Free trade is the most sacred tenet of Economics. So economists go at length to defend it. In doing so, they also ironically seem to talk like “Luddites”, i.e., claiming that automation is the cause of job losses.

Noah Smith has an articleDon’t Blame Robots for President Trump for Bloomberg View. The article is a large concession from orthodoxy. It says:

As Mishel and Bivens point out, estimates by Acemoglu and Restrepo imply that the effect of Chinese competition on U.S. manufacturing-job losses has been three times the effect of robots. So even researchers who are alarmed about robots think that so far, trade has been a much bigger shock to U.S. workers.

It’s easy to see all this is using simple Keynesian economics. In open economy macroeconomics, international trade affects the expenditure multiplier. So output is dependent on exports and imports and the actual output needn’t be the full employment output. Expenditure multiplier depends on both fiscal policy and the private expenditure function and so fiscal policy can be relaxed to achieve a higher output. But this process can be unsustainable.

Except that there may be a market mechanism to resolve imbalances in international trade. By that, what is usually meant is that stock-flow ratios converge and don’t keep rising (or falling if negative) without limits. In fixed exchange rate regimes, there is none. But free trade is not a new idea but an old one and orthodox economists used to argue for mechanisms. The problem with these is that they rely on Monetarism, which is deeply flawed. In floating exchange rate regimes, one could imagine adjustments of the exchange rate in doing the miracle. But it has not been seen in practice. In stock-flow coherent models, one does see adjustment of exchange rates leading to imbalances resolving but this is under simple simple assumptions on expectations of exchange rates. One can’t show this in general.

In reality, instead of convergence of fortunes of nations, what happens is polarisation. The nations who get a head start get more and more competitive and keep winning at the expense of the ones left behind. So we need a solution through actions of all governments.

A closely related claim is that manufacturing employment has reduced because of rise in productivity and not due to international factors. The Bloomberg article concedes that this orthodoxy is not true.

Some Post-Keynesian authors such as Wynne Godley had been stressing the importance of international trade on US employment. In his 1995 essay, A Critical Imbalance In U.S. Trade: The U.S. Balance Of Payments, International Indebtedness And Economic Policy, he said (page 16):

It is sometimes said that manufacturing has lost its importance and that countries in balance of payments difficulties should look to trade in services to put things right. However, while it is still true that manufacturing output has declined substantially as a share of GDP, the figures quoted above show that the share of manufacturing imports has risen substantially. The importance of manufacturing does not reside in the quantity of domestic output and employment it generates, still less in any intrinsic superiority that production of goods has over provision of services; it resides, rather, in the potential that manufactures have for expansion in international trade.

Wynne Godley’s Seven Unsustainable Processes (1999) examined the medium-term prospects for the US economy. It shows that in the United States, growth in that period was associated with seven unsustainable processes related to fiscal policy, foreign trade and payments, and private saving, spending, and borrowing. Given unchanged US fiscal policy and growth in the rest of the world, in order to maintain growth, the excessive indebtedness implied by these processes would be so large as to create major problems for the US economy and the world economy in the future. Godley was right. This web application aims to replicate Godley’s analysis for all of the countries in the EU, to see whether or not these unsustainable processes can be seen. It goes beyond Godley in forecasting each important ratio. The accompanying paper gives full details of the ratios and their construction.

There’s a new book, The Palgrave Companion To Cambridge Economics which features among other things biographies of Wynne Godley, Joan Robinson and Nicholas Kaldor and other notable Cambridge economists. Wynne Godley’s biography—Wynne Godley (1926-2010)—is by his closest collaborators – Francis Cripps and Marc Lavoie (pp. 929-953)

You can access the book on Springer, if you have subscription or preview it on Google Books.

Excerpt:

One interpretation of Godley’s theoretical work is that it is a quest for the Holy Grail of Keynesianism. Keynesians of all stripes had for a long time mentioned the need to integrate the real and the monetary sides of economics. Integration was all the talk, but for a long time, little seemed to be achieved … The main purpose of the Godley and Cripps’s 1983 book is to amalgamate the real and the financial sides, providing a theory of real output in a monetary economy …

Godley believed that Keynesian orthodoxy ‘did not properly incorporate money and other financial variables’ (ibid.: 15). Godley and Cripps and their colleagues ‘found quite early on that there was indeed something deficient in most macroeconomic models of the time’, including their own, ‘in that they tended to ignore constraints which adjustments of money and other financial assets impose on the economic system as a whole’ (ibid.: 16). Interestingly, Godley was aware of the work being carried out at about the same time by Tobin and his Yale colleagues, as well as by others such as Buiter, Christ, Ott and Ott, Turnovsky, and Blinder and Solow, who emphasized, as Godley and Cripps (ibid.: 18) did, that ‘money stocks and flows must satisfy accounting identities in individual budgets and in an economy as a whole’. Still, Godley thought that the analysis of the authors in this tradition was overly complicated, in particular because they assumed some given stock or growth rate of money, ‘leaving an endogenous rate of interest to reconcile’ this stock of money with the fiscal stance (Godley 1983: 137). Godley and Cripps (ibid.: 15) were also annoyed by several of the behavioural hypotheses found in the work of these more orthodox Keynesians, as they ‘could only give vague and complicated answers to simple questions like how money is created and what functions it fulfils’. The Cambridge authors thus wanted to start from scratch, with their own way of integrating the real and the financial sides, thus avoiding these ‘tormented replies’ (ibid.) …

Ultimately, Godley’s desire to present a definitive treatise based on consistent macroeconomic accounting gave rise, nearly 25 years later, to the Monetary Economics book (Godley and Lavoie 2007a) …

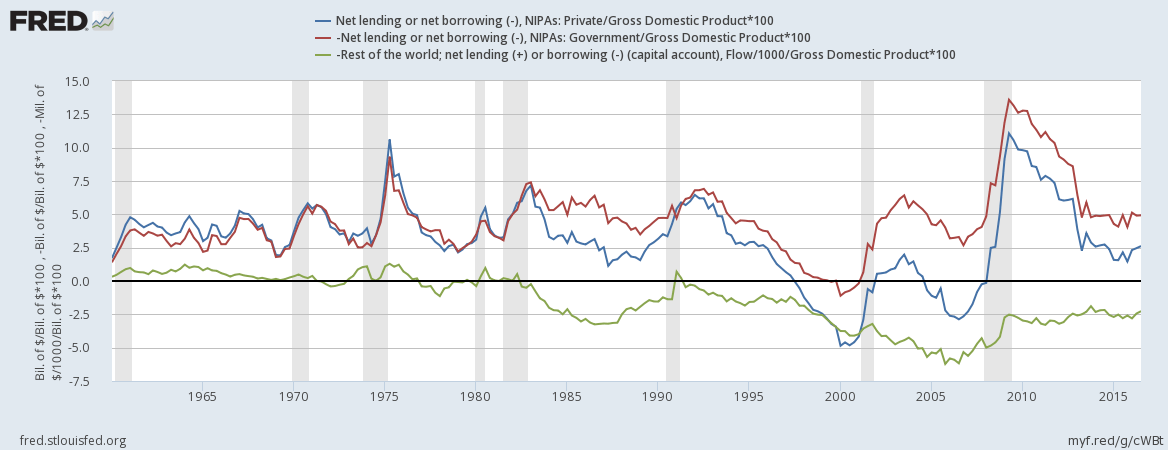

Tracking the sectoral balances of a nation’s economy is a great way to build a narrative about its economic dynamics. It’s true, that an accounting identity doesn’t say much about causation. But they hint it and if we have a behavioural model around it, then we learn a lot more. It was used by Wynne Godley to highlight the predicament on the horizon in the 2000s.

The Federal Reserve Bank of St. Louis has a nice website FRED where you can create charts and even observe them when new data gets updated. Below is the U.S. sectoral balances chart. This is a static image file. For the dynamic chart, track the link above (the header of this page).

The blue line is the private sector net lending—its income less expenditure— which was in deficit and led to the crisis. The red line is the government’s deficit and the green line is the current account balance of international payments.

The U.S. manufacturing deficit was $831 billion in 2015. The 2016 number might be out in a few days. Dean Baker has an excellent article, Painful Nonsense on Trade on his blog in which he debunks the claims of most economists that the US trade imbalance didn’t lead to job losses. He says:

… Note that the level of manufacturing employment, while it has cyclical ups and downs, is nearly constant from 1970 to 2000 at around 17 million. It plunged in the early years of the last decade as the trade deficit exploded. Most of the fall in employment was before the collapse of the housing bubble in 2008. This is what happens when a trade deficit increases from around 1.5 percent of GDP, the mid-1990s level, to almost 6.0 percent of GDP at its peak in 2005–2006 (over $1.1 trillion in today’s economy).

and also that the comparison to Germany is misleading:

DeLong also does a bit of sleight of hand in telling us that the loss of manufacturing employment is the same everywhere, pointing out that even Germany, the big success story, saw employment in manufacturing fall from about 40 percent of the labor force in 1971 to 20 percent at present. This is true, and if the United States had the same share of its workforce employed in manufacturing as Germany, we would have another 15 million manufacturing jobs.

It is sometimes said that manufacturing has lost its importance and that countries in balance of payments difficulties should look to trade in services to put things right. However, while it is still true that manufacturing output has declined substantially as a share of GDP, the figures quoted above show that the share of manufacturing imports has risen substantially. The importance of manufacturing does not reside in the quantity of domestic output and employment it generates, still less in any intrinsic superiority that production of goods has over provision of services; it resides, rather, in the potential that manufactures have for expansion in international trade.

Trade has always been a subject close to non-orthodox economics. Post-Keynesians emphasize the principle of circular and cumulative causation, which in the words of Nicholas Kaldor means, “success creates further success and failure begets more failure”. The importance of trade for the prospects of the US economy was emphasized the most by Wynne Godley in his series of papers for the Levy Institute from the mid-90s to late 2000s. In his paperSeven Unsustainable Processes, Godley said,

The logic of this analysis is that, over the coming five to ten years, it will be necessary not only to bring about a substantial relaxation in the fiscal stance but also to ensure, by one means or another, that there is a structural improvement in the United States’s balance of payments. It is not legitimate to assume that the external deficit will at some stage automatically correct itself; too many countries in the past have found themselves trapped by exploding overseas indebtedness that had eventually to be corrected by force majeure for this to be tenable.

There are, in principle, four ways in which the net export demand can be increased: (1) by depreciating the currency, (2) by deflating the economy to the point at which imports are reduced to the level of exports, (3) by getting other countries to expand their economies by fiscal or other means, and (4) by adopting “Article 12 control” of imports, so called after Article 12 of the GATT (General Agreement on Tariffs and Trade), which was creatively adjusted when the World Trade Organization came into existence specifically to allow nondiscriminatory import controls to protect a country’s foreign exchange reserves. This list of remedies for the external deficit does not include protection as commonly understood, namely, the selective use of tariffs or other discriminatory measures to assist particular industries and firms that are suffering from relative decline. This kind of protectionism is not included because, apart from other fundamental objections, it would not do the trick. Of the four alternatives, we rule out the second–progressive deflation and resulting high unemployment–on moral grounds. Serious difficulties attend the adoption of any of the remaining three remedies, but none of them can be ruled out categorically.

In his 2008 paper, Prospects For The United States And The Rest Of The World: A Crisis That Conventional Remedies Cannot Resolve, he said:

At the moment, the recovery plans under consideration by the United States and many other countries seem to be concentrated on the possibility of using expansionary fiscal and monetary policies.

But, however well coordinated, this approach will not be sufficient.

What must come to pass, perhaps obviously, is a worldwide recovery of output, combined with sustainable balances in international trade. Since this series of reports began in 1999, we have emphasized that, in the United States, sustained growth with full employment would eventually require both fiscal expansion and a rapid acceleration in net export demand. Part of the needed fiscal stimulus has already occurred, and much more (it seems) is immediately in prospect. But the U.S. balance of payments languishes, and a substantial and spontaneous recovery is now highly unlikely in view of the developing severe downturn in world trade and output. Nine years ago, it seemed possible that a dollar devaluation of 25 percent would do the trick. But a significantly larger adjustment is needed now. By our reckoning (which is put forward with great diffidence), if the United States were to attempt to restore full employment by fiscal and monetary means alone, the balance of payments deficit would rise over the next, say, three to four years, to 6 percent of GDP or more—that is, to a level that could not possibly be sustained for a long period, let alone indefinitely. Yet, for trade to begin expanding sufficiently would require exports to grow faster than we are at present expecting, implying that in three to four years the level of exports would be 25 percent higher than it would have been with no adjustments.

It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

So there was a voice for the Post-Keynesian community talking about US trade.

Dean Baker has an article saying the TPP gave us Trump and I agree. Although Donald Trump is a disaster socially, he is less dogmatic about trade and has promised to put tariffs on China (and has even promised fiscal expansion!). Since the Democrats (except Bernie Sanders) didn’t say anything about it and guarded orthodoxies, I believe this was decisive for Trump’s victory.

For the sake of quotes, here’s fromThe New York Times, July 31, 2016:

Mr. Trump himself said in a telephone interview last week that he believed more borrowing and spending would help lift economic growth, a departure from traditional Republican economics.

“It’s called priming the pump,” Mr. Trump said. “Sometimes you have to do that a little bit to get things going. We have no choice — otherwise, we are going to die on the vine.”

He added: “The economy would be crushed under Hillary. But no matter who it is, the debt is going up.”

Here’s a fun video of Donald Trump saying China in loop

click the picture to see the video on YouTube.

Since today morning the BBC has been saying how immoral Trump’s policies are: that fiscal expansion invariably burdens future generations and that thinking of the Chinese government using unfair trade policies is orthodoxy.

That’s not all, Paul Krugman even claimed that equity prices aren’t going to ever rise to pre-Trump level, a position which he flipped within hours after financial markets recovered.

So it’s not difficult to conclude that purely for the sake of defending one’s favourite party or ideology, people are going to make the case against fiscal policy and for free trade. We might hear a lot of pre-Keynesian orthodoxies from smart people more and more. I won’t even be surprised if Paul Krugman becomes a fiscal hawk again.

This has already been the case in discussions around wars. George Bush started the Iraq war and faced a lot of opposition from the so-called progressives. But then Barack Obama is the record holder for the most number of days as being in office as the President of the United States while the nation was at war but hardly gets any opposition from those who opposed him. I have also noticed that the same people who opposed Bush are now war apologizers.

So economic orthodoxy lies ahead. What will be sad is that it will come from people to the left of Republicans in the political spectrum.

There’s a paper by Jason Furman who is the Chairman of the Council of Economic Advisers which concedes how wrong economists were on fiscal policy. The link is a file hosted at the White House’s website! The paper starts off with a remarkable admission on fiscal policy (h/t and words borrowed from Jo Michell)

A decade ago, the prevalent view about fiscal policy among academic economists could be summarized in four admittedly stylized principles:

Discretionary fiscal policy is dominated by monetary policy as a stabilization tool because of lags in the application, impact, and removal of discretionary fiscal stimulus.

Even if policymakers get the timing right, discretionary fiscal stimulus would be somewhere between completely ineffective (the Ricardian view) or somewhat ineffective with bad side effects (higher interest rates and crowding-out of private investment).

Moreover, fiscal stabilization needs to be undertaken with trepidation, if at all, because the biggest fiscal policy priority should be the long-run fiscal balance.

Policymakers foolish enough to ignore (1) through (3) should at least make sure that any fiscal stimulus is very short-run, including pulling demand forward, to support the economy before monetary policy stimulus fully kicks in while minimizing harmful side effects and long-run fiscal harm.

Today, the tide of expert opinion is shifting the other way from this “Old View,” to almost the opposite view on all four points. This shift is partly the result of the prolonged aftermath of the global financial crisis and the increased realization that equilibrium interest rates have been declining for decades. It is also partly due to a better understanding of economic policy from the experience of the last eight years, including new empirical research on the impact of fiscal policy as well as observations of the reaction of sovereign debt markets to the large increases in debt as a share of GDP in the wake of the global financial crisis. In the first part of my remarks, I will discuss the theory and evidence underlying this “New View” of fiscal policy (with, admittedly, the core of this theory being an “Old Old View” that dates back to John Maynard Keynes and the liquidity trap).

Compare that to the Post-Keynesian view, which according to Wynne Godley and Marc Lavoie in their book Monetary Economics written before the crisis (from chapter 1, Introduction):

The alternative paradigm, which has come to be called ‘post-Keynesian’ or ‘structuralist’, derives originally from those economists who were more or less closely associated personally with Keynes such as Joan Robinson, Richard Kahn, Nicholas Kaldor, and James Meade, as well as Michal Kalecki who derived most of his ideas independently.

… According to post-Keynesian ideas, there is no natural tendency for economies to generate full employment, and for this and other reasons growth and stability require the active participation of governments in the form of fiscal, monetary and incomes policy.

There is no branch of economics in which there is a wider gap between orthodox doctrine and actual problems than in the theory of international trade.

– Joan Robinson, The Need For A Reconsideration Of The Theory Of International Trade, 1973

Orthodox trade theory tells us that the “market mechanism” should work to resolve imbalances in the current account of balance of international payments. Although, the economics profession has conceded that Keynesianism is correct, it is still far from thinking clearly about international trade.

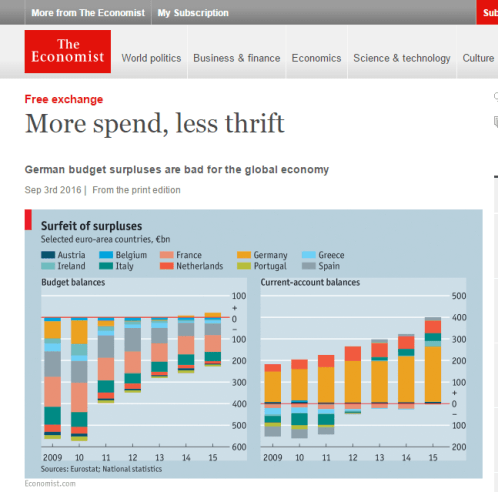

So it is a bit surprising that The Economist would say something unorthodox about this. In a recent article it complains about Germany:

This is the Post-Keynesian idea that surplus economies put a burden on deficit economies.

A fiscal expansion by the German government has the effect of raising domestic demand and imports and reducing the German current account balance of payments. This allows the rest of the world to grow both because of German imports and also because they are less “balance-of-payments constraint”.

Second, Brad Setser has a blog post on the current account surplus of the Republic of Korea (South Korea).

It’s impressive to see Setser get the causality right:

Fiscal policy alone doesn’t determine the current account (even if tends to be the biggest factor in the IMF’s own model). A boom in domestic demand, for example, would improve the fiscal balance and lower the current account surplus, just as a fall in private demand improves the current account balance while raising the fiscal deficit.

The current account balance, government’s budget balance and the private sector financial balance are related by an identity and sum to zero. But the identity itself shouldn’t be confused with causation.

The correct causation between the balances is between domestic demand and output at home versus abroad. This causality has been highlighted by Wynne Godley in the past. See more on this blog post by me here.

Stephen Kinsella is out with a new paper with co-authors Stephen Burgess, Oliver Burrows, Antoine Godin, and Stephen Millard published by the Bank of England.

From the paper:

Our paper makes two contributions to the literature. First, we develop, estimate, and calibrate the model itself from first principles as well as describing the stock-flow consistent database we construct to validate the model; as far as we know, we are the first to develop such a sophisticated SFC model of the UK economy in recent years.4 And second, we impose several scenarios on the model to test its usefulness as a medium-term scenario analysis tool. The approach we propose to use links decisions about real variables to credit creation in the financial sector and decisions about asset allocation among investors. It was developed in the 1980s and 1990s by James Tobin on the one hand, and Wynne Godley and co-authors on the other, and is known as the ‘stock-flow consistent’ (SFC) approach. The approach is best described in Godley and Lavoie (2012) and Caverzasi and Godin (2015) and underpins the models of Barwell and Burrows (2011), Greiff et al. (2011), and Caiani et al. (2014a,b). Dos Santos (2006) describes how SFC models incorporate detailed accounting constraints typically found in systems of national accounts. SFC models allow us to build a framework for the model where every flow comes from somewhere in the economy and goes somewhere, and sectoral savings/borrowings and capital gains/losses add or subtract from stocks of wealth/debt, following Copeland (1949). Accounting constraints allow us to identify relationships between sectoral transactions in the short and long run. The addition of accounting constraints is crucial, as one aspect of the economy we would like to model is the way it might react differently when policies such as fiscal consolidations are imposed slowly or quickly

4 Such models were popular in the past; for example Davis (1987a, 1987b) developed a rudimentary stock flow consistent model of the UK economy.