But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task, if in tempestuous seasons they can only tell us, that when the storm is long past, the ocean is flat again.

– John Maynard Keynes, A Tract on Monetary Reform (1923), Ch. 3, p. 80.

As you might know, the Indian government cancelled the legal tender nature of majority of bank notes in circulation, earlier this month and asked Indians to deposit them at banks or exchange them for new. The aim according to the government was to curb counterfeiting and what’s called black money here. This is damaging as a large amount of transaction is in bank notes and the implementation has been a failure. People have been standing in queues for the whole day and some even reach banks at 2 am to get a good position in the queue. For many, standing in queues means that the day’s labour is lost. For others, there are delays in wage payments since their employers have problems getting hold of new bank notes. More than 50 people have died. Even 11 bank managers have died due to stress and work overload.

Despite this we keep hearing from the government and the ruling political party’s defenders that the benefits will be long term.

The previous Indian Prime Minister (who was the nation’s leader during mid 2004-mid 2014), Manmohan Singh gave a scathing speech in the Indian Parliament yesterday in which he quotes Keynes on the long run. Manmohan Singh was a student at Cambridge and his heroes are Nicholas Kaldor and Joan Robinson and presumably John Maynard Keynes as well. In this era where politicians are promoting neoliberal ideas, it’s good to see the master being quoted in a Parliament.

The seven-minute video is linked below.

click the picture to see the video on YouTube.

This question about the long-term reminds me of super-hysteresis which was referred by Marc Lavoie recently in an article for INET. It’s closely related to the Kaldor-Verdoorn law in which demand affects supply. The damage done to the demand side because of slowdown in production caused by the Indian government’s poor implementation of its decision to replace majority of bank notes by value affects the supply side as well. Almost nobody who talks about the long-term benefits talks about this issue.

Trade has always been a subject close to non-orthodox economics. Post-Keynesians emphasize the principle of circular and cumulative causation, which in the words of Nicholas Kaldor means, “success creates further success and failure begets more failure”. The importance of trade for the prospects of the US economy was emphasized the most by Wynne Godley in his series of papers for the Levy Institute from the mid-90s to late 2000s. In his paperSeven Unsustainable Processes, Godley said,

The logic of this analysis is that, over the coming five to ten years, it will be necessary not only to bring about a substantial relaxation in the fiscal stance but also to ensure, by one means or another, that there is a structural improvement in the United States’s balance of payments. It is not legitimate to assume that the external deficit will at some stage automatically correct itself; too many countries in the past have found themselves trapped by exploding overseas indebtedness that had eventually to be corrected by force majeure for this to be tenable.

There are, in principle, four ways in which the net export demand can be increased: (1) by depreciating the currency, (2) by deflating the economy to the point at which imports are reduced to the level of exports, (3) by getting other countries to expand their economies by fiscal or other means, and (4) by adopting “Article 12 control” of imports, so called after Article 12 of the GATT (General Agreement on Tariffs and Trade), which was creatively adjusted when the World Trade Organization came into existence specifically to allow nondiscriminatory import controls to protect a country’s foreign exchange reserves. This list of remedies for the external deficit does not include protection as commonly understood, namely, the selective use of tariffs or other discriminatory measures to assist particular industries and firms that are suffering from relative decline. This kind of protectionism is not included because, apart from other fundamental objections, it would not do the trick. Of the four alternatives, we rule out the second–progressive deflation and resulting high unemployment–on moral grounds. Serious difficulties attend the adoption of any of the remaining three remedies, but none of them can be ruled out categorically.

In his 2008 paper, Prospects For The United States And The Rest Of The World: A Crisis That Conventional Remedies Cannot Resolve, he said:

At the moment, the recovery plans under consideration by the United States and many other countries seem to be concentrated on the possibility of using expansionary fiscal and monetary policies.

But, however well coordinated, this approach will not be sufficient.

What must come to pass, perhaps obviously, is a worldwide recovery of output, combined with sustainable balances in international trade. Since this series of reports began in 1999, we have emphasized that, in the United States, sustained growth with full employment would eventually require both fiscal expansion and a rapid acceleration in net export demand. Part of the needed fiscal stimulus has already occurred, and much more (it seems) is immediately in prospect. But the U.S. balance of payments languishes, and a substantial and spontaneous recovery is now highly unlikely in view of the developing severe downturn in world trade and output. Nine years ago, it seemed possible that a dollar devaluation of 25 percent would do the trick. But a significantly larger adjustment is needed now. By our reckoning (which is put forward with great diffidence), if the United States were to attempt to restore full employment by fiscal and monetary means alone, the balance of payments deficit would rise over the next, say, three to four years, to 6 percent of GDP or more—that is, to a level that could not possibly be sustained for a long period, let alone indefinitely. Yet, for trade to begin expanding sufficiently would require exports to grow faster than we are at present expecting, implying that in three to four years the level of exports would be 25 percent higher than it would have been with no adjustments.

It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

So there was a voice for the Post-Keynesian community talking about US trade.

Dean Baker has an article saying the TPP gave us Trump and I agree. Although Donald Trump is a disaster socially, he is less dogmatic about trade and has promised to put tariffs on China (and has even promised fiscal expansion!). Since the Democrats (except Bernie Sanders) didn’t say anything about it and guarded orthodoxies, I believe this was decisive for Trump’s victory.

For the sake of quotes, here’s fromThe New York Times, July 31, 2016:

Mr. Trump himself said in a telephone interview last week that he believed more borrowing and spending would help lift economic growth, a departure from traditional Republican economics.

“It’s called priming the pump,” Mr. Trump said. “Sometimes you have to do that a little bit to get things going. We have no choice — otherwise, we are going to die on the vine.”

He added: “The economy would be crushed under Hillary. But no matter who it is, the debt is going up.”

Here’s a fun video of Donald Trump saying China in loop

click the picture to see the video on YouTube.

Since today morning the BBC has been saying how immoral Trump’s policies are: that fiscal expansion invariably burdens future generations and that thinking of the Chinese government using unfair trade policies is orthodoxy.

That’s not all, Paul Krugman even claimed that equity prices aren’t going to ever rise to pre-Trump level, a position which he flipped within hours after financial markets recovered.

So it’s not difficult to conclude that purely for the sake of defending one’s favourite party or ideology, people are going to make the case against fiscal policy and for free trade. We might hear a lot of pre-Keynesian orthodoxies from smart people more and more. I won’t even be surprised if Paul Krugman becomes a fiscal hawk again.

This has already been the case in discussions around wars. George Bush started the Iraq war and faced a lot of opposition from the so-called progressives. But then Barack Obama is the record holder for the most number of days as being in office as the President of the United States while the nation was at war but hardly gets any opposition from those who opposed him. I have also noticed that the same people who opposed Bush are now war apologizers.

So economic orthodoxy lies ahead. What will be sad is that it will come from people to the left of Republicans in the political spectrum.

Jason Furman, Chairman of the Council of Economic Advisers to the President of the United States, has an article, The New View Of Fiscal Policy And Its Application for Vox. In this, he admits how wrong economists have been about fiscal policy. I’ve quoted his paper on which the article is based before here on this blog.

Furman says:

A decade ago, the prevalent view about fiscal policy among academic economists could be summarised in four admittedly stylised principles:

Discretionary fiscal policy is dominated by monetary policy as a stabilisation tool because of lags in the application, impact, and removal of discretionary fiscal stimulus.

Even if policymakers get the timing right, discretionary fiscal stimulus would be somewhere between completely ineffective (the Ricardian view) or somewhat ineffective with bad side effects (higher interest rates and crowding-out of private investment).

Moreover, fiscal stabilisation needs to be undertaken with trepidation, if at all, because the biggest fiscal policy priority should be the long-run fiscal balance.

Policymakers foolish enough to ignore (1) through (3) should at least make sure that any fiscal stimulus is very short-run, including pulling demand forward, to support the economy before monetary policy stimulus fully kicks in while minimising harmful side effects and long-run fiscal harm.

Furman then goes on to highlight how wrong each of the “principles” is.

He also says,

In the immediate postwar decades, economists broadly supported fiscal stimulus (e.g. Blinder and Solow 1973). But much of modern academic macroeconomics has ranged from dismissive of any effect of fiscal policy on the macroeconomy …

While that’s good, the main issue with the article is that it fails to mention that Post-Keynesians have argued about the strong effects of fiscal policy since long. Not only that, Furman advocates fiscal policy coordination across countries:

Finally, there may be larger benefits to undertaking coordinated fiscal action across countries.

Again, this is not “new” in any sense, just non-orthodox. Here is what Nicholas Kaldor said in 1984 in his lecturesCauses Of Growth And Stagnation In The World Economy:

I should like to end this series of lectures by suggesting the outline of a world-wide agreement on the necessary policies for recovery. The programme could be summed up under four main heads:

The first is coordinated fiscal action including a set of consistent balance of payments targets and “full employment” budgets.1 If this does not prove to be politically feasible, it is inevitable that the growth of unemployment will sooner or later force governments to take measures that would make it necessary for them to expand demand without being frustrated by the inevitable balance of payments consequence of expanding their economies relative to their trading partners. This means that there needs to be some form of restriction that would limit the increase in “competitive” imports to some target ratio in relation to exports. Trade liberalisation, which played such an important part in the rapid economic progress during the years of expansion, becomes a serious obstacle to economic recovery in the case of prolonged stagnation due to the inability of countries to achieve a coordinated set of policies. But, given a proper recognition of the problem, that under conditions of unrestricted free trade the actual volume of production and trade may in fact be considerably less than under some system of regulated trade – a system which relates the volume of imports in manufactures from a particular group of countries, such as the members of the EEC, to some mutually agreed ratio to the exports of individual members to the rest of the group – there is no reason why full employment should not be restored through policies of expansion, preferably directed by the expansion of State investment. This coordinated action by all countries, instead of isolated actions by each country, is the first and most important requirement of recovery.

1 At present all countries have fairly large deficits in the general government budget, but these are largely the consequence of the low level of activity. On a “full employment” basis they would show a highly restrictive picture – they would show surpluses and not deficits. Contrary to appearances, the requirement of stability is for expansionary budgets with lower taxes and higher expenditure, and not further fiscal restriction (as is advocated, for example, by M. de Larosiere of the International Monetary Fund).

But finally some sense prevails in the economics community. Jason Furman’s article should be used to argue against anyone who says: “we always knew” even though his/her position has shifted. So there’s nothing new about the “new view”. Just that economists from the mid-70s till now have been orthodox.

There’s a paper by Jason Furman who is the Chairman of the Council of Economic Advisers which concedes how wrong economists were on fiscal policy. The link is a file hosted at the White House’s website! The paper starts off with a remarkable admission on fiscal policy (h/t and words borrowed from Jo Michell)

A decade ago, the prevalent view about fiscal policy among academic economists could be summarized in four admittedly stylized principles:

Discretionary fiscal policy is dominated by monetary policy as a stabilization tool because of lags in the application, impact, and removal of discretionary fiscal stimulus.

Even if policymakers get the timing right, discretionary fiscal stimulus would be somewhere between completely ineffective (the Ricardian view) or somewhat ineffective with bad side effects (higher interest rates and crowding-out of private investment).

Moreover, fiscal stabilization needs to be undertaken with trepidation, if at all, because the biggest fiscal policy priority should be the long-run fiscal balance.

Policymakers foolish enough to ignore (1) through (3) should at least make sure that any fiscal stimulus is very short-run, including pulling demand forward, to support the economy before monetary policy stimulus fully kicks in while minimizing harmful side effects and long-run fiscal harm.

Today, the tide of expert opinion is shifting the other way from this “Old View,” to almost the opposite view on all four points. This shift is partly the result of the prolonged aftermath of the global financial crisis and the increased realization that equilibrium interest rates have been declining for decades. It is also partly due to a better understanding of economic policy from the experience of the last eight years, including new empirical research on the impact of fiscal policy as well as observations of the reaction of sovereign debt markets to the large increases in debt as a share of GDP in the wake of the global financial crisis. In the first part of my remarks, I will discuss the theory and evidence underlying this “New View” of fiscal policy (with, admittedly, the core of this theory being an “Old Old View” that dates back to John Maynard Keynes and the liquidity trap).

Compare that to the Post-Keynesian view, which according to Wynne Godley and Marc Lavoie in their book Monetary Economics written before the crisis (from chapter 1, Introduction):

The alternative paradigm, which has come to be called ‘post-Keynesian’ or ‘structuralist’, derives originally from those economists who were more or less closely associated personally with Keynes such as Joan Robinson, Richard Kahn, Nicholas Kaldor, and James Meade, as well as Michal Kalecki who derived most of his ideas independently.

… According to post-Keynesian ideas, there is no natural tendency for economies to generate full employment, and for this and other reasons growth and stability require the active participation of governments in the form of fiscal, monetary and incomes policy.

The United Nations Conference On Trade and Development’s annual report for 2016 is out and it’s worth reading as always. It’s generally written by non-orthodox authors.

There’s reference to Myrdal and Kaldor’s work on circular and cumulative causation: specifically the importance of manufacturing. See page 58 onward (page 92 of the pdf file).

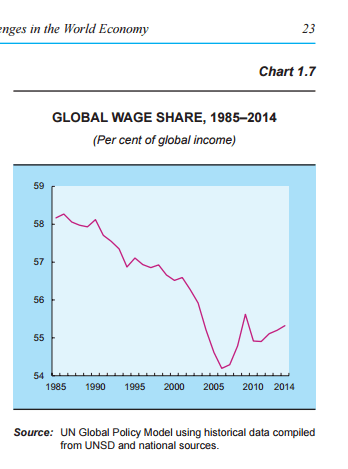

Another thing which caught my attention is the share of wages in the national income.

In my opinion, what Kaldor calls the principle of circular and cumulative causation (originally ascribed to Gunnar Myrdal) is as much an important principle in economics as is the Keynesian principle of effective demand. The former is built on top of the latter and so we could just have one most important Keynesian principle.

In an article Foundations And Implications Of Free Trade Theory, written in 📚 Unemployment In Western Countries – Proceedings Of A Conference Held By The International Economics Association At Bischenberg, France, Kaldor says:

Owing to increasing returns in processing activities (in manufactures) success breeds further success and failure begets more failure. Another Swedish economist, Gunnar Myrdal called this’the principle of circular and cumulative causation’.

It is as a result of this that free trade in the field of manfactured goods led to the concentration of manufacturing production in certain areas – to a ‘polarization process’ which inhibits the growth of such activities in some areas and concentrates them on others.

In a recent paper titled The debate Over ‘Thirlwall’s Law’: Balance-Of-Payments Constrained Growth Reconsidered, Robert Blecker says:

Another key empirical question is the direction of causality between export growth and capital accumulation: does the former cause the latter (as assumed implicitly in Thirlwall’s Law), or does the latter cause the former (as in some of the newer small-country models)? Perhaps this is a case of truly ‘circular and cumulative causation’, in which investment is required to promote exports and success in exporting in turn induces further investment.

I have always thought—ever since I have read Kaldor—that this is the case. When Kaldor says success creates more success, what he is really saying is that a rise in a success of a nation makes it more competitive and increases its exports and so on.

In Kaldorian models, however, elasticity of imports/exports is taken to be constant. Rise in production leads to a rise in productivity and hence price competitiveness. But there is no way in which there is a causation to non-price competitiveness (propensity to import, or income elasticities).

A more general modeling plus empirical work should actually study the impact on non-price competitiveness. Personally, my guess is that only this will explain the vast divergence in nations’ fortunes, empirically speaking. Without it, won’t be sufficient. Interestingly, I believe the dynamics could be complex and rich and even lead to convergence in some cases, although will remain just a theoretical curiosity.

Dani Rodrik has a new article, The Abdication Of The Left written for Project Syndicate. He says:

The good news is that the intellectual vacuum on the left is being filled, and there is no longer any reason to believe in the tyranny of “no alternatives.” Politicians on the left have less and less reason not to draw on “respectable” academic firepower in economics.

Consider just a few examples: Anat Admati and Simon Johnson have advocated radical banking reforms; Thomas Piketty and Tony Atkinson have proposed a rich menu of policies to deal with inequality at the national level; Mariana Mazzucato and Ha-Joon Chang have written insightfully on how to deploy the public sector to foster inclusive innovation; Joseph Stiglitz and José Antonio Ocampo have proposed global reforms; Brad DeLong, Jeffrey Sachs, and Lawrence Summers (the very same!) have argued for long-term public investment in infrastructure and the green economy. There are enough elements here for building a programmatic economic response from the left.

This is fine, but it wouldn’t be enough to solve the world’s problems because the world as a whole is balance-of-payments constrained as most individual nations are. What is needed is a coordinated response at the international level – a concerted action.

In his 1984 book Causes Of Growth And Stagnation In The World Economy, Nicholas Kaldor wrote:

I should like to end this series of lectures by suggesting the outline of a world-wide agreement on the necessary policies for recovery. The programme could be summed up under four main heads:

The first is coordinated fiscal action including a set of consistent balance of payments targets and “full employment” budgets.1 If this does not prove to be politically feasible, it is inevitable that the growth of unemployment will sooner or later force governments to take measures that would make it necessary for them to expand demand without being frustrated by the inevitable balance of payments consequence of expanding their economies relative to their trading partners. This means that there needs to be some form of restriction that would limit the increase in “competitive” imports to some target ratio in relation to exports. Trade liberalisation, which played such an important part in the rapid economic progress during the years of expansion, becomes a serious obstacle to economic recovery in the case of prolonged stagnation due to the inability of countries to achieve a coordinated set of policies. But, given a proper recognition of the problem, that under conditions of unrestricted free trade the actual volume of production and trade may in fact be considerably less than under some system of regulated trade – a system which relates the volume of imports in manufactures from a particular group of countries, such as the members of the EEC, to some mutually agreed ratio to the exports of individual members to the rest of the group – there is no reason why full employment should not be restored through policies of expansion, preferably directed by the expansion of State investment. This coordinated action by all countries, instead of isolated actions by each country, is the first and most important requirement of recovery.

1 At present all countries have fairly large deficits in the general government budget, but these are largely the consequence of the low level of activity. On a “full employment” basis they would show a highly restrictive picture – they would show surpluses and not deficits. Contrary to appearances, the requirement of stability is for expansionary budgets with lower taxes and higher expenditure, and not further fiscal restriction (as is advocated, for example, by M. de Larosiere of the International Monetary Fund).

Before the crisis, the economics profession believed in two orthodoxies:

crude version of Monetarism, which treats the stock of money as exogenous and also claims that fiscal policy is impotent.

free trade.

While policy response following the 2008 crisis have made economists realize that the first orthodoxy is wrong, they are yet to realize the orthodoxy of the second. As Joan Robinson said in her 1973 article, The Need For A Reconsideration Of The Theory Of International Trade, “there is no branch of economics in which there is a wider gap between orthodox doctrine and actual problems than in the theory of international trade”. The recent consensus of the economics profession on the debate about the UK EU referendum highlights it. Instead of the invisible hand, we need a visible hand, i.e., a coordination at the international level. The leftist response as highlighted by Dani Rodrik are welcome but still leave the problem open. So one needs both this and a world-wide fiscal expansion with balance-of-payments targets.

In the previous post, I highlighted Nicholas Kaldor’s view on the EU. I want to quote Wynne Godley’s views as well. Wynne Godley was highly influenced by Nicholas Kaldor so it is not surprising his views were similar.

In an article Wynne Godley Asks If Britain Will Have To Withdraw From Europe, written for London Review Of Books, written in October 1979, Godley writes:

The implications for Britain of EEC membership are rapidly becoming so perversely disadvantageous that either a major change in existing arrangements must be made or we shall have, somehow, to withdraw.

I strongly support the idea of Britain’s membership of the Common Market for political and cultural reasons. I would also support co-ordinated economic policies which were mutually advantageous to all the member countries. But this is not what we have got at the moment.

…

So we are all to be losers. The taxpayer through the Budget contribution, the consumer through higher food prices, the farmer through costs rising more than selling prices, and the manufacturer through rapidly rising import penetration.

…

… And if we may also take into account the dynamic effects, our balance of payments would be better by several thousand million pounds than it is at present. This would by itself have had a favourable effect on real national income and output, but, more important, it would have enabled the Government to pursue a less restrictive fiscal and monetary policy. According to preliminary estimates, the real national income could have been at least 10 per cent higher than at present and the rate of price inflation several points lower than if we had never joined the EEC.

It’s the United Kingdom European Union membership referendum tomorrow. In my opinion, the UK should leave the EU.

When discussing the Euro Area, it is emphasized frequently that Euro Area governments do not have the power to make expenditures by making drafts at the central bank as argued by Wynne Godley in 1992:

It needs to be emphasised at the start that the establishment of a single currency in the EC would indeed bring to an end the sovereignty of its component nations and their power to take independent action on major issues. As Mr Tim Congdon has argued very cogently, the power to issue its own money, to make drafts on its own central bank, is the main thing which defines national independence. If a country gives up or loses this power, it acquires the status of a local authority or colony. Local authorities and regions obviously cannot devalue. But they also lose the power to finance deficits through money creation while other methods of raising finance are subject to central regulation. Nor can they change interest rates.

The Euro Area was formed because Europeans wanted to come together and create a union which is big and powerful enough to be not affected by financial markets. The original intent was right but soon the whole idea came to be influenced by neoliberalism. The thing which was hugely missing (“the incredible lacuna” in Wynne Godley’s words in the above cited article) was the absence of central government of the Euro Area itself, which will have the power to collect taxes from Euro Area economic units and make expenditures. After some years of boom, the Euro Area found itself in crisis and could not deal with it well because there was no central government and fiscal policy to the rescue. The European Central Bank tried to save the monetary union but isn’t as powerful enough as a central government. More importantly, the Euro Area was brought into existence with the idea of free trade. Not only was power taken away from relatively economically weaker nations such as Greece but free trade was imposed by bringing their producers compete in the common market. In summary, there were two reasons why some Euro Area nations suffered.

The monetary arrangement

The common market.

Typically the former is emphasized more than the latter. Perhaps the reason is simple. It is easier to explain the former than the latter. In my experience, the latter is more difficult for people to understand and appreciate. Very few have emphasized it. Few exceptions are: Nicholas Kaldor, Wynne Godley.

Because economic growth is “balance of payments constrained”, free trade is devastating. The Euro Area could have had free trade if it had a central government which keeps imbalances in check because of fiscal transfers and regional policies.

Which brings us to the European Union itself and Britain’s membership. Although the UK government neither didn’t surrendered its sovereignty to make drafts at the central bank nor irrevocably fix the exchange rate in 1999, the nations’ producers still compete in the common market. It is better off leaving the European Union and have powers to impose tariffs on imports. Free trade is destructive to trade and one needs a lot of protection – at least the power of the optionality to impose such things any time a nation needs.

It was surpising to see less heterodox noise on this.

Nicholas Kaldor wrote a lot on this in the 1970s before the United Kingdom European Communities membership referendum in 1975. In his Collected Economics Essays, Volume 7, Nicky wrote (Introduction, page xxvi, October 1977) :

The final section of this volume, Part III, reproduces papers written in the course of the “Great Debate” on the question of British Membership of the Common Market in 1970 and 1971, and includes as a postscript a lecture on Free Trade written in 1977. As this debate came to an end when Britain entered the market, a decision which was later confirmed in popular referendum with a 2:1 majority, the reproduction of these papers may strike as otiose and serving little purpose other than somewhat ignoble one of self-vindication in the eyes of future historians. However, if the long-run effects of our membership turn out to be as disastrous as I feared they would be in 1971—and nothing that has happened has caused me to change my views—I think it is of the utmost importance that the true arguments against membership should be accessible to successive generations of students, the more so since the political debate continues to be dominated by issues (such as our effects of membership on the cost of food, on our agriculture, or the net budgetary cost of membership) which I regard as secondary and which could be brushed aside if the long-run effects on Britain’s manufacturing industry and on our capacity to provide employment were favourable.

…

[page xxviii] … the last essay of this volume, “The Nemesis of Free Trade”, which recounts the arguments in the great debate on Free Trade and Protection conducted at the beginning of this century between Herbert Asquith and Joseph Chamberlain. The points made on both sides seem to have lost none of their freshness or relevance in the intervening years. What has changed is our freedom to act. In 1905 we were free to decide whether to continue with the policy of free imports or to protect our industries. In 1977 the choice is no longer open to us, except at a political cost of withdrawing from the Common Market, an act which few people would contemplate seriously so soon after accession.

But after so many years, here is the chance to undo all this and withdraw from the EU. The UK should leave the EU.

This is the basis of the doctrine of the ‘foreign trade multiplier’, according to which the production of a country will be determined by the external demand for its products and will tend to be that multiple of such demand which is represented by the reciprocal of the proportion of internal incomes spent on imports. This doctrine asserts the very opposite of Say’s Law: the level of production will not be confined by the availability of capital and labour; on the contrary, the amount of capital accumulated, and the amount of labour effectively employed at any one time, will be the result of the growth of external demand over a long series of past periods, which permitted the capital accumulation to take place that was required to enable the amount of labour to be employed and the level of output to be reached which were (or could be) attained in the current period.

Keynes, writing in the middle of the Great Depression of the 1930s, focused his attention on the consequences of the failure to invest (due to unfavourable business expectations) in limiting industrial employment below industry’s attained capacity to provide such employment; and he attributed this failure to excessive saving (or an insufficient propensity to consume) relative to the opportunities for profitable investment. Hence his concentration on liquidity preference and the rate of interest, as the basic cause for the failure of Say’s Law to operate under conditions of low investment opportunities and/or excessive savings, and the importance he attached to the savings/investment multiplier as a short-period determinant of the level of production and employment.

On retrospect I believe it to have been unfortunate that the very success of Keynes’s ideas in connection with the savings/investment multiplier diverted attention from the ‘foreign trade multiplier’, which, over longer periods, is a far more important and basic factor in explaining the growth and rhythm of industrial development. For over longer periods Ricardo’s presumption that capitalists only save in order to invest, and that hence the proportion of profits saved would adapt to changes in the profitability of investment, seems to me more relevant; the limitation of effective demand due to oversaving is a short-run (or cyclical) phenomenon, whereas the rate of growth of’external’ demand is a more basic long-run determinant of both the rate of accumulation and the growth of output and employment in the ‘capitalist’ or ‘industrial’ sectors of the world economy.

– Nicholas Kaldor, Capitalism and industrial development: some lessons from Britain’s experience, Camb. J. Econ. (1977)1 (2):193–204, link