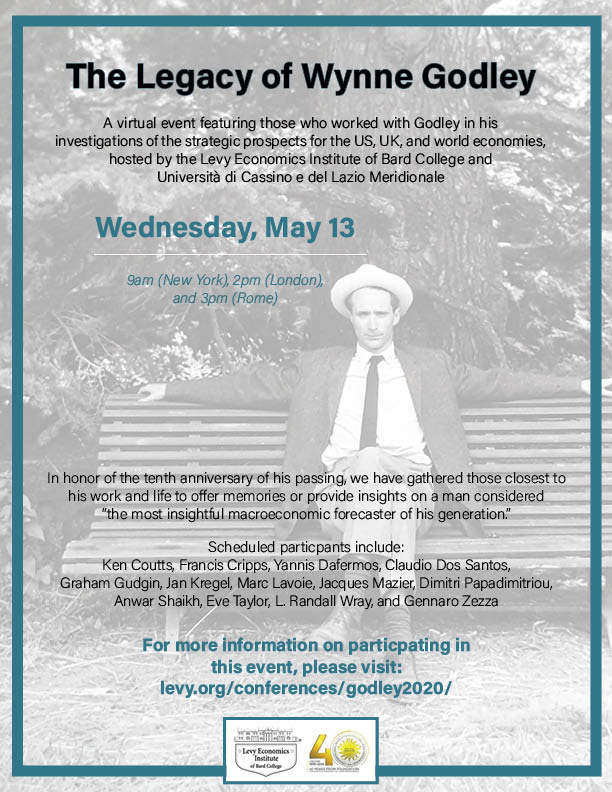

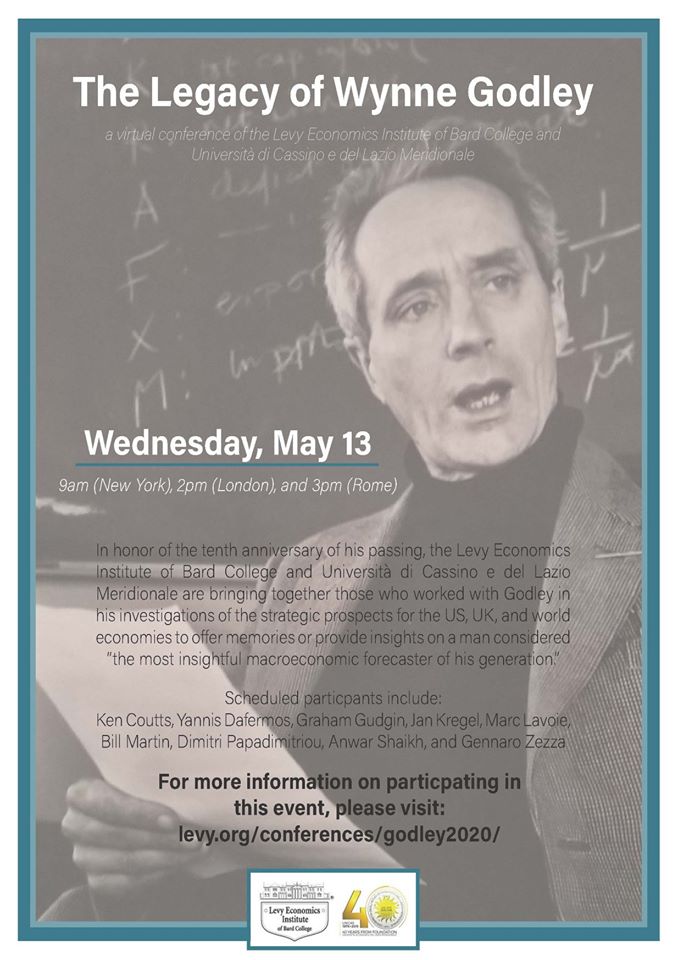

Jan Hatzius of Goldman Sachs talks about how he drew inspiration from Wynne Godley in the latest Odd Lots podcast hosted by Joe Weisenthal and Tracy Alloway of Bloomberg.

He talks of how the private sector financial balance (or net lending) is an important thing to look at to predict crisis.

Wynne Godley in a 1988 article, The Sensibility Of Contemporary Institutions in Theology, (first given as a Sermon before the University in King’s College Chapel, 31 May 1987:

Recourse to the dictionary gives, among the definitions of the word sensibility, ‘the glad or sorrowful recognition of a fact or a condition of things’. Also, ‘readiness to feel compassion for suffering’.

…

But the major issues at stake have been vastly more important than ones which concern sensibility narrowly defined. They go beyond who becomes rich and who remains poor. They extend to matters such as slavery, mass unemployment and civil war.

…

… The IMF would do well to reperuse its own Article I, which .lists among its purposes: ‘to facilitate the expansion and balanced growth of international trade, and to contribute thereby to the promotion and maintenance of high levels of employment and real income and to the development of the productive resources of all members as primary objectives of economic policy … ‘ In this passage you hear the authentic note of optimism and mutual concern which informed economic relationships within and between countries in the first twenty-five years after the war.

I have been forced to recognize with sadness and very great disappointment that I have so far failed in my personal endeavour to change the course of events or the attitudes of other people. But I remain steadfast to what I understand to be the meaning of Christianity: the unique value it places on the individual inner life; the ability to tolerate aloneness and the imminence of death; the joyful and sensitive concern for and love of other human beings.

From Alan Shipman’s biography, Wynne Godley, A Biography, Chapter 9: Balance Of Payments, Deindustrialisation And Protection, page 151:

Of all Godley’s policy prescriptions, direct import controls were the one most roundly rejected by other economists, and least likely to be adopted by politicians with any chance of gaining power. The accusation of advocating a policy that was economically illogical, politically infeasible and inadmissible in international law hurt deeply, but never crushed his belief that import quotas should be seriously considered as an additional macroeconomic instrument. The depth of the wound emerged in an unusually personal statement to a 1978 conference on ‘Slow Growth in Britain’, convened by Oxford University’s Wilfred Beckerman in Bath. ‘I am disconcerted and distressed to find myself, together with the group of people with whom I work in Cambridge, in such an isolated position. For we seem to be the only group of professional economists who entertain the possibility that control of international trade may be the only way of recovering and maintaining the prosperity of this country; that free trade may be an enemy for the relatively weak’ (Godley 1979: 226).

…

References

…

Godley, W. (1979). Britain’s chronic recession—Can anything be done? In W. Beckerman (Ed.), Slow Growth in Britain. Oxford: Clarendon Press.

A study of the history of opinion is a necessary preliminary to the emancipation of the mind.

Although in the poor countries, ones colonised and which suffered because of imposition of laissez-faire, there have been a lot of opposition to free trade—and those voices aren’t heard through silencing internationally—in the advanced countries, it has been almost non-existent except from Cambridge Keynesians and maybe a few others. In recent times, we see some opposition, but not remotely like this even 40 years ago. It is important to know the history of thought to understand how hegemonic the ruling ideology has been.

For Wynne Godley, dissenting against free trade was one of the most important reasons for his dissent against the profession. In his short autobiography written in 2001 for A Biographical Dictionary Of Dissenting Economists, Godley said:

There are two aspects (in particular) of the work of the CEPG [Cambridge Economic Policy Group] which put its members into a category which may he termed ‘dissenting’. The first – a matter mainly of concern to the modelling fraternity and academic econometricians – was the unconventional view we took about how to construct and use an econometric model.

…

The second, and more egregious, respect in which we became a ‘dissident’ group was that, as a result of trying to think through the possible ways in which Britain’s net export demand might be improved, we entertained the possibility that international trade should be, in some sense, ‘managed’. There might, we argued, be no way in which the adverse trends could be reversed other than some form of control of imports. Our argument (see for instance Cripps, 1978; Cripps and Godley, 1978) was never one in favour of protectionism as normally understood – that is, the selective and unilateral protection of relatively failing industries under conditions of general stagnation. On the contrary, we were most careful to lay down conditions under which the management of trade would benefit not only our own country (without making its industry less efficient) but would also increase the level of trade and output in the rest of the world. The two basic principles were, first, that trade management should reduce import propensities without ever reducing imports themselves (in total) below what they otherwise would have been; and, second, that ‘protection’ should be as minimally selective as possible (for example, through the use of market mechanisms such as auction quotas) so that industrial inefficiency would not be sponsored.

I was surprised by the hostility with which our ideas about trade were received. It seemed to me at the time, and still seems to me, that the arguments actually used against us (at their most coherent by Maurice Scott et al., 1980) did not, in practice, rest on a well-articulated theoretical position but on very special assumptions about behavioural relationships and international political responses. (I have, to the best of my ability, answered these particular points in Christodoulakis and Godley, 1987.)

…

The ‘dissident’ argument in favour of managed trade is well summarized in Kaldor (1980), where he points out that the modern theory of international trade is based on the assumption that all production takes place according to the conditions described by the neoclassical production function, with constant returns to scale. Kaldor postulated instead, and he was surely right to do so, that the principle of circular and cumulative causation leads (through dynamically increasing returns) to a process, not of convergence, but of polarization between successful and unsuccessful economies in which success in competitive performance feeds on itself and losers become immiserated by trade.

…

Godley’s Major Writings

…

(1978), ‘Control of Imports as a Means to Full Employment: The UK’s Case’ (with T.F. Cripps), Cambridge Journal of Economics, 2, September.

…

(1987), ‘A Dynamic Model for the Analysis of Trade Policy Options’ (with N. Christodoulakis), Journal of Policy Modelling, 9.

…

Other References

Cripps, T.F. (1978), ‘Causes of Growth and Recession in World Trade’, Cambridge Economic Policy Review, No. 4.

Kaldor, N. (1980), ‘The Foundations of Free Trade Theory and Recent Experiences’, in E. Malinvaud and Fitoussi, J.P. (eds), Unemployment in Western Countries, London: Macmillan.

…

Scott, M., Corden, W.M. and Little, I.M.D. (1980), The Case Against Import Controls (Thames Essay No. 24), London: Trade Policy Research Centre.

There’s a nice recent six-page biography of Wynne Godley in The New Palgrave Dictionary Of Economics by Gennaro Zezza and Alan Shipman. Shipman had recently written a full biography on Wynne Godley’s life.

Abstract:

The chapter provides a brief biography of Wynne Godley (1926–2010), a British economist who informed the discussion of economic policy in the United Kingdom and later the United States. Godley was the main contributor to the development of the stock-flow-consistent approach to macroeconomics, setting out models based on rigorous accounting which allowed him to anticipate (ahead of more orthodox forecasters) adverse developments in the UK economy in the 1970s and 1980s, as well as the global recessions of 2001 and 2007–2009.

Bob Rowthorn’s Godley-Tobin lecture presented at the Eastern Economic Association, New York, on 1 March 2019 is not available as a paper at Review Of Keynesian Economics.

Adam Tooze’s book Crashed seems popular. The book and two reviews have some good appreciation of Wynne Godley’s work used in the book to explain why the crisis happened. The two reviews, both published in New Left Review:

In the acknowledgments section of his book Adam Tooze writes:

Wynne Godley was a mentor and teacher of a very different kind. Spontaneously warm and generous in spirit, he took me under his cape in my first year at King’s and introduced me, and a group of my contemporaries, to what was, at the time, a highly idiosyncratic brand of economics. In so doing he provided a model of intellectual warmth and vitality. He also confirmed doubts that had been gestating in me about the IS-LM model that was my first great love in economics. Wynne introduced me to the importance of looking “beyond the flows” and insisting on stock-flow consistency in macro models. I don’t think this book, written almost thirty years later would have been the same without his early influence.

Cédric Durand says:

What, then, are the conceptual underpinnings of Tooze’s work? In Crashed, none are made explicit. Nevertheless, in his emphasis on balancesheet vulnerabilities he implicitly follows the lead of post-Keynesian research, one of the more creative currents in contemporary economics, deriving from a synthesis of Keynes with a specific form of Marxian macroeconomics pioneered in the 1940s by Michał Kalecki. Tooze appears to draw in part upon the post-Keynesian ‘stock-flow consistency’ model, an approach that seeks to combine the ‘real’ and financial spheres of the economy. The term ‘stockflow’ implies attentiveness to the build-up of vulnerabilities in the ‘stock’ of financial assets and liabilities, beyond the financial ‘flows’ themselves: for example, when a sector’s prolonged deficit results in an unsustainable stock of debt. This approach has become increasingly popular since the crash, and was incorporated in the Bank of England’s policy-making toolkit in 2016. Initially developed by Nicholas Kaldor in the 1940s, the methodology was transformed in the 1960s and 70s by the work of James Tobin and Wynne Godley, Tooze’s teacher at Cambridge. Godley is credited by Tooze here with introducing him to ‘the importance of looking “beyond the flows” and insisting on stock-flow consistency’.

At the heart of this approach is the idea that macroeconomic dynamics hinge on a three-way interaction between the financial balances of public, private and foreign sectors. This ‘three balances’ perspective arguably supplies the unstated backbone of Tooze’s general argument. His achievement is to dress the dryness of this technical skeleton with the dense and complex sensitivity of historical flesh. If this framework were to be made explicit, it would suggest that the adventures of the private-sector balance drove a spectacular upward distribution of wealth that ultimately backfired in the political arena as resurgent nationalism and xenophobia. Public-sector balances were the scene of dramatic deliberations about crisis-containment strategy, with central bankers standing far above the other actors in the hierarchy of policy-making. Finally, the international balance-sheet perspective sheds light on a multipolar world where monetary policy, currency reserves and financial sanctions can be as effective as military force in deciding geopolitical outcomes and national fates.

…

Tooze’s mentor Wynne Godley observed in 1992 that the establishment of a single currency on the Maastricht model ‘would bring to an end the sovereignty of its component nations’, leaving them with the economic autonomy of ‘a local authority or colony’, while no central government could emerge with sufficient fiscal muscle to take decisive economic action. As a result, in the case of a major macroeconomic shock, the populations of countries deprived of the power to devalue, and not benefiting from a system of fiscal equalization, will see ‘emigration as the only alternative to poverty’. This sounds like an impressive, prescient account of the role of macro-institutional systems—and not just bad policy-making, as Tooze would have it—in the fates the Greek, Portuguese and Spanish people have had to suffer. Political, geopolitical and economic dimensions are structurally intertwined via institutions in the process of crisis making and management. While Tooze perfectly demonstrates the latter, in particular in his magnificent account of the balance-sheet intricacy at the heart of the 2008 crisis, he doesn’t account for the former.

Perry Anderson:

Durand observes, its narrative is no simple—or rather in this case, of course, highly complex and intricate—empirical tracking of the crisis and its outcomes. It possesses definite ‘conceptual underpinnings’, suggested by Tooze himself in acknowledging his debt to Wynne Godley’s use of ‘stock-flow consistency’ modelling of the financial interactions between public, private and foreign sectors. This in Durand’s view supplies ‘the unstated backbone’ of Tooze’s general argument.

Both judgements appear sound. But in Durand’s exposition a paradox attaches to each of them, since by the end of his review, somewhat different notes are struck. For Godley, one of the key advantages of the stock-flow consistency approach was that it integrated the financial with the real economy, as alternative models did not. Durand, however, remarks that Crashed ‘does not discuss the concrete intertwining of the financial and productive sectors in the global economy at all’, and so ‘fails to set the financial crisis in the context of the structural crisis tendencies within contemporary capitalist economies.’ This observation in turn generates another, which might seem to put in question Durand’s overall tribute to the book. For there he writes of ‘Tooze’s unwillingness to investigate the relations between the political and the economic’, a reluctance that ‘ultimately undermines his account of the crisis decade.’ Logically, the question then arises: do these two apparent contradictions lie in Tooze’s work, or in Durand’s review of it? Or can both be coherent in their own terms?

So Adam Tooze is appreciated in using the correct mathematical formulation but not paying much attention to political economy. Of course Wynne Godley’s work is based with a background in Kaldorian/Post-Keynesian economics, so the critique doesn’t apply to him. Tooze has a preface to his response to Anderson which will appear soon.

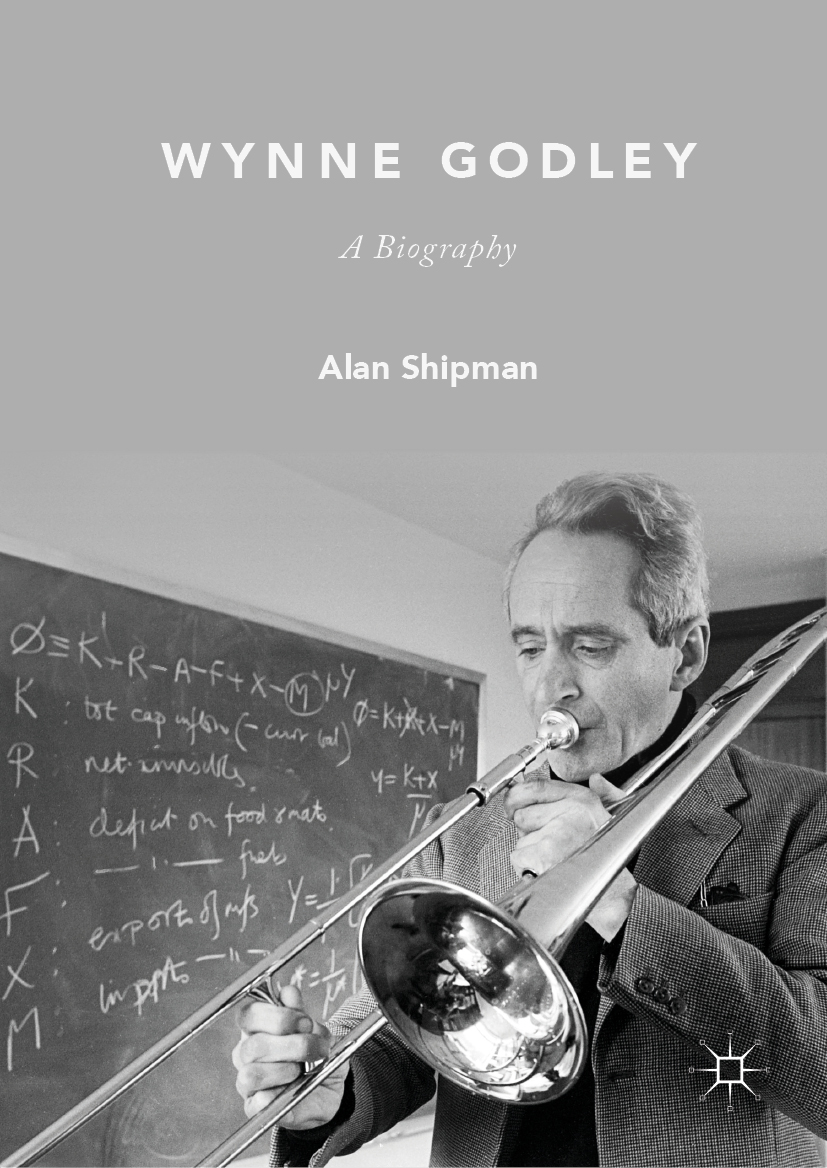

This timely biography of the economist Wynne Godley (1926-2010) charts his long and often crisis-blown route to a new way of understanding whole economies. It shows how early frustrations as a policy-maker enabled him to glimpse the cliff-edges other macro-modellers missed, and re-arm ‘Keynesian’ theory against the orthodoxy that had tried to absorb it. Godley gained notoriety for his economic commentaries – foreseeing the malaise of the 1970s, the Reagan-Thatcher slump, the unsustainable 1980s and 1990s booms, and the crises in the Eurozone and world economies after 2008. This foresight arose from a series of advances in his understanding of national accounting, price-setting, the role of modern finance, and the use of economic data, especially to grasp the interlinkage of stocks and flows. This biography also gives due attention to Godley’s life outside academic economics – including his chaotic childhood, truncated career as a professional oboist, equally brief stints as a sculptor’s model and economist in industry, and a longer spell as as a Treasury adviser with a mystery gift for forecasting.

This first full-length biography traces Wynne Godley’s long career from professional musician to public servant, policymaker, tormentor of conventional macroeconomics and creator of a workable alternative – all after escaping a childhood of decaying mansions and draconian schools, and rescuing his private world from the legacy of two Freuds. Drawing on Godley’s published and unpublished work and extensive interviews with those who knew him, the author explores Godley’s improbable life and explains the lasting significance of his work.

Chapters:

Life Before Economics

Under Treasury Rules 1956–1964

Short-Term Forecasting

Public Expenditure

Planning, Tax Reform and Structural Change

Gatecrashing the Cambridge Tradition

Public Expenditure Revisited

Sector Balances and ‘New Cambridge’

Balance of Payments, Deindustrialisation and Protection