheets (stock-flow consistency). The sectoral accounts are commonly presented in a matrix form, with sectors in columns and transactions/instruments in rows, with horizontal and vertical totals adding up (see the example in the table).

The first five rows of the table show the expenditure and revenues of each of the sectors (broken down into types of expenditure/revenue). In row 6, the difference between revenue and expenditure (the surplus/deficit) is shown.

The notions of revenue and expenditure are close to, but generally less encompassing than, the more traditional national account concepts of resources and uses. Income can then be defined as revenue (except capital transfers received) minus expenditure other than final consumption and capital expenditure (capital formation and capital transfers paid). For corporations, income corresponds to retained earnings. Savings is the excess of income over final consumption.

Surpluses/deficits are then associated with transactions in financial assets and liabilities in each sector. This is shown in rows 7 to 10. The bottom part of the table shows the stocks of assets and liabilities, which result from the accumulation of transactions and other flows. This table is extremely simplified (e.g. omitting an explicit presentation of the stock of non-financial assets).

The excess of revenue over expenditure is the net lending/net borrowing (i.e. financial surplus/ deficit), a key indicator of the sectoral accounts. Typically, a household’s revenue will exceed its expenditure. Households are thus providers of net lending to the rest of the economy. Non-financial corporations typically do not cover their expenditure by revenue, as they finance at least part of their non-financial investments by funds from other sectors in addition to internal funds. Non-financial corporations are thus typically net borrowers. Governments are also often net borrowers. If the net lending provided by households is not sufficient to cover the net borrowing of the other sectors, the economy as a whole has a net borrowing position vis-à-vis the rest of the world. Deviations from this typical constellation were apparent in several euro area countries before the crisis, in particular, with extremely elevated residential investment that resulted in households becoming net borrowers (as has been the case in the United States).

The adding-up constraints in the accounts require that any (ex ante) increase in the financial balance of one sector is matched by a reduction in the financial balances of other sectors. The accounting framework does not, however, indicate by which mechanism this reduction will be brought about, or which mechanisms are at play. The EAA makes it possible to track changes in net lending in the different sectors of the economy. It also specifies the financial instruments affected and shows how the transactions and valuation changes leave a lasting effect on the balance sheets of the sectors.

The article is worth a read.

The Bank of England also had a similar article recently but before: Growing Fragilities – Balance Sheets In The Great Moderation by Richard Barwell and Oliver Burrows and quotes the work of G&L (Godley and Lavoie). It also has a similar matrix as the ECB’s article.

(click to enlarge)

Godley and Lavoie build a series of closed accounting frameworks based on the system of National Accounts, which encompass: the standard national income flows, such as wages and consumption; the counterpart financing flows, such as bank loans and deposits; and stocks of physical and financial assets and liabilities. This framework lends itself to representation in a set of matrices. The first matrix captures flow variables (Table A.1). The columns represent the sectors of the economy and the rows represent the markets in which they interact. The matrix has two important properties. Each sector’s resources and uses columns provide their budget constraint — the sums must equal to ensure that all funds they receive are accounted for. And each row must also sum to zero, to ensure that each market clears — that is, the supply of a particular asset must be matched by purchases of that asset, to ensure that no funds go astray.

The table can usefully be split in two, with the top half covering the standard income and expenditure flows and the bottom half covering financing flows. The two halves of the table are linked together by each sector’s ‘net lending balance’, or ‘financial surplus’. The net lending balance can be used to summarise each sector’s income and expenditure flows as the difference between the amount the sector spends on consumption and physical investment and the amount that it receives in income. This difference must be met by financing flows — either borrowing or the sale of financial assets. In national accounts terminology, a sector’s net lending balance (NL) must equal its net acquisition of financial assets (NAFA) less its net acquisition of liabilities (NAFL). Across sectors, the net lending balances have to sum to zero, as all funds borrowed by one sector must ultimately come from another.

While it is useful to split the table for accounting purposes into income and expenditure flows and financing flows, it is important to note that the acquisition of financial assets and liabilities is not necessarily determined purely by imbalances between income and desired expenditure. Sectoral balance sheets can adjust for other reasons. Agents may want to borrow money to purchase assets, simultaneously acquiring financial assets and liabilities. And on occasion agents may want to shrink the size of their balance sheets, selling off financial assets to pay off financial liabilities. Finally, some agents may default on their debt obligations, which will involve a revision in the financial assets and liabilities of both debtor and creditor. At an aggregate level, simultaneous expansion of a sector’s assets and liabilities invariably represents one set of underlying agents taking on assets whilst the other takes on liabilities. The household sector provides an important example. If a young household takes a mortgage to buy a house from an old household, the sector in aggregate simultaneously acquires a liability (the young household’s mortgage) and an asset (the deposit created for the young household to pay to the old household).

All of these activities — leveraging up, deleveraging and default — involve NAFA and NAFL moving in lockstep. The net lending identity still holds: the gap between income and expenditure determines the difference between NAFA and NAFL. But the absolute size of the NAFA and NAFL flows is determined by agents’ actions in financial markets. The second table captures the balance sheet positions of each sector. The balance sheet matrix is updated over time using data on the acquisition of assets and liabilities from the transaction flows matrix, and revaluation effects to asset positions. Proceeding in this manner, balance sheets always balance across sectors, flows of funds are always accounted for over time and the impact of flows of funds on balance sheets is always recorded.

Again, good article!

The first time a proper transactions flow matrix appeared was in a 1996 Levy institute paper by Wynne Godley: Money, Finance And National Income Determination – An Integrated Approach.

It is frequently asserted by some economists and even some Post-Keynesians that as long as the effective interest rate paid on stocks of debt is less than the growth rate, stock-flow-norms do not keep rising forever. That is, ratios such as public debt/gdp, external debt/gdp do not rise forever at full employment if this condition is maintained, implying thereby that fiscal policy can be used to achieve a higher output and there is nothing one needs to do about the external sector.

It is the purpose of this post to clear such misconceptions.

Fiscal Policy

What can fiscal policy achieve and what are its limitations? In an essay from the centenary conference of 1983, Wynne Godley wrote [1]:

How did Keynes think the economy worked? Any time between 1950 and 1970 1 would have confidently attributed to Keynes, as preeminently important, the following views about economic policy:

(a) Real demand, output and employment are determined via a multiplier process by the fiscal and monetary operations or the government and by foreign trade performance.

(b) Inflation, though influenced by the pressure of demand, is largely indeterminate in terms or economic variables and therefore, if it is to be controlled, requires some kind of direct political intervention.

(c) Fiscal and monetary policies in any one country are potentially subject to important external constraints.

While there is reasonable support for these views about economic policy in Keynes’s writings, there is no warrant for them at all in the General Theory. Indeed it is strange, seeing how commonly the view is attributed to Keynes that fiscal policy is crucial to real output determination, that the General Theory is concerned with an economy in which neither a government nor for that matter a foreign sector exist at all.

Notwithstanding this I still think, not only that the propositions can be correctly attributed to Keynes, but that they are, themselves, essentially correct. I have however been forced to the conclusion that Keynes was a long way from achieving a coherent theoretical basis for maintaining them, and largely for this reason, his ideas have proved very vulnerable to the attacks from many different directions to which they have been subjected, particularly in the last fifteen years.

To points (a), (b) & (c) above, let me add

(a(i)) Higher output is also possible when the private sector expenditure is higher than private sector income.

This was highlighted by Godley himself in the late 90s, when the US economy expanded in spite of a tight fiscal stance and he was the first to write that this process is unsustainable!

Debt Convergence Analysis

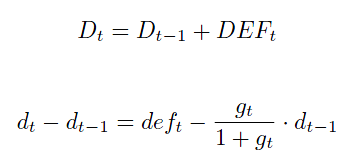

Let us now turn to the question on convergence/divergence of stock-flow norms. In what follows, I simply use debt to denote the public debt or the external debt. Assuming away complications arising from revaluations, we have the identities [2]

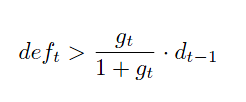

Uppercase is for stock of debts, and lower case for debt-to-gdp ratio and g is the growth rate. Note: DEF is primary deficit and excludes interest payments. We will turn to complications added by interest payments soon. Whenever

the stock of debt keeps rising.

Note, when the debt-to-gdp ratio is less than 1 (100%), the sustainability condition is strong on the deficit. The condition DEF < g is at at a debt-to-gdp ratio is 1. Beyond 100%, the condition on the deficit is a bit weaker than DEF < g because the deficit can be between g and g·d.

This argument is sometimes presented differently by some Post Keynesians by including the effective interest rate r. The equation looks like the following when it is included:

It is argued that the third term on the right hand side can be set to be greater than the second term (which is to say that r < g is sufficient to ensure sustainability).

This argument (r < g guaranteeing problems are solved) has no substance. This is because rearranging the terms in the way done above, shows more clearly that the stock-flow ratio rises faster than the case where the analysis was done without the interest rate term!

There is one more complication. It may be argued that growth can only bring down the deficit (the deficit here being the public sector deficit). This is true for the case of a closed economy. The convergence of the public debt-to-gdp ratio is also achieved in the case of a closed economy because interest payments by the government is income for the private sector and they will consume it (although the capitalist class’s propensity to consume is less than that of the worker class). Higher consumption leads to higher national income and hence higher taxes, bringing down the deficit.

Wynne Godley and Marc Lavoie [3] showed how this happens precisely in the case of a closed economy:

This paper deploys a simple stock-flow consistent (SFC) model in order to examine various contentions regarding fiscal and monetary policy. It follows from the model that if the fiscal stance is not set in the appropriate fashion—that is, at a well-defined level and growth rate—then full employment and low inflation will not be achieved in a sustainable way. We also show that fiscal policy on its own could achieve both full employment and a target rate of inflation. Finally, we arrive at two unconventional conclusions: (1) that an economy (described within an SFC framework) with a real rate of interest net of taxes that exceeds the real growth rate will not generate explosive interest flows, even when the government is not targeting primary surpluses, and (2) that it cannot be assumed that a debtor country requires a trade surplus if interest payments on debt are not to explode.

Also, they create some very special scenarios, where the external debt stays sustainable.

However, making the above work is difficult for the case of an open economy in general. This was what the essential argument of the New Cambridge School.

So is there a way to achieve convergence of the stock-flow norm? To achieve that, the external sector deficit (more precisely, the primary balance in the current balance of payments) should be less than the growth rate times the external debt. This creates tensions for demand-management because if the external deficit grows higher than the growth rate, it is usually brought back to a sustainable path by deflating demand. This is because the balance of payments deficit itself will grow if growth is high! (unless exports improve).

There are of course some scenarios which can lead to the convergence of the external debt (if the markets allow it). A more careful treatment will always lead one to studying income and price elasticities of imports, growth in the rest of the world etc.

Other scenarios which could lead to the improvement of the external sector are: promotion of exports leading to more success abroad and luck – market forces miraculously achieving the required depreciation to improve the external sector. Since the latter is mere wishful thinking, we see nations trying to depreciate their currencies because it makes their exports more competitive.

To bring the balance of payments deficit back into balance, there is also the option of restricting imports but in the world of “free trade”, it can create tensions between nations.

There are two more options. The first is to ask your trading partners to appreciate their currencies if they have pegged them but this has to go through negotiations because they want you to do the same! The second (which includes the previous option) is what this blog is about. Since, the external sector creates problems for demand management, one can only think of coordinated efforts by institutions running the world economy, working to achieve higher world demand instead of contracting it.

References

Wynne Godley, Keynes And The Management Of Real Income And Expenditure, p135, Keynes And The Modern World: Proceedings Of The Keynes Centenary Conference, ed. David Worswick and James Trevithick, Cambridge University Press, 1983.

Wynne Godley and Marc Lavoie, Fiscal Policy In A Stock-Flow Consistent Model, p 79, Journal of Post Keynesian Economics / Fall 2007, Vol. 30, No. 1. Draft version available at http://www.levyinstitute.org/publications/?docid=911

Horizontalism, Endogenous Money and ideas such as that were brought into Macroeconomics by Nicholas Kaldor. In [1] he wrote

Diagrammatically, the difference in the presentation of the supply and demand for money, is that in the original version, (with M exogenous) the supply of money is represented by a vertical line, in the new version by a horizontal line, or a set of horizontal lines, representing different stances of monetary policy.

Loans Make Deposits. Deposits Make Reserves

In 1985, Marc Lavoie [2] coined the phrase Loans Make Deposits and Deposits Make Reserves. In the article Credit And Money: Overdraft Economies, And Post-Keynesian Economics, he says:

Orthodox monetary economics is founded on the double entry hypothesis of free reserves and the credit multiplier Each individual bank may only increase its loans to the public when depositors increase their balances there, i.e., when free cash reserves augment for that one bank. In the aggregate, commercial banks are allowed to make supplementary loans when they dispose of free reserves. The latter can be obtained through modifications of the behaviour of the public, as a result of a surplus in the foreign account, as a consequence of the intervention of the central bank on the open market, or following a change in the reserve requirements. Although the credit multiplier functions on the basis of an expansion of credit, deposits make loans in the orthodox context. The usual sequence of events is as follows: the central bank buys some security from a member of the public; the deposits of this person are increased; the bank which benefits from these increased deposits now disposes of excess reserves and can make new loans …

… The credit-money view rejects this approach to money and inflation by reversing the sequence of events. According to the unorthodox view, loans make deposits. Banks do not wait for the appropriate amount of liquid resources to exists to provide new loans to the public (mainly firms). Credits are created ex nihilo. The recipient of the purchasing power is the initial recipient of the loan. When the bank makes a new loan, the borrower is being immediately credited with a deposit, the amount of which is exactly equal to the amount of the loan. Hence, the increase in the supply of money is a consequence of increased loan expenditure, not a cause of it. The loan is the causal factor …

… Once commercial banks have created credit money, how do they get hold of the reserves required by the newly created deposits or how do they obtain the currency cash requested by the public? In many European banking systems, France in particular, commercial banks simply borrow their requirements in high-powered money. Most banks are permanently indebted to the central bank. The money market in those circumstances does not play a fundamental role. When banks, overall, are in need of more high-powered money, they increase their borrowings with the central bank at the discount rate set by the latter. Legal reserve ratios, when they do exist, are not used to control the created quantity of money. They exist to increase the cost of the loans granted by the banks since reserves carry no interest revenue …

… It is often claimed that the North American and German banking systems function in quite a different way. This however is an illusion. Although institutional arrangements are quite dissimilar, the expansionary process of credit is the same… First… banks grant legally binding lines of credit which imply future access to reserves. Second, North American banks must respond to lagged required reserve-accounting conventions. Third, banks always have access, although limited, to the discount window of the central bank.

References

Nicholas Kaldor, Keynesian Economics After Fifty Years, p22, Keynes And The Modern World, ed. George David Norman Worswick and James Anthony Trevithick, Cambridge University Press, 1983.

Marc Lavoie, Credit And Money: Overdraft Economies, And Post-Keynesian Economics, pp 67-69, Money And Macro Policy, ed. Marc Jarsulic, 1985. (Available at UMKC’s course site)

The central message of this book is that members of the economics profession, all the way from professors to students, are currently operating with a basically incorrect paradigm of the way modern banking systems operate and of the causal connection between wages, prices, on the one hand, and monetary developments, on the other. Currently, the standard paradigm, especially among economists in the United States, treats the central bank as determining the money base and thence the money stock. The growth of the money supply is held to be the main force determining the rate of growth of money income, wages, and prices.

… This book argues that the above order of causation should be reversed. Changes in wages and employment largely determine the demand for bank loans, which in turn determine the rate of growth of the money stock. Central banks have no alternative but to accept this course of events, their only option being to vary the short-term rate of interest at which they supply liquidity to the banking system on demand. Commercial banks are now in a position to supply whatever volume of credit to the economy their borrowers demand.

– Basil Moore, Horizontalists and Verticalists, 1988 [1]

Most economics books come nowhere close to starting like this. To be fair, when Moore wrote the book, many Post-Keynesians thought that this picture is too simplified. Only a few – such as Marc Lavoie – supported Moore’s view. He himself had been writing about the Post-Keynesian theory of money for some years, around that time. The supposed simplicity gave rise to the long debate Horizontalism versus Structuralism. There’s a lot of nice literature on this and its worth a read.

What do the terms horizontal and vertical refer to? Economists make supply-demand diagrams in which price is on the y-axis and quantity is on the x-axis. Moore called neoclassical economists Verticalists because according to them, the “money supply” is vertical in the diagram. “Money demand” is downward sloping. The interest rate at which the supply and demand curves meet is the market interest rate. Horizontalists, strongly believe that this is exactly wrong and the supply curve is horizontal at the rate determined by the central bank. The quantity of money, then, is the point at which the non-banking sector’s desire to hold money balances (as opposed to “demand”) determines the money stock (as opposed to “supply”). Of course, as explained by Louis-Philippe Rochon and Matias Vernengo [2], the idea of making supply-demand diagrams is only a second-best tool, the more important point being that money is endogenous.

Recommend Moore’s book. I had previewed the book at amazon.com but had to search the whole internet to get it. I tried a Greek and a French seller and ordered online, only to be told later I should expect a refund since that the book is out of stock and wrongly mentioned on the website as available. I finally found a seller at Amazon France selling a used copy for €175.38 but would deliver only to a few countries. I had to get it shipped to a friend in the US and ask him to ship it to me, which cost me an extra $94.

References

Basil Moore, Horizontalists and Verticalists, The Macroeconomics Of Credit Money, Cambridge University Press, 1988.

Louis-Philippe Rochon and Matias Vernengo, Introduction, p2, Credit, Interest Rates And The Open Economy: Essays On Horizontalism, ed. Louis-Philippe Rochon and Matias Vernengo, Edward Elgar Publishing, 2001.

Update: 4 Jan 2012: Fixed some errors in the quote.

(click to expand, and click again to expand)

(click to expand, and click again to expand)

which at the end of Q3 was $3,616bn, or 24% of GDP.

which at the end of Q3 was $3,616bn, or 24% of GDP.