There have been too many praises for Mrs Thatcher after her death today.

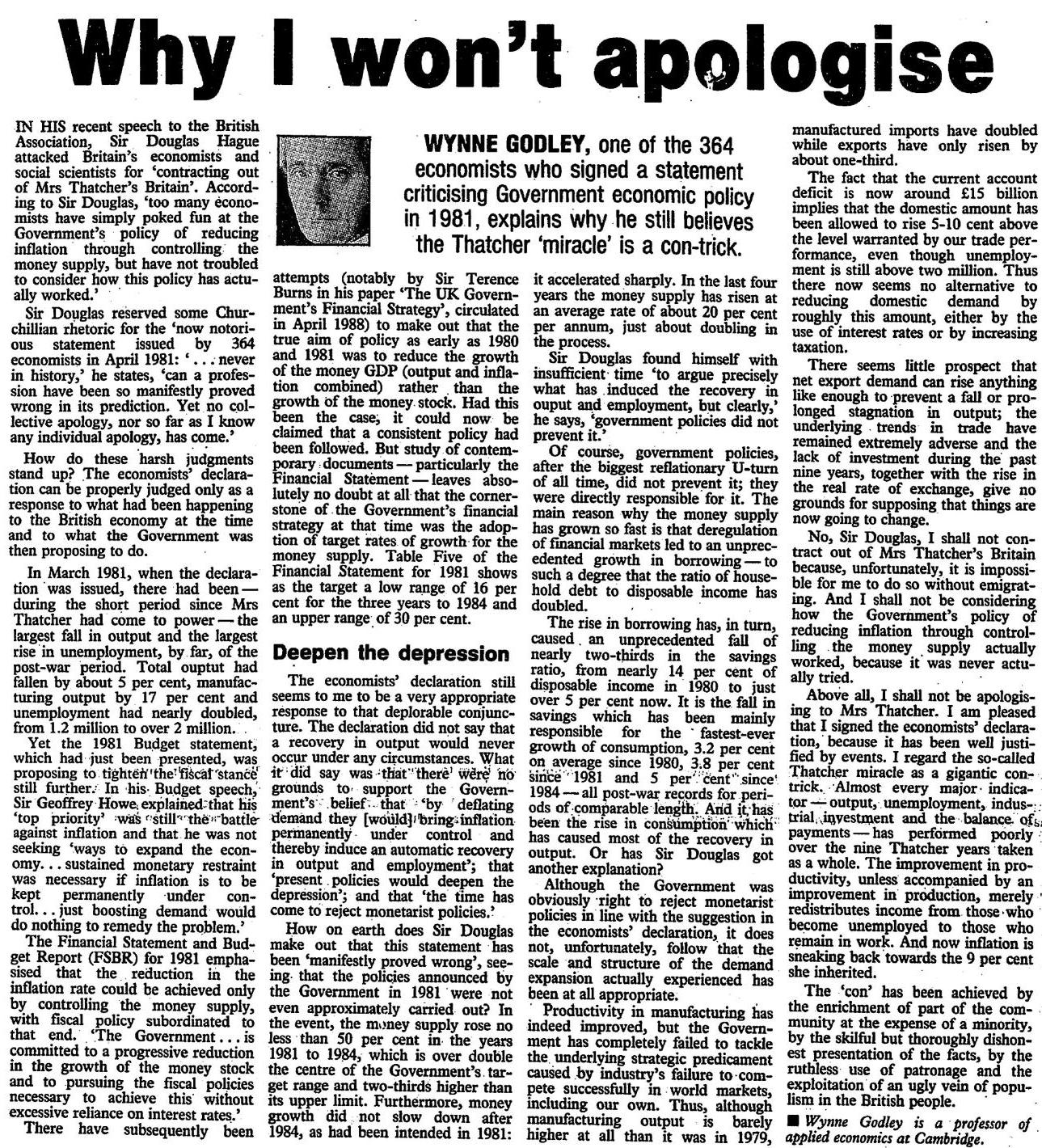

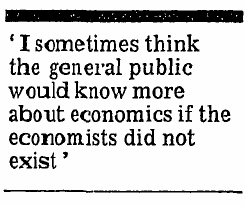

Wynne Godley once described the Thatcher “miracle” as a gigantic con-trick. Here is from a newspaper article:

I regard the Thatcher miracle as a gigantic con-trick. Almost every major indicator – output, unemployment, industrial investment, and the balance of payments has performed poorly over the nine Thatcher years taken as a whole … The ‘con’ trick has been achieved by the enrichment of part of the community at the expense of a minority, by skilful but thorougly dishonest presentation of the facts, by the ruthless use of patronage and the exploitation of an ugly vein of populism in the British people.

– Wynne Godley in Why I Won’t Apologize, September 18, 1988, Observer.

The article scan is below:

Wynne Godley, Why I Won’t Apologize (click to enlarge and click again)

Also see the papers which describes the right facts:

Coutts, K. and Godley, W. (1989), The British Economy Under Mrs Thatcher. The Political Quarterly, 60: 137–151. (Link)

Godley, W. (1990), The British Economy Under Mrs Thatcher: A Rejoinder. The Political Quarterly, 61: 101–102. (Link)

Thatcher’s bluff was caught very early by Godley. The huge rise in unemployment (to 3 million) was predicted first by Wynne Godley himself in 1979.

Reference: Godley W., ‘Britain’s chronic recession-can anything be done?’ in W. Beckerman (ed.) Slow Growth in Britain, Oxford University Press, 1979.

His King’s College Obituary (Annual Report, 2011) had this to say about Thatcherism:

Wynne rather relished his reputation as the ‘Cassandra of the Fens’. He famously made a double prediction: that under current policies of the first Thatcher government unemployment would inevitably rise to three million, but – the second prediction – that this would not in fact happen, on the grounds that, since in post-war Britain three million unemployed had to be an electoral suicide note, the policies would have to be changed. He was right with the first prediction, and – misreading the not-for-turning dispositions of the Iron Lady – wrong with the second. The actual outcomes appalled him. For Wynne the fundamental economic responsibility of a government was to ensure ‘full employment’. In pursuit of that aim he was uninhibited as Keynes himself and perhaps rather close in his motivation. He believed it was essential to use fiscal levers to stimulate demand, and was even prepared – though under very strict conditions – to countenance temporary import controls to protect and strengthen economic activity. His ideas were controversial and, like the man himself, often stood at an odd angle to the contemporary world, but the moral imagination which informed them was large and generous.

Economists struggle with simple things. Two examples.

National Saving, Trade Deficits etc.

In a blog article Has Anyone Heard of the Trade Deficit?, Dean Baker uses the sectoral balances identity to make a claim which is presented like a no-go theorem.

Baker says:

Fans of arithmetic (a tiny minority among DC policy types) like to point out that a large trade deficit implies negative national savings. In other words, if we have a trade deficit then by definition the United States as a whole has a negative saving rate.

This means that we either must have budget deficits (negative public savings) or negative private savings, or both. There is no way around this fact.

Baker confuses saving with saving net of investment – just like the Neochartalists. (Confuses S with S minus I)

Without proof, the sum of saving of a whole economy is given by

S = I + BP

where (here) S is the sum of the savings of all resident sectors of the economy – the “national saving”, I is the total investment expenditure of the resident sectors of the economy (i.e., both private and public) and BP is the current account balance of international payments.

So it is possible for an economy to have a trade deficit and hence a negative BP (although it’s not always the case that the trade deficit translates into a current account deficit) and still have I + BP positive if investment is sufficiently high. So an economy can have positive national saving with a trade deficit.

Of course it must be said that the persons he is attacking are wrong. The claim (of the persons he is criticizing) is that the United States should save more (by a reduction in budget deficits brought about by a tightening of fiscal policy and/or higher propensity to save of the private sector achieved in some way). This is illegitimate as such a policy will induce a recession in the United States. Via the paradox of thrift, an increase in the private sector propensity to save can lead to lower saving of the private sector. Investment will fall because of lower sales expectations and the recession in the United States caused by the fiscal tightening will most likely lead to a recession in the rest of the world reducing its exports so that the only thing achieved is higher world unemployment.

Debt/GDP Ratio

In a series of posts aimed at showing something, Randall Wray claims the following:

… To simplify, if the interest rate is higher than the economy’s growth rate, then the debt ratio rises continuously…

Of course he also claims that if g>r, the debt ratio stabilizes.

Now, the debt sustainability conditions relating the interest rate and the growth rate of output are misleading. I showed this two posts back, where I showed that the claim that the condition that g>r ensures stabilization of the public debt/gdp ratio is incorrect. The above quote claims the opposite and is equally erroneous and misleading.

An economy can have the growth rate lower than the interest rate and still not have an exploding debt ratio.

A standard error in such analysis is to treat the budget deficit as exogenous.

Consider an economy without a strong balance of payments constraint and with inflation less of a trouble. A fiscal expansion brings about an increase in output and this has the effect of stabilizing the debt ratio in two ways: the higher output itself and an increase in tax revenues of the government due to higher output. The budget balance may go into primary surplus automatically even though the government may not be targeting this.

In other words, if r>g, the sequence dn given by the relation

dt – dt-1 = λdt-1 – pbt

(where λ is equal to (r-g)/(1+g) and dtis the debt/gdp ratio at the end of time period t and pbt is the primary budget balance of the government in the period) would seem to explode because of the first time on the right hand side. But higher output will automatically lead to a dynamics for pbt ensuring sustainability.

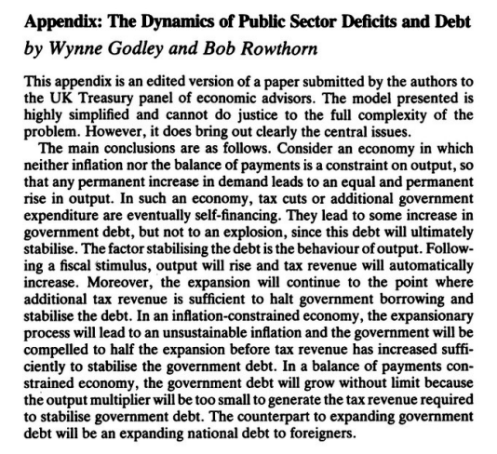

How this works was shown by Wynne Godley in an article The Dynamics Of Public Sector Deficits And Debts written in 1994 written by his co-author Bob Rowthorn in J. Michie and J. Grieve Smith (eds), Unemployment in Europe (London: Academic Press), 1994 pp. 199-206 and which was originally a paper to the UK Treasury around ’92-’93.

For a demand constrained economy:

… Note that the primary budget balance adjusts automatically so as the stabilise the debt to GDP ratio. This spontaneous adjustment occurs through induced variations in GDP. The government cannot directly determine the primary balance. It can only control r, θ and G, and once the time path of these is fixed as above, the variable Y will evolve so as to stabilise the ratio B/Y. If this ratio is too large, Y will grow rapidly and generate sufficient tax revenue to bring this ratio down.

There is a standard proposition that the government cannot permanently maintain a primary deficit if the interest rate is greater than the growth rate (r>g) … even if true, the statement can be misleading. In a demand-constrained economy, the level of Y relative to G will automatically adjust so as to produce a primary balance (deficit or surplus) to stabilise the ratio B/Y …

It is counterproductive to go around making statements about the conditions on interest rate and the growth rate without qualifications and care and considering a situation/history and future scenarios.

There is one place where this condition is useful. Consider a balance of payments constrained economy. In studying the sustainability of the external debt of a country, one can conclude that if r>g (where r is the effective interest rate paid on foreign liabilities), then the debt dynamics will lead to an exploding debt even if the trade balance is held constant. Of course that doesn’t mean if r<g alone ensures sustainability.

In a five-part series in his blog, Functional Finance and the Debt Ratio Scott Fullwiler claims that if the interest rate is held below the growth rate of output, sustainability of the public debt/gdp ratio is guaranteed in the sense that the ratio converges and does not keep increasing forever. This is erroneous and his conclusions are misleading.

Wolfgang Schäuble understands the connection between public finances and international competitiveness, although his solutions are all wrong. Heteredox economists should understand this connection as well!

Rather than write a detailed essay, I thought I should directly get to the point and pinpoint his errors. Of course, several Post Keynesians even before Fullwiler wrote his 2006 paper Interest Rates And Fiscal Sustainability (referred in his posts) have made this claim and this criticism applies to them as well.

While there are future scenarios, where growth improves the public debt/gdp ratio, it does not mean that all scenarios lead to a convergence. Fullwiler has examples in his posts where he shows how the convergence happens. But it doesn’t prove much.

Fullwiler’s error is a simple mathematical one. He sums the series for debt-sustainability equation and shows the the public debt/gdp ratio converges to

– pb/(g – r)

where pb is the primary balance/gdp ratio, g is the growth rate of output and r the interest rate. [notations are changed somewhat without any effect on conclusions]

This is a wrong result because it assumes that the primary balance is constantas a percentage of gdp. The series he sums need not converge if the primary balance in each period is different. One such scenario is when the deficit in each period is bigger than the deficit of the previous period. Fullwiler claims:

… in terms of convergence or unbounded growth of the debt ratio, as Jamie Galbraith put it, “it’s the interest rate, stupid!” since any level of primary deficit can converge if the interest rate is below the growth rate.

[italics and link in original]

This is repeated:

… More importantly, given an interest rate lower than GDP growth, any primary budget deficit will eventually converge …

Now this doesn’t make sense. The claim that “any” level of primary deficit can converge if the interest rate is below the growth rate is incorrect. For example, if we have primary balances pb0, pb1, pb2 and so on and each of them is growing sufficiently faster, the debt/gdp ratio is explosive even if interest rate is less than the growth rate of output. His result is valid if each of the balances pb0, pb1, pb2 … are equal to each other and not in general.

In other words, if g>r, the sequence dn given by the relation

dt – dt-1 = λdt-1 – pbt

where λ is equal to (r-g)/(1+g) need not converge for general values of pbn and only converges in special circumstances (if suppose the pbn are all equal or more realistic if there is a mechanism to bring the primary deficit into a surplus which may or may not be a discretionary attempt by the government.)

Example

Nothing of the above is purely academic. So in what situation can the public debt explode?

Let us assume an open economy. Let us assume that a country’s exports is X0 and not growing because of its inability to increase its market share or because of limited demand in world markets due to deflationary policies adopted by the rest of the world. Or both.

If one imagines a scenario in which there is growth in output and hence income, imports rise as well in a world of free trade. This implies the current account deficit explodes. While growth may work to improve the debt/gdp ratio, the current account deficits work to worsen the debt ratio. The net effect is that “growth” instead of improving the debt/ratio worsens it.

This can be seen if one remembers that the sectoral balances identity connects the public sector deficit and the current balance of payments. We have

NAFA = PSBR + BP

where NAFA is the private sector net accumulation of financial assets, PSBR is the public sector borrowing requirement (the deficit) and BP is the current account balance of international payments.

Since the private sector typically wishes to have a positive NAFA (else there is another unsustainable process!), an exploding BP leads to an exploding PSBR if output grows much faster than exports. This implies the public debt/gdp grows forever and growth is not sustainable.

Now Fullwiler can potentially claim that the government can “simply credit bank accounts” and public debt/gdp and external debt/gdp rising forever is no cause for trouble but then why write a post claiming convergence of the ratios!

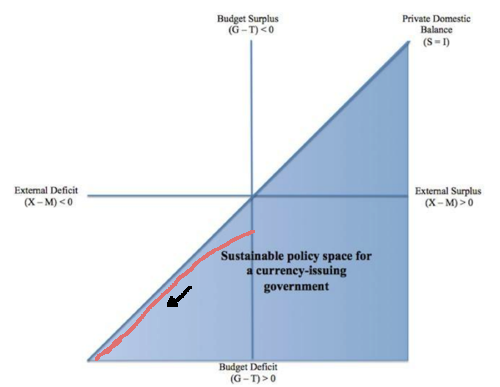

There is a diagram in the post which I modified below with a red line for a path for the sectoral balances. Is the claim that this line extrapolated leads to a stabilizing debt ratio?

[image updated]

Wynne Godley And Debt Dynamics

The above was pointed out by Wynne Godley in the 1970s. The following brings it out clearly. It is from an appendix to an article written by his co-author Bob Rowthorn in J. Michie and J. Grieve Smith (eds), Unemployment in Europe (London: Academic Press), 1994 pp. 199-206 and was originally a paper to the UK Treasury around ’92-’93

Conclusion

Now this may sound as a pessimistic view for any individual nation or the world as a whole. The real problem is free trade – the most sacred tenet of the economics profession.

I came across this article (via a Tweet from Stephen Kinsella): Accounting As The Master Metaphor Of Economics by Arjo Klamer and Donald McCloskey which discusses how the framework of national accounts has been pushed to the background in economic analysis over the years.

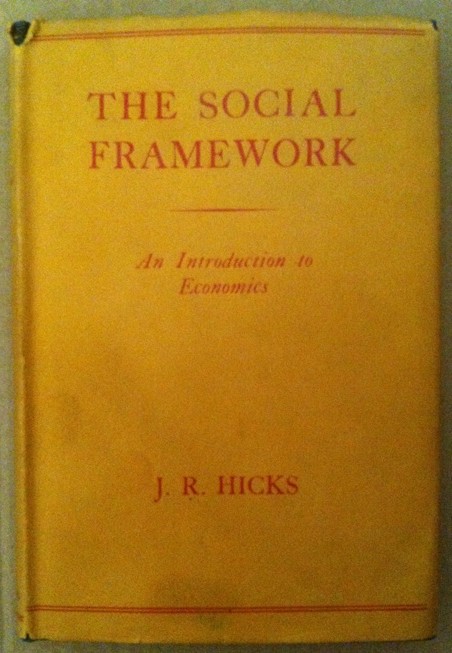

It is a nice read – although boring in a few places. I found this reference to John Hicks’ 1942 book The Social Framework: An Introduction To Economics in the above article and managed to get a copy – although a used one but with almost no usage. As described in the Klamer-McCloskey’s article, Hicks’ textbook really goes into details of national accounts and he seems to have had a great intuition of how it all works.

Hicks’s book gives a nice introduction to how important national accounts are in understanding and describing the production process and economic cycles.

Here is a scan of two pages on the balance of payments – the topic I like the most.

(click to enlarge)

Hicks understood how weak balance of payments can cause troubles. Of course, it took the genius of Nicholas Kaldor to realize the supreme importance of balance of payments in the determination of national income and expenditure. Leaving that aside, the text has nice ideas and discussions on how stocks and flows feed into one another.

John Hicks is famous for an entirely different reason – the IS/LM model. Later he accepted it was a huge mistake, but put it mildly: “… as time as gone on, I have myself become dissatisfied with it”. But economists still keep using it and keep erring.

Also, Hicks was to soon abandon/forget his own social accounting approach as per Klamer-McCloskey’s article. Perhaps, not really.

In an extremely important paper, Wynne Godley said:

To come down to it, the present paper claims to have made, so far as I know for the first time, a rigorous synthesis of the theory of credit and money creation with that of income determination in the (Cambridge) Keynesian tradition. My belief is that nothing the paper contains would have been surprising or new to, say, Kaldor, Hicks, Joan Robinson or Kahn.

John Hicks also had another nice book called A Market Theory Of Money written in 1989. Here is a great insight (also the view of Kaldor) from Page 11, Chapter 1 named “Supply And Demand?” on how to create a dynamic Keynesian theory of determination of national income and expenditure:

… The traditional view that market price is, at least in some way, determined by an equation of demand and supply had now to be given up. If demand and supply are interpreted, as had formerly seemed to be sufficient, as flow demands and supplies coming from outsiders, it is no longer true that there is any tendency over any particular period, for them to be equalized: a difference between them, if it were not too large, could be matched by a change in stocks. It is of course true that if no distinction is made between demand from stockholders and demand from outside the market, demand and supply in that inclusive sense must be equal. But that equation is vacuous. It cannot be used to determine price, in Walras’ or Marshall’s manner. For what matters to the stockholder is the stock that he is holding: the increment in that stock, during a period is the difference between what is held at the end and what was held at the beginning, and the beginning stock is carried over from the past. So the demand-supply equation can only be used in a recursive manner, to determine a sequence (It is a difference or a differential equation); it cannot be used directly to determine price, as Walras and Marshall had used it.

which is the now famous sectoral balances identity! Incidentally, it also includes Kalecki’s profit equation. In the above “Foreign Investment” shouldn’t be confused with Foreign Direct Investment flows in the financial account of the balance of payments. The authors define it as:

… equal to income generated by receipts from abroad less current expenditure abroad.

So can we call the profit equation SMK equation? 🙂

James Meade and Richard Stone were pioneers of national accounts. Incidentally, James Meade wrote a famous textbook on balance of payments.

Of course the way this is presented doesn’t make the connection between the financial account and current accounts. The sectoral balances was usually written by Wynne Godley as:

NAFA = PSBR + BP

where NAFA is the net accumulation of financial assets of the private sector, PSBR is the net public sector borrowing requirement, and BP is the current account balance of international payments. More on this connection below.

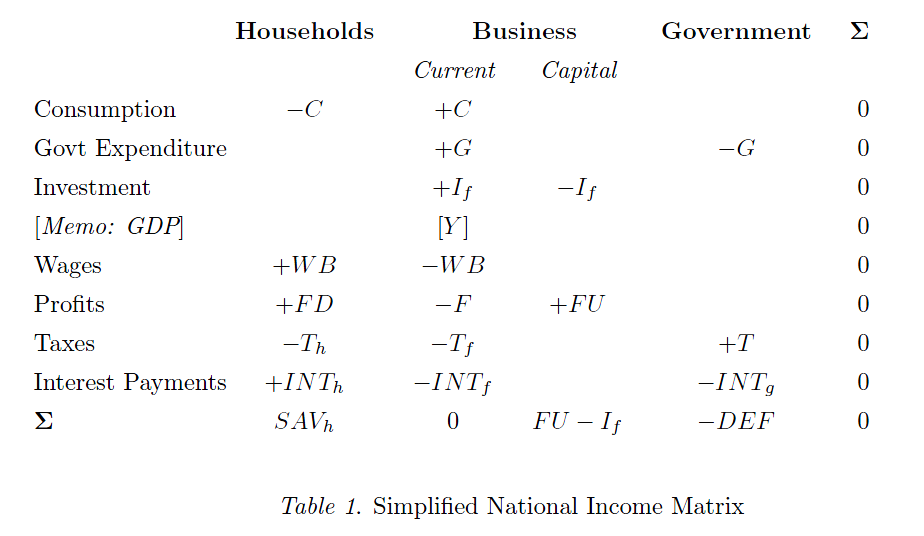

How it is to be derived in a stock-flow consistent framwork of Godley/Lavoie? If you click on this search Transactions Flow Matrix, you will find some blog posts on the background. First, we construct a flow matrix like this:

The last line is essentially Kalecki’s profit equation.

The above construction however raises an important question. Godley and Lavoie’s textbook (Chapter 2) quotes a famous 1949 article of Morris Copeland on this:

When total purchases of our national product increase, where does the money come from to finance them? When purchases of our national product decline, what becomes of the money that is not spent?

Copeland’s work was highly successful and established the flow of funds accounts of the United States in 1952.

Here is a republished version of the article (via Google Books):

click to preview on Google Books’ site

Incidentally, Copeland was motivated to prove the quantity theory of money wrong when he did this work! Also Godley/Lavoie point out that John Dawson (the editor of the above book) says:

the acceptance of…flow-of-funds accounting by academic economists has been an uphill battle because its implications run counter to a number of doctrines deeply embedded in the minds of economists.

in an article from the chapter The Conceptual Relation Of Flow-Of-Funds Accounts To The SNA of the same book.

Over time, the system of national accounts (with its first version in 1947) has used some of the concepts of flow of funds accounting and now the framework is much more wider than usual textbook guides of national accounts. The flow of funds still retains importance because it has information which the system of national accounts such as (2008 SNA) doesn’t handle.

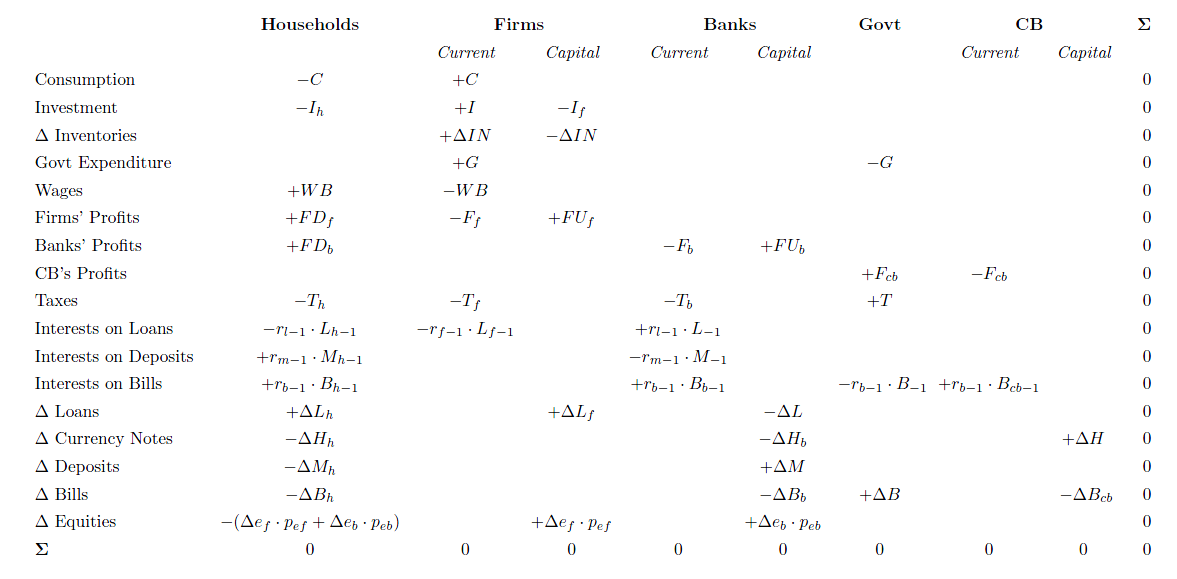

How does one look at this in a stock-flow coherent framework? Simple, we need a full transactions flow matrix – which not only includes income/expenditure flows but also financial flows. The following is how it looks like for a simple model:

Formally, prescribing a closure boils down to stating which variables are endogenous or exogenous in an equation system largely based upon macroeconomic accounting identities, and figuring out how they influence one another.

Business Insider’s Joe Weisenthal interviewed Goldman Sachs’ Jan Hatzius recently with questions aimed at his usage of the sectoral balances approach:

…

BI: Back to the balance sheet, multi-sectoral framework of looking at the economy. How did you come to this view? On Wall Street this is still very rare. I don’t see many economist talk about the economy this way, recognizing this identity and making projections based on it. How did you come to see this as the framework by which we should be looking at the economy right now?

HATZIUS: I’ve long been fascinated with looking at private sector financial balances in particular. There was an economics professor at Cambridge University called Wynne Godley who passed away a couple of years ago, who basically used this type of framework to look at business cycles in the UK and also in the US for many many years, so we just started reading some of his material in the late 1990s, and I found it to be a pretty useful way of thinking about the world.

It’s usually not something that gives you the secret sauce at getting it all right, because there are a lot of uncertain inputs that go into this analytical framework, but I do think it’s a reasonable organizing framework for thinking about the short to medium term ups and downs of the business cycle.

Basically, in order to have above trend growth, a cyclically strong economy, you need to have some sector that wants to reduce its financial surplus or run a larger deficit in order to provide that sort of cyclical boost, most of the time.

There are other factors at play in the business cycle – I’m certainly not claiming that ‘this is it!’ – but I have found it to be pretty useful.

I frequently quote Wynne Godley’s Maastricht And All That written for the London Review Of Books in 1992. Here’s from another article (paywalled) for the same magazine from 1993:

I am in favour of Britain having much closer ties with other European countries, provided that appropriate institutions are created and the whole thing is brought under effective political control …

… The tract made only two points: that a single currency would remove the instability caused by fluctuating exchange rates, thereby enabling business to plan more reliably, and that international traders would no longer incur ‘transaction costs’ in the form of the small margin they now have to pay dealers when they buy and sell foreign exchange. It was as simple as that! The brief contained no reference whatever to the obvious fact that by joining a currency union, member countries would be giving up powers of independent action which at present they possess. It follows a fortiori that the document said nothing about who those powers would be given up to, and how the new authorities would exercise them …

… And if an individual country cannot issue its own money, it has no more power to conduct an independent fiscal policy than has a local authority, say, or an erstwhile colony in an imperial system …

… But to the extent that national governments can no longer be effective, this points to a pressing need for some supranational authority, call it a federal government, to carry out these functions …

… It is a good moment to start again. I think the Maastricht enterprise was built on a premise that has turned out to be completely mistaken: namely, that there can exist some kind of union between countries which is much more than a community of independent nations with special trading arrangements but much less than a full-blown political union. Maastricht is a half-baked half-way house and, with the CAP always at the back of my mind, I cannot agree that it is right to support it on the grounds that it is the only route ahead, the full nature of which will only be revealed in due course. Going forward should now mean that we explicitly hand over the main instruments of independent policy-making to some properly constituted body under appropriate political control. If this is not what Britain wants, is it completely out of the question that we now deliberately go backwards?

[italics in original, boldening mine]

– Wynne Godley in Derailed, London Review Of Books, 1993

I thought I should share what I found recently about who was to state the sectoral balances identity first – since it comes across as enlightening to say the least. I found the identity in Nicholas Kaldor’s 1944 article Quantitative Aspects Of The Full Employment Problem In Britain. It was published as Appendix C to Full Employment In A Free Societyby William Beveridge.

(If you find the mention of this identity anywhere before, please let me know!)

Here’s a Google Books screenshot of the page:

The article also appears in Kaldor’s Collected Essays, Vol 3 (Chapter 2, pp. 23-82).

The ‘net’ is net of consumption of fixed capital. Also ‘balance of payments’ is used for the current balance (footnote 1, page 28). (In TheScourge Of Monetarism, Kaldor used ‘net saving’ as saving net of investment).

Anthony Thirlwall wrote a biography of Kaldor in 1987 and he mentions that Kaldor kept pushing the implications of the identity in the 1960s (page 251). He managed to convinced some of his colleagues such as Wynne Godley and Francis Cripps and pick up public fights with others such as Richard Kahn.

Wynne Godley recalled how he came to appreciate this identity in his book Monetary Economics with Marc Lavoie. In Background Memories (W.G.) he wrote:

… In 1970 I moved to Cambridge, where, with Francis Cripps, I founded the Cambridge Economic Policy Group (CEPG). I remember a damascene moment when, in early 1974 (after playing round with concepts devised in conversation with Nicky Kaldor and Robert Neild), I first apprehended the strategic importance of the accounting identity which says that, measured at current prices, the government’s budget deficit less the current account deficit is equal, by definition, to private saving net of investment. Having always thought of the balance of trade as something which could only be analysed in terms of income and price elasticities together with real output movements at home and abroad, it came as a shock to discover that if only one knows what the budget deficit and private net saving are, it follows from that information alone, without any qualification whatever, exactly what the balance of payments must be. Francis Cripps and I set out the significance of this identity as a logical framework both for modelling the economy and for the formulation of policy in the London and Cambridge Economic Bulletin in January 1974 (Godley and Cripps 1974). We correctly predicted that the Heath Barber boom would go bust later in the year at a time when the National Institute was in full support of government policy and the London Business School (i.e. Jim Ball and Terry Burns) were conditionally recommending further reflation! We also predicted that inflation could exceed 20% if the unfortunate threshold (wage indexation) scheme really got going interactively. This was important because it was later claimed that inflation (which eventually reached 26%) was the consequence of the previous rise in the ‘money supply’, while others put it down to the rising pressure of demand the previous year …

So the news is that Mark Carney – the Governor of the Bank of Canada will now be the next Governor of the Bank of England.

Wynne Godley would have been happy – had he been alive and known that Carney is perhaps the only central banker to have recognized his foresight. (Carney probably is also the only central bank head to have named some names.)

… Few forecast these events; although, in an outbreak of retrospective foresight, an increasing number now claim they saw it coming. The reality is that among all the banks, investors, academics and policy-makers, only a handful were able to identify ahead of time the causes and potential scale of the crisis. …

with an attached footnote:

Examples include Bill White, formerly of both the Bank of Canada and the Bank for International Settlements; Harvard University’s Ken Rogoff; Nouriel Roubini of New York University; Wynne Godley of Cambridge; and Bernard Connolly of AIG Financial Products.

I recite all this to suggest, not that sovereignty should not be given up in the noble cause of European integration, but that if all these functions are renounced by individual governments they simply have to be taken on by some other authority. The incredible lacuna in the Maastricht programme is that, while it contains a blueprint for the establishment and modus operandi of an independent central bank, there is no blueprint whatever of the analogue, in Community terms, of a central government. Yet there would simply have to be a system of institutions which fulfils all those functions at a Community level which are at present exercised by the central governments of individual member countries.

The counterpart of giving up sovereignty should be that the component nations are constituted into a federation to whom their sovereignty is entrusted. And the federal system, or government, as it had better be called, would have to exercise all those functions in relation to its members and to the outside world which I have briefly outlined above.

That was published 8th October 1992 – exactly 20 years back!

Worth your time if you haven’t read it yet. Even if you have, worth reading it again!

Here’s the link to the full article Maastricht And All That by Wynne Godley.

He has a nice way of giving a short description of pricing in the G&L models:

In my view, the stock-flow and the demand driven (and I should say, the fact that price dynamics is orthogonal to the income flow determination structure) is the essential characteristic of this approach.

—

Also, Simon Wren-Lewis (from Oxford) has a new blog post on the sectoral balances approach – Sector Financial Balances As A Diagnostic Check, where he mentions Martin Wolf’s recent post on Wynne Godley’s approach. He (Wren-Lewis) has been admitting recently that DSGE models are not useful.

In the comments section Simon Wren-Lewis has this to say:

Martin Wolf sent me the following comment, which I am sure others will also find interesting:

“I used sectoral financial balances before the crisis, following Wynne. I argued that what was going on in the US external and household sectors were evidently unsustainable. This allowed me to argue that when the latter’s deficits were eliminated, there would be a recession and a huge fiscal deficit. What I had not expected was that the turnaround in the household sector would trigger a meltdown of the financial system.

“This makes it clear that one has to link the flow sectoral balances to the balance sheets in the economy. In this case, my mistake was not looking closely enough at the balance sheet of the financial sector. Good macroeconomic analysis has to examine the flows and stock meticulously and seek to assess whether the behaviour we see is sustainable. The assumption that private agents cannot make huge mistakes about the sustainability of what they are doing is, in my view, the biggest mistake in macroeconomics.”

Back to DSGE models. I think they are totally useless. I like this quote by Francis Cripps from an article in The Guardian from 27 Feb 1979: Economists With A Mission: